Introduction

Real estate investors often run into the same problem. Traditional mortgages are built around personal income, not property performance. That creates friction for self-employed borrowers, portfolio investors, and anyone whose income does not fit a standard W-2 profile.

A DSCR loan approaches the decision differently. Instead of focusing on your personal earnings, it evaluates whether the property itself generates enough income to support the loan.

This guide explains how DSCR loans work, what lenders actually look for, and when this financing strategy makes sense. By the end, you will understand how to evaluate a DSCR deal with clarity and avoid the common mistakes that lead to rejection or poor terms.

Key Takeaways

- A DSCR loan is based on the property’s income, not your personal income.

- The key metric is the Debt Service Coverage Ratio (DSCR), which compares rental income to loan payments.

- Most lenders look for a DSCR of 1.20 to 1.25 or higher for approval.

- These loans are commonly used by real estate investors and self-employed borrowers.

- DSCR loans offer flexibility, but usually come with higher interest rates and larger down payments.

- Property quality and rental income stability are critical to approval.

- Understanding how lenders calculate DSCR can directly impact your approval and loan terms.

Disclaimer: This site contains affiliate links. If you make a purchase, we may earn a commission at no extra cost to you.

What a DSCR Loan Is

A DSCR loan is a type of real estate investment loan that qualifies borrowers based on a property’s income rather than their personal income.

DSCR stands for Debt Service Coverage Ratio. It measures whether a property generates enough cash flow to cover its loan payments.

Traditional mortgages focus on the borrower. Lenders review your job history, tax returns, and debt-to-income ratio. The goal is to determine whether you can afford the loan.

A DSCR loan flips that approach. The lender evaluates the property instead. The central question becomes: Does this property produce enough income to pay for itself?

If the answer is yes, the loan is more likely to be approved. If the answer is no, approval becomes difficult regardless of your personal income.

How DSCR Loans Differ from Traditional Mortgages

The distinction is structural, not cosmetic.

- Traditional loans rely on personal income and employment stability

- DSCR loans rely on property income and cash flow performance

This makes DSCR loans especially relevant for:

- Real estate investors building rental portfolios

- Self-employed borrowers with variable income

- Individuals whose tax returns do not reflect true cash flow

However, this does not mean “no qualification.” Lenders still evaluate risk through:

- Property income consistency

- Credit profile

- Down payment size

- Cash reserves

The difference is what carries the most weight. In DSCR lending, the property’s ability to generate income drives the decision.

The Core Idea

A DSCR loan is built on a simple principle:

- If the asset can support the debt, the deal works.

Everything else supports that evaluation.

Why DSCR Loans Matter

DSCR loans exist because traditional mortgage standards do not align well with how real estate investing actually works.

Most conventional loans evaluate borrowers based on personal income stability. That model works for salaried employees, but it breaks down for investors. Rental properties are income-producing assets, yet traditional underwriting often ignores that income or discounts it heavily.

This creates a gap. Investors may own profitable properties but still struggle to qualify for additional financing.

DSCR loans address that gap directly.

The Problem with Traditional Lending

Traditional underwriting focuses on risk at the borrower level. Lenders ask:

- How stable is your income?

- How long have you been employed?

- What does your tax return show?

For investors, these questions can produce misleading answers.

Rental income may be reduced by write-offs. Business income may fluctuate. Portfolio growth may increase debt-to-income ratios even when properties perform well.

As a result, strong investors can appear weak on paper.

The Shift to Asset-Based Lending

DSCR loans change the evaluation model from borrower-focused to asset-focused.

Instead of asking whether you can personally cover the loan, lenders ask whether the property can sustain itself.

This aligns financing with the core principle of real estate investing:

Each property should stand on its own financial performance.

When that condition is met, scaling becomes more practical. Investors can acquire additional properties without being constrained by personal income limits.

Why This Matters for Investors

This structure creates three practical advantages:

- It allows investors to qualify based on deal quality, not income structure

- It removes the bottleneck created by debt-to-income ratios

- It supports portfolio growth when properties generate consistent cash flow

However, this also introduces discipline. Poor-performing properties are harder to finance under DSCR guidelines. The model rewards strong deals and exposes weak ones.

The Trade-Off

DSCR loans are not a loophole. They are a different risk model.

Because lenders rely heavily on property performance, they often offset that risk with:

- Higher interest rates

- Larger down payments

- Stricter property standards

This is the cost of flexibility. Investors gain access to financing without traditional income verification, but they must present stronger deals.

How DSCR Loans Work

At the core of every DSCR loan is a single calculation. This number determines whether a deal is viable in the eyes of a lender.

