The Cost of Financial Misinformation (And How to Take Back Control)

Have you ever signed a loan agreement you didn’t fully understand?

You’re not alone. Millions of people pay more than they should on loans, ruin their credit by accident, or fall into debt traps not because they’re irresponsible, but because they were never taught how the system works.

The financial system is complex on purpose. From confusing rates to hidden fees, the odds are stacked against everyday borrowers.

At LookUpLoans, we believe that access to clear, unbiased financial education is a form of empowerment. And that when you understand how credit, interest, and lending actually work you make smarter decisions, avoid costly mistakes, and stay in control of your future.

This guide is your starting point.

We’ll break down how lenders really make money, the mistakes that quietly keep people in debt, and the tools you can use to borrow better, pay less, and protect your credit.

The Truth About Loans and Credit (That Lenders Won’t Tell You)

Lenders don’t profit when you pay off your debt quickly. They profit when you stay in debt longer, pay more in interest, and accept terms you don’t fully understand.

From “too good to be true” interest rates to hidden fees buried in fine print, the lending system often works against the very people it claims to serve. And while financial institutions spend millions marketing loan products, they spend far less teaching people how those loans really work.

The result?

- Borrowers locked into expensive, long-term debt

- Missed payments due to confusing terms or unexpected fees

- Damaged credit scores from decisions made in the dark

And yet most of it is preventable.

At LookUpLoans, we’re not here to sell you on a loan. We’re here to give you the tools to understand how borrowing actually works, so you can avoid the traps, negotiate better terms, and protect your financial health long-term.

We expose what the industry doesn’t want you to know, like:

- How lenders really calculate your loan costs

- What’s behind the “guaranteed approval” ads

- Why some loans destroy credit while others build it

- And how to compare loan offers on your terms, not theirs

This isn’t financial theory. It’s real-world information you can use today to borrow smarter, repay faster, and finally feel confident about your financial decisions.

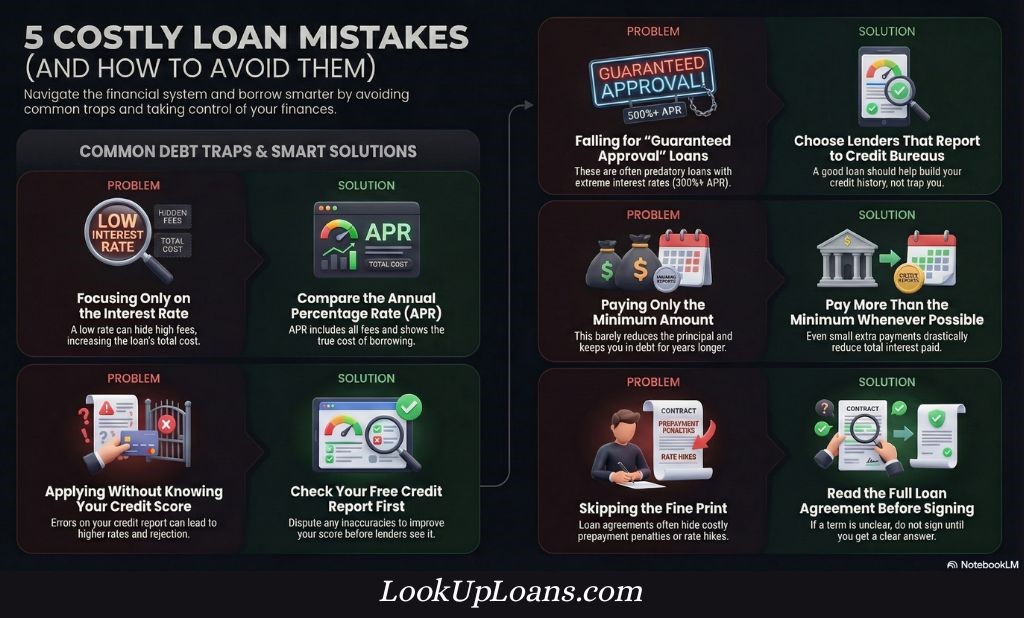

7 Costly Mistakes That Keep People in Debt

Most people don’t go into debt recklessly. It happens slowly through small decisions, bad advice, and confusing loan terms that were never fully explained.

Here are seven of the most common borrowing mistakes and how to avoid them starting today.

