Introduction

When you have a financial emergency, speed often feels like the only thing that matters. This urgency leads many people to choose predatory lenders that charge extreme fees. However, you have a better option.

Legitimate banks and Credit Unions offer personal loans to ITIN holders that are safe, legal, and affordable.

This guide explains how to find these lenders, what documents you need, and how to get funded without falling into a debt trap.

Key Takeaways

- The Math: A legitimate personal loan costs 10% to 35% in interest. A payday loan can cost 400% or more.

- Financial Proof: Lenders do not trust cash. They require 3 months of bank statements to prove your income.

- Your Asset: Unlike a “cash advance,” a real personal loan reports to the credit bureaus and builds your score.

- The Source: Start your search at local Credit Unions and Community Development Financial Institutions (CDFIs).

- Safety Warning: Never pay an “application fee” or “insurance fee” before you receive the money.

Disclaimer: This site contains affiliate links. If you make a purchase, we may earn a commission at no extra cost to you.

Why You Should Avoid Payday Loans (The Math)

The biggest mistake people make is choosing the “easiest” money. Payday lenders and “Title Loan” shops are easy because they do not check your background. But this convenience has a massive price tag.

The table below compares borrowing $2,000 for one year. Look at the difference in what you actually pay back.

| Feature | ITIN Personal Loan (The Smart Choice) | Payday / Title Loan (The Predatory Choice) |

|---|---|---|

| Annual Interest (APR) | 10% – 35% | 300% – 400%+ |

| Monthly Payment | Approx. $190 | Approx. $750 (Fees + Interest) |

| Total Interest Paid | $280 | $7,000+ |

| Result | You pay back $2,280 total. | You pay back $9,000+ total. |

| Credit Score | Goes Up (Builds history). | No Change (Does not report). |

The Economic Reality:

The payday lender charges you fees every two weeks. If you cannot pay the full amount, they add more fees. This creates a cycle where you are paying interest on top of interest.

A personal loan is different. You have a fixed monthly payment. You know exactly when the debt will be finished. It is cheaper, safer, and helps you qualify for better loans in the future.

Where To Find Legitimate ITIN Lenders

Most big banks will not give you a personal loan. Do not waste your time applying at huge national banks. They usually require a Social Security Number. You need to look for lenders who specifically serve the immigrant community.

1. Credit Unions (The Best Option)

These are non-profit organizations. Unlike big banks, they exist to serve their members, not to make a profit for investors.

- Why choose them: They have the lowest interest rates. They listen to your story instead of just looking at a computer screen.

- The Requirement: You usually have to live in their local area to join.

- Examples: Self-Help Federal Credit Union, Latino Community Credit Union, or Navy Federal (if you have family in the military).

2. Fintech Apps (The Fast Option)

These are technology companies. They use computer programs to scan your bank account and approve you quickly.

- Why choose them: Speed. You can often get approved in 24 hours using just your phone.

- The Trade-off: The interest rates are higher than a credit union. You pay for the convenience.

- Examples: Oportun, Upgrade, or Aura.

3. CDFIs (The Community Option)

A CDFI is a “Community Development Financial Institution.” These are organizations funded by the government to help people who cannot get normal bank loans.

- Why choose them: They are safe and fair. They often offer financial coaching to help you fix your credit.

- How to find them: They are often small and local. You must search for “CDFI near me” to find one in your city.

Warning: If a company is not a Credit Union, a known App, or a CDFI, be very careful. It might be a loan shark in disguise.

