Introduction

Finding a DSCR loan lender is not difficult. Finding one that consistently executes well for real estate investors is harder.

Many lenders advertise DSCR programs, but operate with traditional underwriting habits. That often leads to slow timelines, unclear requirements, and last-minute conditions that disrupt deals.

For investors, the difference is not theoretical. A lender’s speed, clarity, and consistency directly affect whether a deal closes or falls apart.

This guide focuses on that distinction. Instead of listing lenders based on marketing claims, it evaluates how they perform in practice. The goal is to help you identify which lenders align with your strategy, your deal type, and your timeline.

Key Takeaways

- Not all DSCR lenders operate with investor-focused underwriting, even if they market that way.

- Execution matters more than headline rates. Speed, clarity, and consistency drive outcomes.

- The right lender depends on your deal type, not just your credit or DSCR ratio.

- Delays and unclear requirements are the most common reasons deals fail.

- Strong lenders provide predictable timelines, transparent terms, and consistent underwriting.

Disclaimer: This site contains affiliate links. If you make a purchase, we may earn a commission at no extra cost to you.

What Makes a Strong DSCR Loan Lender

Not all DSCR lenders operate the same way. Many offer similar products on the surface, but differ significantly in how they underwrite, communicate, and execute.

A strong DSCR lender is defined less by marketing claims and more by how consistently they close deals under real conditions.

Investor-Focused Underwriting

A core distinction is how the lender evaluates risk.

Strong DSCR lenders prioritize:

- Property cash flow

- Rental income consistency

- Deal structure

They avoid defaulting to traditional borrower-based analysis unless necessary. This keeps the process aligned with how investment properties are actually evaluated.

Clear and Predictable Requirements

Clarity upfront reduces friction later.

Reliable lenders define:

- Minimum DSCR thresholds

- Accepted property types

- Rental income methodology

- Reserve requirements

This allows investors to structure deals correctly before entering underwriting.

Consistent Execution Speed

Speed is not just about being fast once. It is about being predictable.

Strong lenders:

- Provide timelines they can maintain

- Move efficiently from application to closing

- Avoid unnecessary delays during underwriting

Inconsistent timelines are often more damaging than slow ones.

Transparent Pricing and Terms

A strong lender provides full visibility into loan structure early in the process.

This includes:

- Interest rate

- Origination fees

- Prepayment penalties

- Reserve requirements

Transparency reduces the risk of last-minute changes that can disrupt closing.

Flexibility Within Defined Boundaries

DSCR lending is not one-size-fits-all.

Effective lenders offer flexibility in areas such as:

- Property types

- Ownership structures (including LLCs)

- Loan structures (fixed, adjustable, interest-only)

At the same time, they maintain clear boundaries. Flexibility without structure leads to inconsistency.

Alignment With Investor Strategy

The strongest lenders understand how investors operate.

They recognize:

- Portfolio growth strategies

- Short-term vs long-term rental models

- The importance of repeat transactions

This alignment improves communication and reduces unnecessary friction.

Key Insight

A strong DSCR lender is not defined by how quickly they say yes.

They are defined by how consistently they move from approval to closing without introducing new uncertainty.