1. Focusing Only on the Interest Rate

A low interest rate sounds great but it doesn’t always mean a low-cost loan.

Lenders often pair “introductory” or advertised low rates with:

- High origination or administrative fees

- Variable rate clauses that increase your cost over time

- Long loan terms that lower your monthly payment but raise your total repayment

What to do instead:

Always calculate the APR (Annual Percentage Rate), not just the interest rate. It includes all fees and gives you the real cost of borrowing.

2. Applying Without Knowing Your Borrowing Power

Many people apply for loans with no clear sense of how much they should borrow, only how much they can borrow.

That leads to:

- Over-borrowing (leading to long-term debt)

- Under-borrowing (limiting opportunities or forcing repeat borrowing)

What to do instead:

Before applying, assess your financial profile income, existing debts, goals and use a loan calculator to estimate what you can comfortably afford to repay.

3. Not Checking Your Credit Report First

A single error on your credit report like an old account still marked “unpaid” can lower your score and increase your interest rate, costing you thousands over the life of a loan.

What to do instead:

- Get a free credit report at AnnualCreditReport.com

- Dispute inaccuracies

- Know your score before lenders do

Checking your credit takes minutes and can instantly put you in a stronger negotiating position.

4. Falling for “Guaranteed Approval” or “No Credit Check” Loans

These offers may look appealing, especially if you’re worried about your credit. But many are structured to trap borrowers in cycles of fees, penalties, and rollovers.

What to watch for:

- Payday loans with 300%+ APR

- Title loans that risk your vehicle

- Hidden clauses that extend the loan without reducing the principal

What to do instead:

Look for lenders that report to credit bureaus, offer fair terms, and are transparent about repayment schedules. Reputable lending doesn’t rely on bait-and-switch tactics.

5. Paying Only the Minimum

Minimum payments keep you in good standing but also keep you in debt.

When you only pay the minimum:

- Interest continues to accumulate

- Your principal barely goes down

- The loan lasts years longer than necessary

What to do instead:

Pay more than the minimum whenever possible. Even a small increase can dramatically reduce total interest and shorten your loan term.

6. Skimming the Fine Print (Or Skipping It Entirely)

Buried in many loan agreements are terms that can cost you later:

- Prepayment penalties

- Balloon payments

- Rate hikes after a “promo” period ends

What to do instead:

Slow down. Read the full loan agreement. Ask questions. And if something’s unclear, don’t sign until you’re satisfied with the answer.

7. Believing All Loans Help Build Credit

Some lenders don’t report to credit bureaus at all meaning your positive payment history won’t improve your score.

Worse, some predatory loans can damage your credit if they’re structured to encourage missed payments or renewals.

What to do instead:

Choose lenders that report to all three major credit bureaus. Consider credit-builder loans or secured credit cards if your goal is to raise your score.

The biggest financial mistakes aren’t always the loud ones, they’re the quiet, overlooked decisions that cost you time, money, and freedom.

Now that you know what to watch out for, let’s look at how to recognize a fair loan offer, figure out how much you can truly afford, and take control of your credit no matter where you’re starting from.

Borrowing Mistakes, Solutions, and Financial Tips

| Common Mistake or Question | Key Risk or Trap | Recommended Action | Financial Tool or Resource | Benefit of Following Advice |

|---|---|---|---|---|

| Focusing Only on the Interest Rate | Hidden fees, variable rate hikes, and long terms that increase total repayment costs. | Always calculate the APR (Annual Percentage Rate) to see the real cost including all fees. | APR Calculator | Reveals the true cost of borrowing and avoids hidden administrative fees. |

| Falling for “Guaranteed Approval” or “No Credit Check” Loans | Payday loans with 300%+ APR, title loans risking vehicles, and cycles of fees or penalties. | Look for lenders that report to credit bureaus and are transparent about repayment. | Lender Reviews and Comparisons | Avoids bait-and-switch tactics and predatory debt cycles. |

| Applying Without Knowing Your Borrowing Power | Over-borrowing leading to long-term debt or under-borrowing limiting opportunities. | Assess income and existing debts; use a calculator to estimate affordable repayments. | Loan Affordability Calculator | Ensures the borrower can comfortably repay without sacrificing other goals. |

| Not Checking Your Credit Report First | Errors can lower scores and increase interest rates, costing thousands over the loan life. | Get a free report, dispute inaccuracies, and know your score before lenders do. | AnnualCreditReport.com | Puts the borrower in a stronger negotiating position and lowers interest rates. |