This formula compares a property’s income to its debt obligations. The result shows whether the property can support the loan.

Breaking Down the Formula

To understand how lenders evaluate a deal, you need to understand both parts of the equation.

Net Operating Income (NOI)

This is the property’s income after operating expenses, but before loan payments.

NOI typically includes:

- Rental income

- Minus property management

- Minus maintenance

- Minus taxes and insurance

It does not include mortgage payments.

Debt Service

This is the total cost of the loan.

It includes:

- Principal

- Interest

- Property taxes

- Insurance

This is often referred to as PITIA in lending.

What the DSCR Number Means

The result of the formula is a ratio. That ratio tells the lender how safe the deal is.

| DSCR | Meaning |

| Below 1.0 | Property does not generate enough income to cover the loan |

| 1.0 | Property breaks even |

| 1.20 – 1.25 | Meets most lender minimums |

| 1.50+ | Strong cash flow, lower perceived risk |

A higher DSCR indicates a larger income buffer. This reduces risk from vacancies, repairs, or market changes.

How Lenders Use DSCR

Lenders do not look at DSCR in isolation. They use it as the primary filter, then adjust terms based on risk.

- Higher DSCR → better rates and lower reserves

- Lower DSCR → higher rates and stricter conditions

If the DSCR falls below a lender’s threshold, the deal may be denied or require a larger down payment.

Real-World Example

Consider a rental property generating $2,500 per month.

After expenses, the Net Operating Income is $2,000 per month.

The total monthly loan payment is $1,500.

The DSCR is:

- 2,000 ÷ 1,500 = 1.33

This means the property generates 33% more income than required to cover the debt.

From a lender’s perspective, this is a stable deal. There is enough margin to absorb minor disruptions without default risk increasing significantly.

The Key Insight

DSCR loans reduce lending decisions to a clear financial test:

Does the property produce enough income to support the debt with a margin of safety?

If the answer is yes, the deal moves forward. If not, the structure of the deal must change.

Use our free DSCR loan calculator to instantly see how your numbers stack up and whether your deal has a shot at approval.

DSCR Loan Requirements (Key Components Lenders Evaluate)

DSCR loan requirements go beyond a single number. Lenders evaluate several key factors to determine risk and loan terms.

Each component affects your approval, loan terms, and flexibility.

DSCR Ratio (Primary Factor)

This is the foundation of the loan.

Most lenders look for a minimum DSCR between 1.20 and 1.25. A higher ratio improves your position.

- Higher DSCR → stronger deal, better terms

- Lower DSCR → higher risk, stricter conditions

If the ratio is too low, lenders may require:

- A larger down payment

- Additional reserves

- Or they may decline the deal entirely

This is the most important metric in DSCR lending.

Credit Score (Risk Indicator)

Even though income is not verified, your credit profile still matters.

Typical expectations:

- 620 to 680 minimum for most lenders

- 700+ for stronger pricing and flexibility

Credit does not drive the approval, but it influences:

- Interest rate

- Loan fees

- Reserve requirements

A stronger credit profile reduces perceived borrower risk.

Down Payment (Equity Buffer)

Lenders require you to have capital invested in the deal.

Common range:

- 20% to 25% down

This creates a margin of safety. If the property underperforms, your equity reduces the lender’s exposure.

Lower down payments are sometimes available, but they usually result in:

- Higher interest rates

- Tighter underwriting

- Additional conditions

More equity generally improves approval odds.

Cash Reserves (Stability Measure)

Reserves show that you can sustain the property during income disruptions.

Typical requirement:

- 3 to 6 months of mortgage payments

These funds act as a buffer against:

- Vacancy

- Unexpected repairs

- Market fluctuations

Reserves do not need to be held in cash alone. Many lenders accept:

- Savings accounts

- Brokerage accounts

- Retirement funds

This component reinforces the deal’s resilience.

Property Type (Eligibility Filter)

Not all properties qualify for DSCR loans.

Lenders prefer properties that produce stable, predictable income:

- Single-family rentals

- Condos and townhomes

- 2 to 4 unit multifamily properties

Properties that often face restrictions:

- Vacant land

- Fix-and-flip projects

- Heavy renovation properties

Some lenders allow short-term rentals, but many apply stricter guidelines or require documented income history.

The property must function as a reliable income-producing asset.

How These Components Work Together

These factors do not operate independently. Lenders evaluate them as a combined risk profile.

For example:

- A high DSCR can offset a lower credit score

- A larger down payment can compensate for a borderline DSCR

- Strong reserves can strengthen an otherwise average deal

Approval is based on the overall balance, not a single metric.

