Introduction

Most people think that when a debt collector calls, they must pay immediately. This is exactly what the collection agency wants you to think. The reality is very different.

Collection agencies are not banks. They are private companies that buy old debts on spreadsheets for pennies on the dollar. Because they buy thousands of accounts at once, they often do not receive the original contracts or legal paperwork.

They are betting that you are too scared to ask for it. This guide teaches you how to use a single letter to demand proof, force them to follow the law, and potentially delete the debt without paying a cent.

Key Takeaways

- The Secret: Collectors often own your data, but not your contract.

- The Law: The FDCPA (Federal Law) gives you the right to demand “Validation.”

- The Power: If they cannot find the original paperwork, they cannot legally collect.

- The Method: You must send a certified letter within 30 days of first contact.

Disclaimer: This site contains affiliate links. If you make a purchase, we may earn a commission at no extra cost to you.

The Law Is On Your Side (The FDCPA)

You are not asking for a favor. You are exercising a federal right. The Fair Debt Collection Practices Act (FDCPA) is a law written to protect you from harassment.

The most powerful part of this law is the “Burden of Proof.”

In a court of law, the accuser must prove you are guilty. In debt collection, the collector must prove you owe the money. You do not have to prove you paid it. They must prove they own it.

The “Broken Chain” Theory

Look at the diagram above. When a bank sells your debt, it goes through a chain.

- Original Creditor (Bank): Has your contract with your signature.

- Debt Buyer A: Buys a spreadsheet with your name and balance.

- Debt Buyer B (The Collector): Buys the spreadsheet from Buyer A.

By the time the debt reaches the Collector who is calling you, the original paper contract is often lost. Without that paper, they have no legal standing. Your “Validation Letter” is simply asking them to show that paper. If the chain is broken, the debt must be deleted.

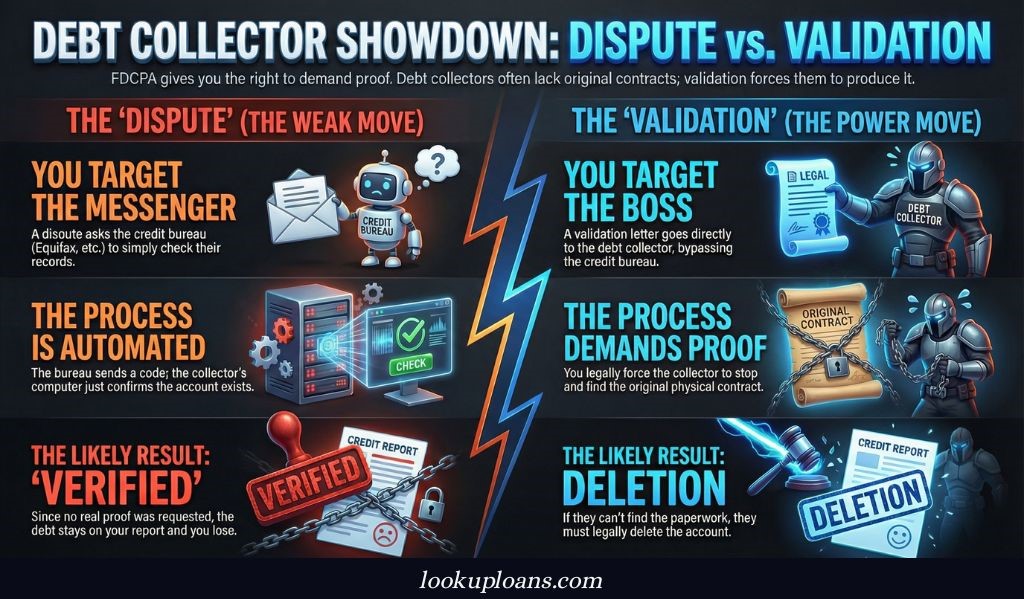

Dispute vs. Validation (Know The Difference)

Most people fail at credit repair because they fight the wrong enemy. They see a collection on their report and immediately log into Credit Karma or Experian to click “Dispute.”

This is a mistake. You are talking to the messenger, not the boss.

1. The “Dispute” (The Weak Move)

When you file a dispute with a Credit Bureau (like Equifax), you are just asking them to check their computer.

- The Process: Equifax sends a generic code to the collector asking, “Is this account real?”

- The Response: The collector checks their spreadsheet and says, “Yes, it’s real.”

- The Result: Equifax says, “Verified.” The debt stays. You lose.

2. The “Validation” (The Power Move)

When you send a Validation Letter, you bypass the Credit Bureau. You attack the Collector directly.

