Introduction

Buy Now, Pay Later has become a common option at checkout. Whether you’re shopping online or in a store, you’ve likely seen the offer: split your purchase into smaller payments instead of paying the full amount upfront.

On the surface, it sounds simple and convenient. Smaller payments can feel easier to manage than one larger charge.

But how does Buy Now, Pay Later actually work? And is it a helpful budgeting tool, or can it create financial strain if not used carefully?

In this guide, we’ll walk through what Buy Now, Pay Later is, how it works, the potential risks, and when it may or may not make sense to use.

Key Takeaways

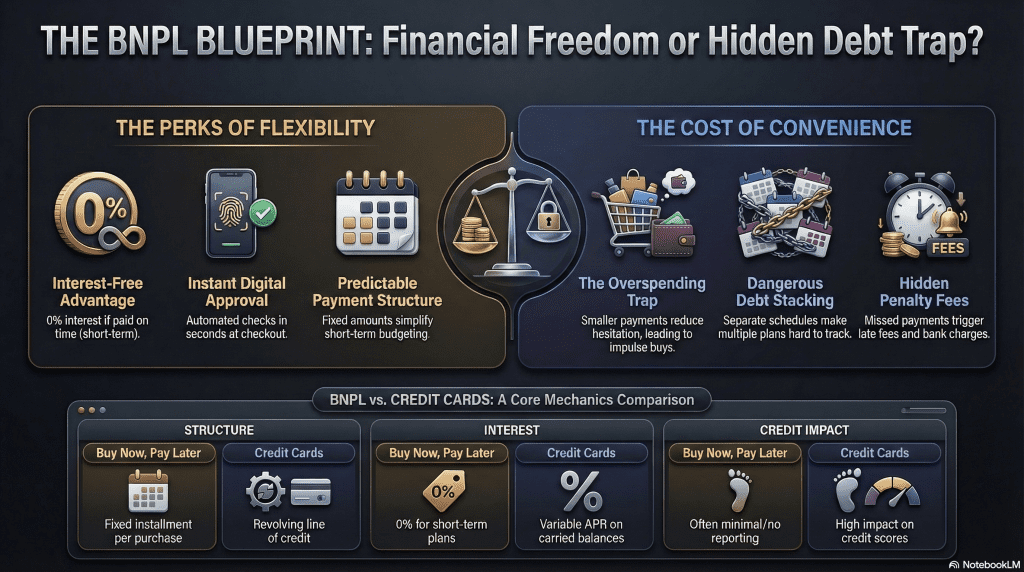

- Buy Now, Pay Later (BNPL) allows you to split a purchase into smaller installments, often over a few weeks or months instead of paying upfront.

- Many short-term plans are interest-free if payments are made on time, but longer-term plans may include interest charges.

- Each purchase creates its own payment schedule, which can become difficult to manage if you use BNPL frequently.

- Missed payments may result in late fees and could affect your credit, depending on the provider and plan type.

- BNPL is not designed as a credit-building tool, and on-time payments are not always reported to credit bureaus.

- It can be useful for planned purchases that fit within your budget, but it requires careful tracking and financial discipline.

Disclaimer: This site contains affiliate links. If you make a purchase, we may earn a commission at no extra cost to you.

What Is Buy Now, Pay Later?

Buy Now, Pay Later (often abbreviated as BNPL) is a short-term financing option that allows you to divide a purchase into smaller payments over time instead of paying the full amount upfront.

It’s typically offered at checkout, both online and in stores, through third-party providers. After a quick approval process, you agree to a payment schedule, often four equal installments spread over several weeks.

In many cases, short-term plans are advertised as interest-free, as long as payments are made on time. Some providers also offer longer-term installment plans, which may include interest.

Unlike traditional credit cards, BNPL is usually tied to a specific purchase rather than an open line of credit you can reuse repeatedly. Each transaction creates its own payment plan.

At its core, Buy Now, Pay Later is a payment method designed to spread out costs. The structure may feel simple, but the terms and implications can vary depending on the provider and the plan you choose.

How Buy Now, Pay Later Works (Step by Step)

Although the process feels quick and simple at checkout, there are several structured steps behind it.

1. You Select Buy Now, Pay Later at Checkout

When completing a purchase, you choose the Buy Now, Pay Later option instead of paying in full with a debit or credit card.

The BNPL provider becomes the company financing the transaction. In most cases, the provider pays the merchant upfront, and you agree to repay the provider over time.

2. A Quick Approval Process Takes Place

You’ll enter basic personal information such as your name, address, and date of birth. Some providers may request additional verification details. Approval decisions are typically automated and completed within seconds.

Depending on the provider and the purchase amount, a soft credit check or internal risk review may be performed.

3. You Make an Initial Payment

For many short-term plans, the first installment is due immediately at checkout.

A common structure is four equal payments spread over six weeks, meaning you pay one-quarter of the total purchase price upfront.

4. Remaining Payments Are Scheduled Automatically

The remaining installments are automatically withdrawn from your linked debit card or bank account on scheduled dates, often every two weeks.