| Paying Only the Minimum | Interest accumulates, the principal barely decreases, and the loan lasts years longer. | Pay more than the minimum whenever possible. | Custom Payoff Plans | Dramatically reduces total interest and shortens the loan term. |

| Skimming the Fine Print | Prepayment penalties, balloon payments, and rate hikes after promo periods. | Slow down and read the full agreement; ask questions before signing. | Loan Education Guides | Prevents unexpected costs and restrictive terms later in the loan. |

| Believing All Loans Help Build Credit | Lenders that don’t report to bureaus won’t help your score; some predatory loans damage it. | Choose lenders that report to all three major bureaus; consider credit-builder loans. | Credit-builder loans or secured credit cards | Positively impacts credit history and improves future borrowing opportunities. |

Look Up Loans: Everything You Need to Know Guide

The good news? You don’t need to be a financial expert to avoid common debt traps, you just need the right information, in plain language, at the right time.

At LookUpLoans, we break down what most lenders won’t explain and give you the tools to borrow confidently, protect your credit, and avoid hidden costs.

Below are answers to some of the biggest questions people ask before applying for a loan along with guidance to help you make smarter decisions at every step.

1. How Do I Know If I’m Getting a Fair Loan?

Most people accept the first offer they receive even if the terms aren’t ideal. But just like shopping for a car or home, loan terms are negotiable, and better options are often out there.

Here’s what makes a loan fair:

- Transparent APR (Annual Percentage Rate): Not just the interest rate, but all fees included

- Clear repayment terms: No hidden balloon payments or vague due dates

- No excessive penalties: Prepayment penalties, early exit fees, or late charges should be reasonable

- Aligned with your credit profile: Your rate should reflect your current score not punish you for it

What to do: Use a loan comparison tool to evaluate multiple lenders side by side. Don’t just look at the monthly payment look at the total repayment amount over the full term.

2. How Much Can I Actually Afford to Borrow?

This isn’t just about how much you qualify for, it’s about how much you can comfortably repay without stretching your budget or sacrificing other goals.

What to consider:

- Monthly income and fixed expenses

- Existing debt obligations

- Loan term and interest rate

- Emergency savings cushion

What to do: Use our interactive Loan Affordability Calculator to get a personalized estimate based on your income and lifestyle. Borrowing less may cost more monthly but it often saves you thousands over time.

3. What If I Have Bad Credit? Can I Still Get a Loan?

Yes, but proceed carefully. Some lenders specialize in helping borrowers rebuild credit, while others target vulnerable consumers with high-risk, high-cost offers.

How to protect yourself:

- Avoid loans with triple-digit APRs or aggressive rollover terms

- Look for lenders that report to credit bureaus, this helps your score

- Read reviews and confirm licensing or registration before applying

Pro Tip: Secured loans or credit-builder loans may offer safer terms and lower rates than high-interest “bad credit” products.

4. How Can I Boost My Credit to Get Better Loan Offers?

Improving your credit score is one of the most powerful things you can do to unlock lower rates and better financial opportunities.

Here’s what actually works:

- Lower your credit utilization: Keep balances under 30% of your available limit

- Pay on time, every time: Even one missed payment can hurt your score

- Dispute errors: 1 in 5 credit reports has a mistake fixing one can raise your score fast

- Add positive history: Become an authorized user on a trusted account or use a credit-builder product

What to do: Set up automatic payments. Review your credit report at least twice a year. And give yourself 60–90 days before applying for a loan to optimize your profile.

Understanding these principles can save you thousands and open doors to better financial choices.

In the next section, we’ll show you exactly what you can find here on LookUpLoans from tools and calculators to unbiased lender reviews and expert strategies.

What You’ll Find on LookUpLoans

We built LookUpLoans for people who want to borrow smarter not just faster.

Whether you’re trying to understand your credit, compare loan offers, or avoid common traps, everything on this site is designed to help you make confident, informed decisions.

Here’s how we help you take control of your financial future:

Clear, Jargon-Free Loan Education

No financial background? No problem.

Our guides explain loans, credit, and borrowing strategies in plain English without the industry jargon that confuses and overwhelms.