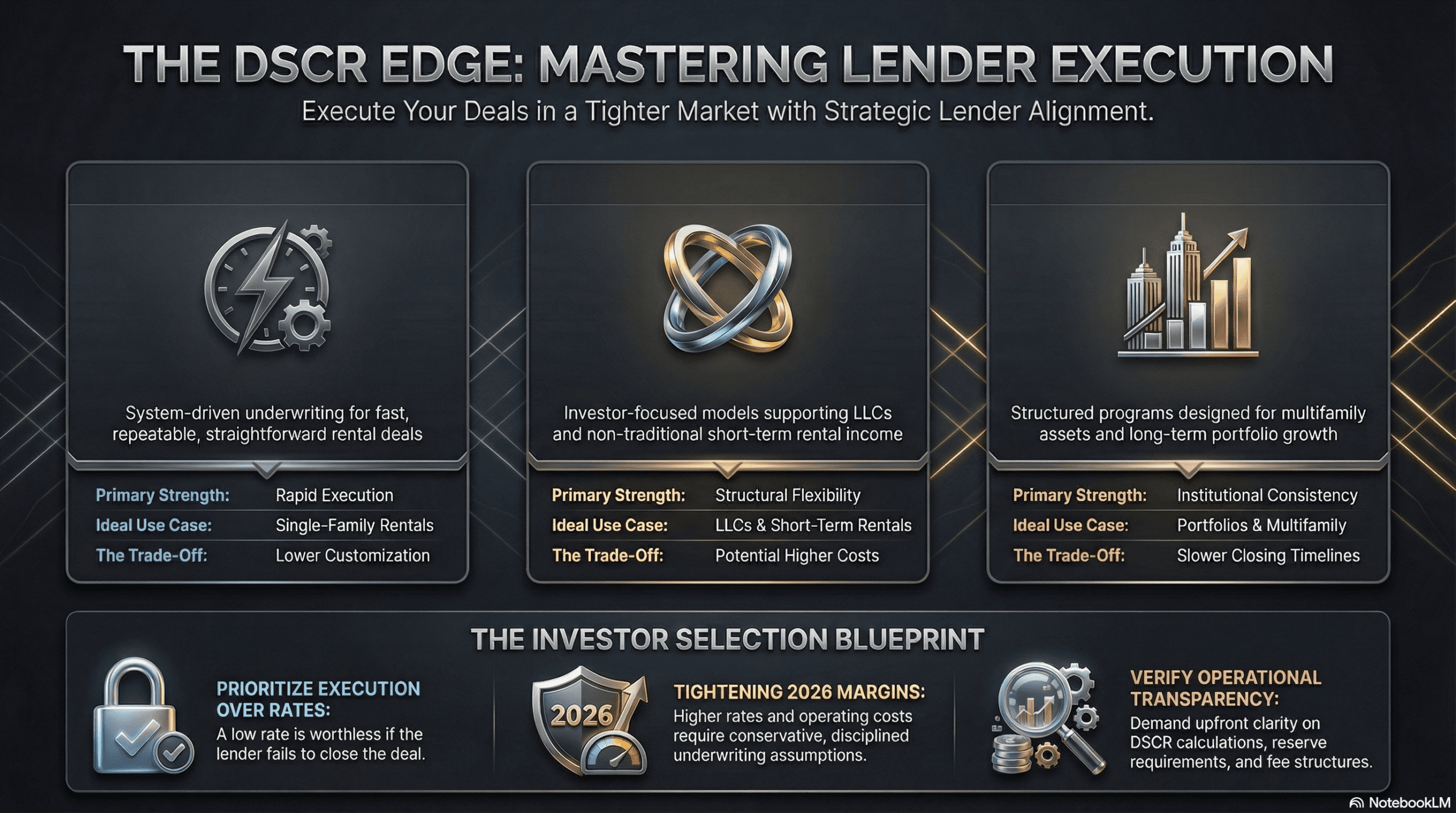

Best DSCR Loan Lenders (Who They Fit and Where They Perform)

Not all DSCR lenders are built for the same type of investor or deal.

Some prioritize speed and simplicity. Others focus on structure and scalability. The difference is not just in pricing, but in how each lender handles underwriting, communication, and execution.

The lenders below are not ranked. Each is included based on where they tend to perform well and the type of investor they align with.

Kiavi

Where they perform well

Kiavi is structured for speed and operational efficiency. Their platform is designed to move standard rental deals through underwriting with minimal friction.

They are most effective when:

- The property is straightforward

- The income profile is predictable

- The deal does not require customization

Their process is heavily system-driven, which helps maintain consistency across transactions.

Where they may be limited

This structure can reduce flexibility.

Deals involving:

- Complex ownership structures

- Mixed-use properties

- Non-standard scenarios

may not fit as easily within their process.

Best fit

Investors who prioritize:

- Fast execution

- Repeatable deal structures

- Consistent process over customization

Visio Lending

Where they perform well

Visio Lending is aligned with investor-focused underwriting. Their programs are designed around property income rather than borrower income.

They tend to work well for:

- LLC-owned properties

- Short-term rental strategies (with documentation)

- Investors scaling portfolios

Their structure supports flexibility in ownership and income types.

Where they may be limited

This flexibility can come with stricter evaluation in other areas.

Expect:

- Careful appraisal review

- Conservative assumptions on income

- Potentially higher pricing compared to more standardized lenders

Best fit

Investors who need:

- Flexibility in structure

- Support for non-traditional income

- Alignment with portfolio-based strategies

Lima One Capital

Where they perform well

Lima One Capital operates with a more structured, institutional approach.

They tend to perform well for:

- Portfolio-focused investors

- Multifamily properties

- Investors planning multiple transactions over time

Their underwriting is consistent and designed for scalability.

Where they may be limited

This structure can result in:

- Longer timelines compared to faster lenders

- More defined requirements, especially for newer investors

Best fit

Investors who value:

- Predictability

- Structured lending programs

- Long-term portfolio growth support

Key Insight

Each lender operates within a different model.