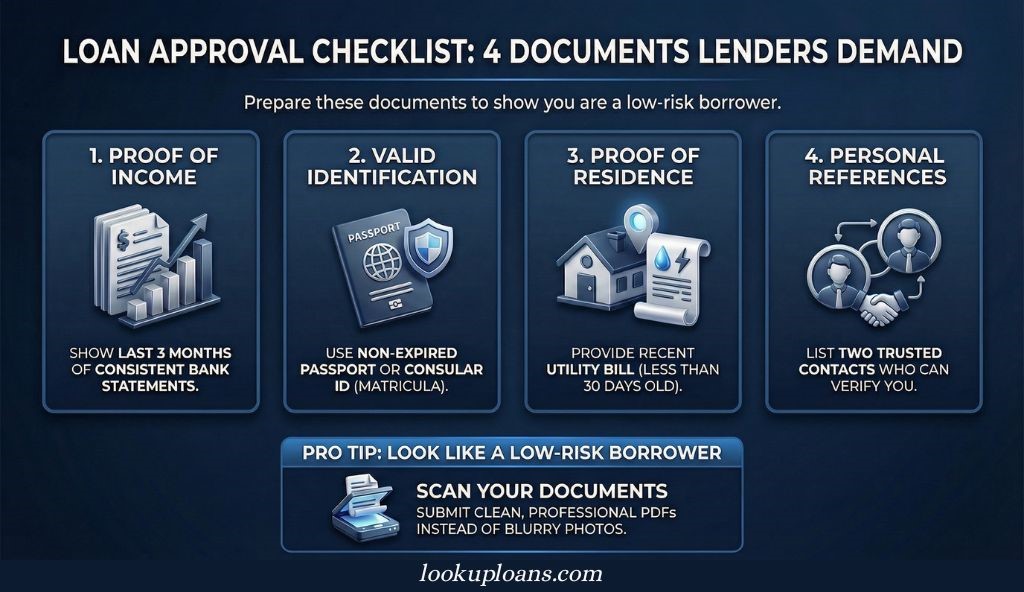

What Documents You Need For Loan Approval

Banks do not lend money on promises. They lend money on proof. Before you apply, gather these four specific documents. If any of them are missing or expired, your application will be rejected immediately.

1. Proof of Income (The Most Important Part)

This is where most people fail. If you get paid in cash and keep it in your pocket, the bank thinks you have zero income.

- The Rule: You need the last 3 months of bank statements.

- The Strategy: If you earn cash tips or side income, deposit it into your bank account every single week. This creates a paper trail that proves you make money.

- Warning: The deposits must be consistent. Large, random deposits look suspicious.

2. Valid Identification

You must prove who you are. Since you do not have a driver’s license, you need a federal ID.

- Acceptable IDs: A valid Passport or a Consular ID (Matricula Consular).

- The Trap: Check the expiration date. If it expires next month, renew it before you apply. A bank cannot accept an ID that is about to expire.

3. Proof of Residence

The lender needs to verify where you live.

- The Document: A utility bill (Electric, Water, or Gas) in your name.

- The Date: It must be less than 30 days old.

- The Match: The address on the bill must match the address on your application exactly.

4. Personal References

Many lenders (especially Fintech apps and Credit Unions) ask for the names and phone numbers of two people who know you.

- Why: If you stop paying and change your phone number, they will call these people to find you.

- Who to pick: Choose family members or close friends who answer their phones. Tell them in advance that a bank might call.

Pro Tip: Scan these documents into clear PDF files on your phone. Do not send blurry photos. A clean, professional application makes you look like a low-risk borrower.

How To Submit A Successful Loan Application

Applying for a loan is a process, not just a click. Follow these steps in order to give yourself the best chance of approval.

Step 1: Prepare Your Bank Account (30 Days Before)

Lenders look at your spending habits.

- The Action: For one month before you apply, do not let your bank balance drop to zero.

- The Reason: If they see “Overdraft Fees” or “Insufficient Funds” fees, they will think you are risky. Keep a small cushion of money in the account at all times.

Step 2: Check Your Rate (Soft Pull)

Most online lenders have a “Check Your Rate” button.

- The Action: Use this tool first. It does a “Soft Pull” on your credit report, which does not hurt your score.

- The Reason: It tells you if you are likely to be approved and what the interest rate will be. If the rate is too high, you can walk away without damage.

Step 3: Upload Clear Documents

When the application asks for your proof, do not be lazy.