- The Process: You demand physical evidence (the contract, the license, the accounting).

- The Law: Under the FDCPA, once they receive this letter, they must stop trying to collect until they find the proof.

- The Result: If they cannot find the paper (which happens often), they must delete the account themselves.

The Strategy: Do not use the “Dispute” button online. That button is built to make you fail. It limits what you can say. Always use a Validation Letter first. If the collector fails to validate, then you show that failure to Equifax to get it removed.

Rule of Thumb: Validation attacks the root (the collector). Dispute attacks the fruit (the report). Kill the root, and the fruit dies.

Step-by-Step: How To Execute The Strategy

You cannot just write a note on a napkin and mail it. This is a legal procedure. You must follow strict rules to force them to respond.

Step 1: The 30-Day Rule

Time is your enemy. The FDCPA gives you 30 days from the first time a collector contacts you to request validation.

- The Window: If you send the letter inside this window, they must stop collecting immediately.

- The Risk: If you wait until day 31, they can keep calling you while they look for the proof.

- Action: Do not wait. As soon as you get a call or a letter, start writing.

Step 2: Certified Mail (The Weapon)

Never send a regular letter. Never send an email. Collectors ignore emails.

- The Method: Go to the Post Office. Ask for “Certified Mail with Return Receipt Requested.”

- The Cost: It costs about $7 or $8. This is the best money you will ever spend.

- The Proof: You will get a green card back in the mail with their signature on it. Keep this card. It is your legal proof that they received your demand. If they continue to call you after signing this card, you can sue them for $1,000.

Step 3: The Silence

Once they sign for the letter, the law requires them to stop.

- No Calls: They cannot phone you.

- No Letters: They cannot send you bills.

- The Investigation: They must pause everything and go find the paperwork. This silence can last weeks or months. Enjoy it.

Pro Tip: While you wait, do not talk to them on the phone. If they call, say: “I have sent you a validation request. Communicate only by mail.” Then hang up.

The 3 Possible Outcomes

After you send your letter, the clock starts ticking. The collector has to make a choice. They will usually do one of three things.

Outcome 1: The Fold (You Win)

This is the best-case scenario. The collector looks for the file and realizes they only have a spreadsheet line, not the original contract.

- The Reaction: They realize it costs too much money to find the paper.

- The Result: They send you a letter saying they are “closing the account” or “ceasing collection.” They delete the item from your credit report. You win.

Outcome 2: The Stall (The Trick)

This is very common. They know they don’t have the proof, so they try to fake it.

- The Reaction: They send you a computer printout that looks like a bill. It lists your name and the balance.

- The Trap: Most people think this is proof. It is not. A printout is just something they typed. It is not a legal contract.

- Your Move: You must write back immediately. Tell them: “This is just a bill. The FDCPA requires the original instrument of indebtedness. Send the contract with my signature or delete this.”

Outcome 3: The Proof (The Hard Truth)

Sometimes, the collector actually has the paperwork.

- The Reaction: They mail you a copy of the original credit card application with your wet-ink signature.

- The Result: The debt is valid. You cannot delete it based on a technicality.

- Your Move: Now you change strategies. Since they proved it, you negotiate a “Pay for Delete” settlement. You offer to pay 30% or 40% of the debt if they agree to remove it from your history.

Key Insight: Even if they validate the debt, you gained valuable time. You stopped the phone calls and forced them to show their hand.