You’ll usually receive reminders before each payment, but the withdrawals occur automatically unless you reschedule or pay early through the provider’s app or website.

5. Fees or Consequences May Apply if Payments Are Missed

If a scheduled payment fails due to insufficient funds or is not made on time, late fees may apply depending on the provider’s terms.

Some providers may pause your ability to make new purchases. In certain cases, unpaid balances may eventually be sent to collections.

Each purchase creates a separate payment plan. If you use Buy Now, Pay Later for multiple transactions, you may end up managing several overlapping payment schedules at once. While each individual plan may seem small, the combined total can add up quickly if not monitored carefully.

Why Buy Now, Pay Later Is So Popular

Buy Now, Pay Later has grown quickly in recent years, largely because it combines convenience with simplicity at the moment of purchase.

Fast and Easy Approval

The approval process typically takes only seconds and requires minimal information. There’s no lengthy application, and decisions are made almost instantly. That speed makes it appealing, especially during online shopping.

Smaller, Manageable Payments

Breaking a purchase into smaller installments can make a higher price feel more affordable. Instead of paying the full amount upfront, you spread the cost over several weeks or months.

For many consumers, this structure feels easier to fit into a budget.

Interest-Free Short-Term Options

Many short-term plans advertise no interest as long as payments are made on time. Compared to carrying a balance on a traditional credit card, this can seem like a lower-cost alternative.

Seamless Checkout Experience

Buy Now, Pay Later is integrated directly into many retail checkout systems. There’s no need to apply for a separate credit card or visit a bank. The financing option appears alongside other payment methods, making it feel like a normal part of the purchase process.

Psychological Appeal

Smaller installment amounts can feel less intimidating than a single larger charge. Even if the total cost is the same, dividing it into parts can reduce hesitation and make a purchase feel more manageable.

This combination of speed, simplicity, and perceived affordability is what has driven its widespread adoption.

The Potential Risks and Downsides

While Buy Now, Pay Later can be convenient, it isn’t risk-free. Understanding the potential downsides is essential before using it regularly.

Late Fees and Penalties

If a scheduled payment fails or is missed, late fees may apply depending on the provider’s terms. Even small fees can add up if multiple payments are missed across different purchases.

Because payments are often automatically withdrawn, insufficient funds in your account can also trigger bank overdraft fees.

Overspending Made Easier

Breaking a purchase into smaller payments can make it feel more affordable than it actually is. This can reduce the natural hesitation that comes with larger purchases.

When used occasionally and intentionally, this may not be a problem. But frequent use can lead to spending beyond what your budget comfortably allows.

Multiple Payment Plans at Once

Each transaction creates its own installment schedule. If you use Buy Now, Pay Later for several purchases, you may end up managing multiple overlapping payment dates.

Individually, each plan may seem manageable. Combined, they can create financial strain if not tracked carefully.

Longer-Term Plans May Include Interest

While many short-term plans advertise no interest, some providers offer extended installment options that do include interest charges. These plans function more like traditional loans and can increase the total cost of your purchase.

Not a Substitute for Financial Planning

Buy Now, Pay Later can make purchases easier in the moment, but it doesn’t reduce the overall cost. If used to cover expenses that exceed your budget, it may delay financial pressure rather than solve it.

Understanding these risks helps ensure that convenience doesn’t turn into unintended debt.

Does Buy Now, Pay Later Affect Your Credit?

The answer depends on the provider and the specific plan you choose.

Initial Approval Checks

Many Buy Now, Pay Later providers perform a soft credit check during the approval process. A soft check does not affect your credit score and is typically used to verify identity and assess basic risk.

Some longer-term financing plans, however, may involve a hard credit inquiry. A hard inquiry can have a small, temporary impact on your credit score.

On-Time Payments

Not all providers report on-time payments to the major credit bureaus. In many short-term “pay-in-four” plans, positive payment activity may not appear on your credit report at all.

That means using Buy Now, Pay Later responsibly does not automatically build your credit in the way a traditional loan or credit card might.

Missed Payments

Late or missed payments may be reported, especially if the account becomes significantly past due or is sent to collections. If that happens, it can negatively affect your credit.

The exact reporting practices vary by provider and plan type, so reviewing the terms before agreeing is important.

Longer-Term Installment Plans

Some Buy Now, Pay Later services offer extended financing options that function more like traditional installment loans. These plans are more likely to involve formal credit checks and credit reporting.

In short, Buy Now, Pay Later is not designed primarily as a credit-building tool. Depending on how it’s structured and used, it may have little impact on your credit unless payments are missed.

Buy Now, Pay Later vs. Credit Cards

Both Buy Now, Pay Later (BNPL) and credit cards allow you to make purchases without paying the full amount upfront. However, they function differently and carry different responsibilities.

| Feature | Buy Now, Pay Later | Credit Card |

|---|---|---|

| Structure | Fixed installment plan tied to a specific purchase | Revolving line of credit that can be reused |

| Approval Process | Quick, often automated | Formal application with credit review |

| Interest | Often interest-free for short-term plans; interest may apply for longer terms | Interest applies if you carry a balance past the due date |

| Payment Schedule | Set installment dates, usually automatic withdrawals | Flexible payments, with a minimum due each month |

| Credit Impact | May not report on-time payments; missed payments may be reported | Typically reports both positive and negative activity |

| Spending Flexibility | Limited to individual purchases | Can be used repeatedly up to your credit limit |

| Risk Pattern | Risk of stacking multiple small payment plans | Risk of carrying high revolving balances |

Key Differences to Consider

A credit card provides ongoing access to credit, but it requires careful balance management to avoid interest charges.