- The Action: Use a free scanner app on your phone (like Adobe Scan) to turn your papers into clean PDFs.

- The Reason: Blurry photos of crumpled paper look unprofessional. A clean PDF shows you are serious and organized.

Step 4: Answer the Phone

After you click submit, the bank might call you to verify your identity.

- The Action: If you see a number you don’t know, answer it.

- The Reason: If they call and you don’t pick up, they might pause or cancel your application for security reasons.

Step 5: Set Up Auto-Pay

Once you are approved, link your bank account for automatic payments.

- The Benefit: Many lenders will lower your interest rate by 0.25% or 0.50% just for doing this. It saves you money and ensures you never miss a payment.

How To Identify Predatory Loan Scams

There are criminals who pretend to be legitimate lenders to steal from people who are desperate for cash. Because ITIN holders often feel excluded by major banks, they are common targets for these schemes.

A real bank operates based on risk and law. A scammer operates based on pressure and fees. If you see any of the following three signs, stop the conversation immediately.

1. The “Upfront Fee” Trap

This is the most common sign of a fake lender.

- The Scam: They tell you your loan for $5,000 is approved, but you must first send them $200 for “Insurance,” “Taxes,” or a “Processing Fee.”

- The Reality: Legitimate lenders never ask you to send them money. If there is a fee, they deduct it from the loan amount after they send you the funds.

- The Rule: Money flows from the bank to you. If they ask for money to flow from you to the bank first, it is a theft.

2. The “Guaranteed Approval” Promise

- The Scam: You see an advertisement that says: “Bad Credit? No Job? No Problem! 100% Guaranteed Approval for ITINs.”

- The Reality: In the United States, it is illegal for a lender to guarantee a loan without checking your ability to pay. Every real bank must check your income.

- The Rule: If they promise to lend you money without asking for your bank statements, they are lying.

3. The “Unusual Payment” Request

- The Scam: The lender asks you to pay your fee or deposit using a Gift Card (like iTunes or Google Play), Western Union, or Cryptocurrency.

- The Reality: Real financial institutions use bank transfers (ACH) or checks. They do not have accounts on crypto exchanges or use gift cards.

- The Rule: No bank will ever ask to be paid in gift cards.

Conclusion: The Loan Is A Test

Getting a personal loan is about more than just money. It is a test of your financial discipline.

When you borrow from a legitimate lender and pay it back on time, you are sending a signal to the entire banking system. You are proving that you are trustworthy. This record stays on your credit report for years.

If you handle this small loan well, the banks will be ready to trust you with bigger things later like a car loan or a mortgage for a house. Use this opportunity to fix your emergency, but also use it to build your reputation.

What to do next: Now that you understand how to manage short-term debt, you are ready to look at the long-term goal. Read our Master Guide to ITIN Loans to learn how to prepare for buying a home.

Frequently Asked Questions About ITIN Personal Loans

Can I get a loan if I have no credit history at all?

Yes. Many Fintech lenders (like Oportun) and local Credit Unions use “Alternative Data.” Instead of looking at a FICO score, they look at your bank account, your rent payments, and your utility bills to see if you are responsible.

How long does it take to get the money?

It depends on the lender.

- Fintech Apps: 24 to 48 hours.

- Credit Unions: 3 to 7 business days (because they often review applications manually).

- Strategy: If you need money instantly, an app is faster, but a Credit Union is cheaper.

Do I need to own a car to get a personal loan?

No. A “Personal Loan” is usually unsecured. This means you do not have to give them your car title or house deed as collateral. They lend you money based on your income and your promise to pay. This is much safer than a “Title Loan,” where you risk losing your vehicle.

Will this loan affect my immigration status?

No. Borrowing money from a private bank is a private contract. It is not a government benefit (like welfare), so it does not count as a “Public Charge.” However, always pay your debt. Leaving unpaid debts can lead to lawsuits, which create legal headaches you do not need.

0 Comments