The goal is not to find the “best” lender overall, but the one that aligns with how your deal is structured and how you operate as an investor.

Side-by-Side Comparison of Top DSCR Lenders

A direct comparison helps clarify how each lender differs in execution, flexibility, and ideal use case.

This is not a ranking. It is a fit-based comparison to support decision-making.

| Factor | Kiavi | Visio Lending | Lima One Capital |

|---|---|---|---|

| Execution Speed | Fast and system-driven | Moderate, depends on deal complexity | Slower, more structured timelines |

| Underwriting Style | Standardized, process-focused | Investor-focused, flexible | Institutional, consistency-focused |

| DSCR Flexibility | Works best with clean, strong DSCR deals | More adaptable across scenarios | Defined thresholds, less flexible |

| Property Types | Primarily SFR and small multifamily | SFR, STR, and LLC-owned properties | SFR, multifamily, some construction |

| Ownership Structure | Simpler structures preferred | Strong support for LLCs | Supports entities with structured requirements |

| Best Use Case | Fast, repeatable rental deals | Flexible investor strategies and scaling | Long-term portfolio building |

| Trade-Off | Less flexibility | Potentially higher cost or tighter scrutiny | Slower execution |

How to Use This Comparison

Each lender represents a different operating model.

- Choose Kiavi when speed and simplicity are the priority

- Choose Visio Lending when flexibility and structure matter

- Choose Lima One Capital when consistency and long-term scaling are the goal

The decision should reflect how your deal is structured, not just which lender appears strongest overall.

Key Insight

A side-by-side comparison highlights one reality:

Differences between DSCR lenders are operational, not just financial.

Execution style often has a greater impact on your outcome than small differences in rates.

DSCR Lending in 2026: What Investors Need to Know

DSCR loans still follow the same structure, but the lending environment has changed. Current market conditions affect how deals are evaluated, structured, and approved.

Understanding these shifts is necessary to avoid mispricing deals or overestimating qualification.

Higher Interest Rates Are Tightening Margins

Borrowing costs remain elevated compared to previous years.

Higher rates increase monthly loan payments, which reduces DSCR. Deals that previously met lender thresholds may now fall closer to minimum requirements.

This makes deal structure more sensitive. Small changes in price, rate, or leverage can determine whether a deal qualifies.

Operating Costs Are Reducing Cash Flow

Property-level expenses have increased in many markets.

Key pressures include:

- Insurance premiums

- Property taxes

- Maintenance costs

These reduce Net Operating Income, which directly impacts DSCR. Lenders are placing more emphasis on realistic expense assumptions rather than optimistic projections.

Short-Term Rental Income Is Treated More Conservatively

Lenders are applying more scrutiny to short-term rental income.

In many cases, they will:

- Require documented income history

- Apply conservative income estimates

- Use long-term rental comps instead of projected short-term revenue

This reduces reliance on projected performance and favors proven income stability.

Lenders Are More Selective

Compared to earlier lending cycles, many DSCR lenders are applying tighter standards.

This may include:

- Higher reserve requirements

- More detailed appraisal reviews

- Stricter validation of rental income

Approval is still achievable, but the margin for error is smaller.

Key Insight

In current market conditions, DSCR lending rewards disciplined underwriting. Conservative assumptions and strong deal structure are more important than speed alone.

What to Watch Out for When Choosing a DSCR Loan Lender

Most DSCR lenders will not reject a deal immediately. More often, problems appear during the process through delays, unclear requirements, or unexpected changes.

These issues can disrupt timelines and create unnecessary risk. Identifying them early is critical.

Inconsistent Underwriting Standards

Some lenders advertise DSCR programs but apply traditional lending logic during underwriting.

This can show up as:

- New documentation requests mid-process

- Shifting qualification criteria

- Unclear DSCR calculations

This creates uncertainty and slows execution.

What to do:

Confirm DSCR requirements, income calculation methods, and documentation expectations before applying.

Unclear or Changing Timelines

Execution speed matters, but consistency matters more.

Warning signs include:

- Delays in issuing initial terms

- Vague answers about closing timelines

- Frequent timeline revisions

These issues often indicate operational inefficiency.

What to do:

Ask for a typical timeline from application to closing, and what factors commonly cause delays.

Lack of Pricing Transparency

Incomplete or delayed fee disclosure can affect deal viability.

This may include:

- Origination fees not clearly defined

- Prepayment penalties introduced late

- Reserve requirements not disclosed upfront

These elements affect total cost and should be known early.

What to do:

Request a full breakdown of fees and loan structure before committing to a lender.

Limited Flexibility on Property or Structure

Some lenders operate within narrow guidelines.