Buy Now, Pay Later plans are more structured and short-term, which can feel simpler. However, because each purchase creates a separate obligation, it’s easier to lose track if used frequently.

Neither option is inherently better. The right choice depends on your spending habits, ability to track payments, and overall financial situation.

When It Might Make Sense to Use Buy Now, Pay Later

Buy Now, Pay Later can be useful in certain situations particularly when it’s used intentionally rather than impulsively.

For a Planned Purchase

If you’ve already decided to make a purchase and have reviewed your budget, spreading the cost over a few weeks may provide short-term flexibility without adding long-term debt.

The key is that the purchase fits within your financial plan before selecting the installment option.

When You Can Comfortably Cover the Payments

Before choosing BNPL, it helps to know that the scheduled withdrawals won’t strain your cash flow. If you could pay the full amount upfront but prefer to spread it out, the risk is generally lower.

For Short-Term, Interest-Free Plans

Many short-term installment options do not charge interest as long as payments are made on time. When used responsibly, this can be a way to manage timing without increasing the total cost of a purchase.

If You’re Tracking Your Obligations Carefully

If you keep a clear record of upcoming payment dates and avoid stacking multiple plans, BNPL can remain manageable. Awareness and organization make a significant difference.

Used thoughtfully, Buy Now, Pay Later can serve as a short-term payment tool. The benefit comes from discipline, not from the convenience alone.

When to Be Cautious

Buy Now, Pay Later can become problematic when convenience replaces planning. In certain situations, extra caution is warranted.

If Your Budget Is Already Tight

If covering regular monthly expenses is already challenging, adding fixed installment payments may increase financial strain. Even small, biweekly withdrawals can create pressure if your margin is limited.

If You’re Managing Multiple Payment Plans

Because each purchase creates a separate schedule, it’s easy to lose track of how many active plans you have. Several small payments due at different times can quickly add up to a larger total obligation.

If You’re Using It for Everyday Necessities

Using installment payments for nonessential purchases occasionally is different from relying on them for routine expenses like groceries or utilities. If BNPL becomes a way to cover basic needs, it may signal a deeper budgeting issue.

If You’re Already Carrying Other Debt

Adding new installment commitments while managing existing credit card balances or loan payments can increase overall financial pressure. In those cases, reducing current obligations may be more helpful than adding new ones.

Buy Now, Pay Later works best as a deliberate choice not a default payment method. When used without careful oversight, small commitments can quietly grow into larger financial stress.

Final Thoughts

Buy Now, Pay Later has become a common part of modern checkout. Its appeal is easy to understand: fast approval, smaller payments, and the ability to spread out costs without immediately reaching for a credit card.

But convenience doesn’t remove responsibility.

At its best, Buy Now, Pay Later can provide short-term flexibility for planned purchases that comfortably fit within your budget. At its worst, it can make spending feel easier than it truly is, especially when multiple payment plans overlap.

The key is understanding what it is and what it isn’t. It’s a payment tool, not a financial strategy. It doesn’t reduce the cost of what you’re buying, and it doesn’t replace thoughtful budgeting.

When used intentionally and monitored carefully, it can serve a purpose. When used casually or frequently without tracking, it can create unnecessary strain.

Like many financial tools, the impact depends less on the product itself and more on how it’s used.

Frequently Asked Questions

Is Buy Now, Pay Later the same as a credit card?

No. A credit card provides a revolving line of credit you can reuse up to your limit. Buy Now, Pay Later creates a separate installment plan for each purchase. The structure, repayment schedule, and credit impact can differ significantly.

Do Buy Now, Pay Later services charge interest?

Many short-term “pay-in-four” plans do not charge interest if payments are made on time. However, longer-term installment plans may include interest. It’s important to review the terms before agreeing to a payment plan.

Will using Buy Now, Pay Later improve my credit score?

Not necessarily. Some providers do not report on-time payments to credit bureaus. In certain cases, missed payments may be reported. Buy Now, Pay Later should not be relied on as a primary credit-building strategy.

What happens if I miss a payment?

Depending on the provider, you may be charged a late fee. Repeated missed payments could lead to account restrictions or collections activity. Automatic withdrawals may also result in bank overdraft fees if funds are unavailable.

Can I use multiple Buy Now, Pay Later plans at the same time?

Yes, but each purchase creates its own payment schedule. Managing multiple overlapping plans can become difficult if not tracked carefully. It’s important to understand your total upcoming payment obligations.

Is Buy Now, Pay Later a good idea?

It can be helpful for short-term, planned purchases that fit within your budget. However, it may create financial strain if used frequently or without clear oversight. The value depends on how responsibly it’s used.

0 Comments