You’ll learn:

- How different loans work (personal, secured, business, auto, and more)

- What terms to watch out for in any loan agreement

- How to evaluate loan offers on your terms not the lender’s

Step-by-Step Borrowing Strategies

From getting your first loan to refinancing existing debt, we walk you through every major financial decision with clear, actionable guidance.

Inside our borrowing guides, you’ll discover:

- When it’s smarter to choose a secured loan over an unsecured one

- How to consolidate debt without damaging your credit

- The right questions to ask a lender before you sign anything

Interactive Tools & Calculators

We believe in doing the math not guessing.

Our calculators help you:

- Estimate monthly loan payments

- Compare total interest over different terms

- See what you can really afford to borrow based on your income and goals

- Build custom payoff plans that actually fit your lifestyle

These tools are free to use and available 24/7 no email opt-in required.

Unbiased Lender Reviews & Comparisons

We don’t push loan offers. We don’t get paid to rank one lender over another.

Instead, we give you:

- Transparent comparisons based on real data

- Honest reviews of terms, fees, customer service, and approval flexibility

- Insights into which lenders are best for specific situations (e.g., poor credit, fast funding, low income)

You’ll know exactly who you’re borrowing from and what to expect before you apply.

Credit Score Improvement Resources

Want better rates and more approval options? It starts with your credit score.

We show you how to:

- Monitor and understand your credit report

- Improve your score with simple, effective steps

- Avoid common credit-building myths and mistakes

- Use tools like secured cards and credit-builder loans strategically

Your credit score shouldn’t be a mystery and we’re here to help make it work for you.

LookUpLoans isn’t about quick hacks or financial hype. It’s about equipping you with real knowledge, tools, and confidence so you can make the best financial choices for your life.

Up next, we’ll show you why you can trust us and what sets us apart from traditional financial sites.

Why Trust LookUpLoans?

In a financial world filled with fine print, biased advice, and confusing offers, we believe in one thing above all:

You deserve the truth.

We’re not a lender. We don’t sell loans. And we don’t earn more when you borrow more.

Our only mission is to help you understand your options, protect your credit, and borrow smarter on your terms.

Here’s how we stay accountable to you:

1. Unbiased, Education-First Content

Every guide, comparison, and resource we publish is built around one goal: helping you make informed financial decisions with clarity and confidence.

We:

- Break down complex financial topics without the jargon

- Teach you how to think like a lender (so you’re never surprised)

- Focus on facts, not fear or hype

You won’t find flashy promises here. Just straight answers and practical tools.

2. No Sales Tactics. Ever.

Most financial sites make money by pushing loan offers or hiding the downside of borrowing. Not here.

We:

- Don’t accept payment for ranking lenders

- Don’t recommend products we wouldn’t use ourselves

- Don’t suggest loans that trap you in long-term debt

If a product has hidden fees, predatory terms, or questionable practices we’ll tell you.

3. Built for Everyday Borrowers

We know what it’s like to be confused by credit scores, loan terms, or rejection letters. That’s why LookUpLoans is built for real people, not finance pros.

Whether you’re:

- Trying to qualify for your first loan

- Rebuilding credit after a tough year

- Weighing debt consolidation or refinancing options You’re in the right place.

We provide the kind of financial advice we wish we had when we started.

4. Transparency First, Always

We explain how loans work, how lenders profit, and how to spot red flags because no one else is doing it.

We’re committed to:

- Clear disclosures

- Plain-language breakdowns

- Content reviewed and updated regularly to reflect real market conditions

When you come to LookUpLoans, you can trust that what you’re reading is written for your benefit not the lender’s.

At the end of the day, we’re not here to tell you what to do with your money. We’re here to give you the knowledge and tools to decide for yourself with confidence.

If you’re ready to take control of your borrowing power, let’s move forward together.

Take Control of Your Borrowing Power Starting Today

You don’t have to overpay for a loan. You don’t have to guess what lenders are thinking. And you don’t have to figure it all out alone.

At LookUpLoans, we give you the knowledge and tools to borrow confidently, avoid hidden costs, and build a stronger financial future on your terms.

Here’s how to get started:

- Explore our loan guides to learn how different options really work

- Use our calculators to see what you can afford (and what it will really cost)

- Compare lenders based on what matters to you not to them

- Start improving your credit with practical, no-fluff tips that work

Wherever you’re starting from, this is your next step forward.

→ Explore our tools and take control of your financial future now.