This can affect:

- Short-term rental properties

- Multifamily units

- LLC or entity ownership

If the lender’s criteria do not align with your deal, approval may fail late in the process.

What to do:

Confirm property eligibility and ownership structure at the start.

Poor Communication

Communication quality often reflects execution quality.

Warning signs include:

- Slow or unclear responses

- Inconsistent answers

- Lack of a defined point of contact

These issues tend to persist throughout the transaction.

What to do:

Evaluate responsiveness before applying. Early communication patterns usually continue through closing.

Key Insight

Most DSCR loan issues are not caused by rejection. They are caused by friction during execution.

Choosing a lender with clear processes and consistent communication reduces that risk.

How to Choose the Right DSCR Loan Lender for Your Deal

There is no single “best” DSCR lender. The right choice depends on how your deal is structured and how you operate as an investor.

The goal is not just approval. It is selecting a lender who can execute consistently within your timeline and strategy.

Match the Lender to the Deal Type

Each lender has a defined range of deals they handle well.

Some are optimized for:

- Standard long-term rentals

- Single-family properties

Others are better suited for:

- Short-term rentals

- Multifamily properties

- Portfolio-level strategies

Choosing a lender outside their typical scope increases the risk of delays or denial.

Ask Direct Questions Before Applying

Clarity early prevents issues later.

Key questions to ask:

- What DSCR ratio do you require?

- How do you calculate rental income?

- Do you support short-term rentals or only long-term leases?

- Do you lend to LLCs or individuals only?

- What is your typical closing timeline?

The quality and consistency of these answers will indicate how the lender operates.

Evaluate Execution, Not Just Rates

Interest rate is only one part of the decision.

Execution factors often have greater impact:

- Time to close

- Documentation requirements

- Flexibility during underwriting

A slightly higher rate may be acceptable if it comes with faster and more predictable execution.

Assess Long-Term Fit

For investors planning multiple transactions, lender consistency matters.

Consider whether the lender:

- Supports repeat transactions

- Maintains consistent underwriting standards

- Provides a reliable point of contact

A stable lending relationship can reduce friction over time.

Balance Speed and Structure

Different lenders prioritize different strengths.

- Faster lenders may offer efficiency but less flexibility

- More structured lenders may provide consistency but slower timelines

The right balance depends on your experience level and deal complexity.

Key Insight

Choosing a DSCR lender is a strategic decision. The best choice aligns with your deal structure, timeline, and long-term investment approach.

Conclusion

A DSCR loan is only as effective as the lender behind it.

While rates and terms matter, they do not determine whether a deal closes smoothly. Execution does. The ability to move from application to funding without delays, confusion, or changing requirements has a direct impact on investment outcomes.

The lenders outlined in this guide operate with different strengths. Some prioritize speed and simplicity. Others focus on flexibility or long-term structure. None are universally better. The right choice depends on how your deal is built and how you operate as an investor.

In current market conditions, this alignment matters more than ever. Tighter margins, higher costs, and more selective underwriting leave less room for error. A lender who communicates clearly and executes consistently reduces that risk.

The decision should be made with a clear objective:

- Match the lender to the deal

- Prioritize execution over headline rates

- Choose consistency over promises

A well-aligned lender does more than fund a transaction. It supports repeatable, predictable growth.

Frequently Asked Questions About DSCR Loan Lenders

Do all DSCR lenders have the same requirements?

No. While most lenders use DSCR as the core metric, their requirements vary in how they calculate income, set minimum ratios, and define reserves. These differences can affect both approval and loan terms.

What DSCR ratio do most lenders require?

Most lenders look for a DSCR between 1.20 and 1.25 or higher. Some may allow lower ratios, but this usually comes with higher rates, larger down payments, or stricter conditions.

How do lenders evaluate rental income for DSCR loans?

Lenders typically use lease agreements or market rent appraisals. Some may accept short-term rental income, but often apply conservative estimates or require documented history.

Can DSCR lenders work with LLCs or entity ownership?

Many DSCR lenders support LLC ownership, especially for investors building portfolios. However, some still require a personal guarantee or have specific structuring rules.

What causes delays with DSCR lenders?

Delays usually come from unclear requirements, slow communication, or appraisal issues. Lenders with inconsistent processes are more likely to create friction during underwriting.

How long does it typically take to close with a DSCR lender?

Closing timelines usually range from 2 to 4 weeks, depending on the lender’s process and the complexity of the deal. More structured lenders may take longer.

Does the lowest interest rate mean the best lender?

Not necessarily. Execution, speed, and consistency often have a greater impact on the deal than small differences in rate. A slower lender can cost more in missed opportunities.

0 Comments