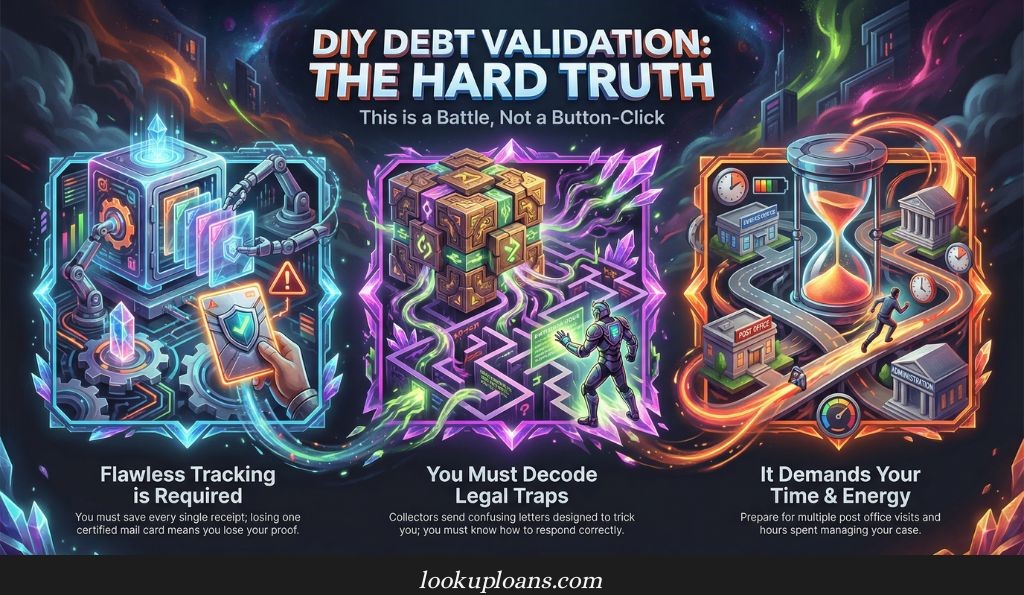

Warning: This Is Hard Work (The Pivot)

I want to be very clear with you. The “Paperwork Strategy” works, but it is not easy. It is a legal battle.

When you send a validation letter, you are starting a fight with a billion-dollar industry. Collection agencies hire expensive lawyers to find loopholes. They do not want to delete your debt. They want to scare you into paying.

The Reality of DIY Repair

If you choose to fight them alone, you must be perfect.

- The Tracking: You must save every receipt. If you lose one green card from the post office, you have no proof.

- The Follow-Up: They will send you confusing letters that sound legal but mean nothing. You must know how to read them.

- The Time: You will have to go to the post office multiple times. You will spend hours on hold.

The Choice Is Yours

You have two options to fix this problem.

Option 1: The “Do It Yourself” Path

You download the templates. You go to the post office. You track the dates. You fight the battle yourself. It is free, but it costs you time and stress.

Option 2: The “Expert” Path

You hire a team of professionals to do it for you. They talk to collectors all day. They know a fake letter when they see it. They know exactly when to threaten a lawsuit. It costs money, but it saves you from the headache.

Conclusion: Silence Is Not A Strategy

The worst thing you can do is ignore the phone calls. Ignoring them does not make the debt go away. It just makes the collector aggressive. They will eventually sue you, garnish your wages, or ruin your credit score for seven years.

You have the power to stop them, but you must take action. The law (FDCPA) gives you a weapon. It is up to you to pick it up and use it. Whether you do it yourself or hire a pro, the goal is the same: force them to prove it or delete it.

Ready To Fight? Choose Your Weapon

You now understand the game. You have two ways to play it.

Option 1: The “DIY” Warrior (Free)

If you have the time and discipline to track certified mail and fight the letters yourself, use our proven template.

⇒ Download The Free Debt Validation Letter Template (PDF)

Option 2: The “Done-For-You” Defense (Fast)

If you want an expert to handle the paperwork, talk to the collectors, and use the law to clean your report while you focus on your life, click below.

⇒ Click Here To Start Your Free Credit Repair Consultation

Frequently Asked Questions About Debt Validation

Will sending this letter “reset the clock” on my debt?

No. This is a common myth. “Resetting the clock” (restarting the Statute of Limitations) usually only happens if you make a payment or sign a document admitting you owe the money. A Validation Letter is not an admission of guilt. It is a request for information. It does not restart the timeline.

Can they sue me for asking for validation?

It is highly unlikely. In fact, asking for validation often protects you from a lawsuit. Lawyers know that if they sue you without having the original paperwork, they will lose in court. By asking for the paperwork early, you show them you are not an easy target. They usually prefer to sue people who ignore them, not people who fight back.

Does this work for Medical Bills?

Yes. Medical debt is often the easiest to remove. Hospitals sell debts to collectors with very little information because of privacy laws (HIPAA). Often, the collector has the amount but no details about the medical procedure. If they cannot prove exactly what the bill was for, they must delete it.

What if they validate the debt properly?

If they send you the original contract with your signature, do not panic. You have simply moved to “Phase 2.” Now that you know they have proof, you can negotiate. Call them and offer a “Pay for Delete” settlement. Tell them: “I will pay you 40% of the balance today if you agree to delete this account from my credit report.”

How long does this process take?

The law gives them 30 days to respond. However, the whole process can take 45 to 60 days.

- Days 1–5: You mail the letter.

- Days 5–35: They investigate.

- Days 35–45: They send a response (or delete it).

- Note: Be patient. Credit repair is not a microwave; it is a slow cooker.

0 Comments