Key Insight

A DSCR loan is built on layered risk evaluation:

- The DSCR ratio determines viability

- The supporting factors determine loan quality

Understanding this interaction allows you to structure stronger deals and negotiate better terms.

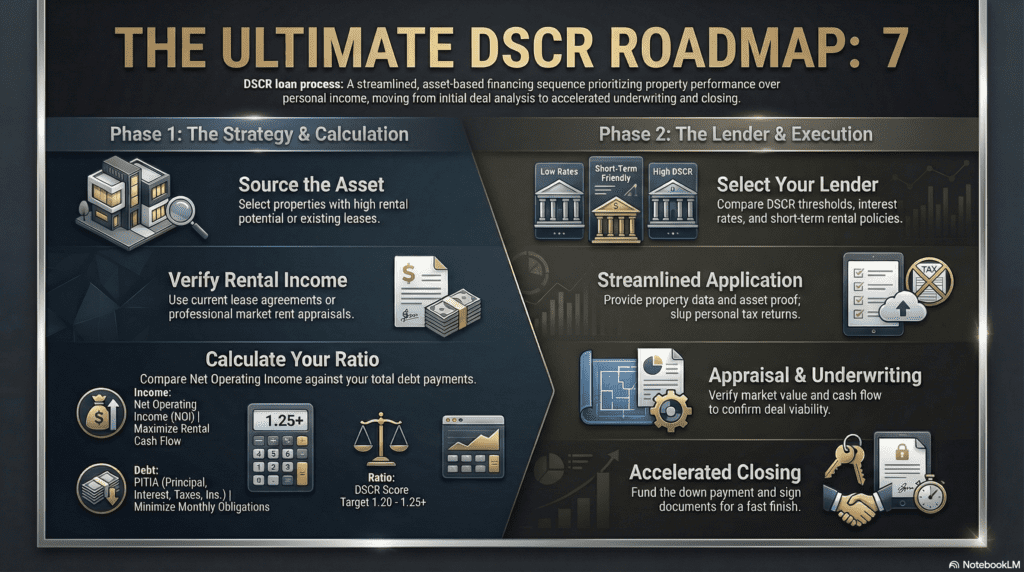

How the DSCR Loan Process Works (Step-by-Step)

Understanding the structure is not enough. You need to see how a DSCR loan actually unfolds from deal to closing.

This process is more streamlined than traditional lending, but each step still requires precision.

1. Identify a Cash-Flowing Property

Everything starts with the deal.

You select a property with strong rental potential. This can be:

- An existing rental with a lease in place

- A market-rent-supported acquisition

At this stage, the focus is simple:

Does this property have the potential to generate consistent income?

2. Estimate Rental Income

Next, you determine how much income the property can produce.

Lenders will verify this using:

- Current lease agreements, or

- Market rent appraisals

Accuracy matters here. Overestimating rent is one of the fastest ways to weaken a deal.

3. Calculate the DSCR

With income and expenses defined, you calculate the DSCR.

You compare:

- Net Operating Income

- Against total debt payments

This step determines whether the deal meets minimum lender thresholds.

If the DSCR is too low, you may need to:

- Increase your down payment

- Adjust the purchase price

- Improve projected income

4. Choose a DSCR Lender

Not all lenders operate the same way.

At this stage, you compare:

- Minimum DSCR requirements

- Interest rates and fees

- Property eligibility rules

- Treatment of short-term rental income

Selecting the right lender can directly impact approval speed and loan terms.

5. Submit the Application

The application process is more streamlined than traditional loans.

You typically provide:

- Property details

- Estimated or actual rental income

- Credit authorization

- Asset documentation for reserves and down payment

Personal income documents are generally not required, but financial verification still exists.

6. Appraisal and Underwriting

The lender orders an appraisal to confirm:

- Property value

- Market rental income

Underwriting then evaluates:

- DSCR ratio

- Credit profile

- Reserves

- Overall deal structure

This is where the deal is either approved, adjusted, or declined.

7. Approval and Closing

Once approved, the loan moves to closing.

Final steps include:

- Signing loan documents

- Funding the down payment

- Completing the purchase

Closings are often faster than traditional loans because the documentation burden is lower.

What This Process Reveals

DSCR lending is not simpler. It is more focused.

- Traditional loans focus on the borrower

- DSCR loans focus on the deal

If the numbers are strong, the process moves efficiently. If the numbers are weak, the process stops quickly.

Key Insight

A DSCR loan rewards preparation.

The clearer your numbers are before applying, the smoother the process becomes.

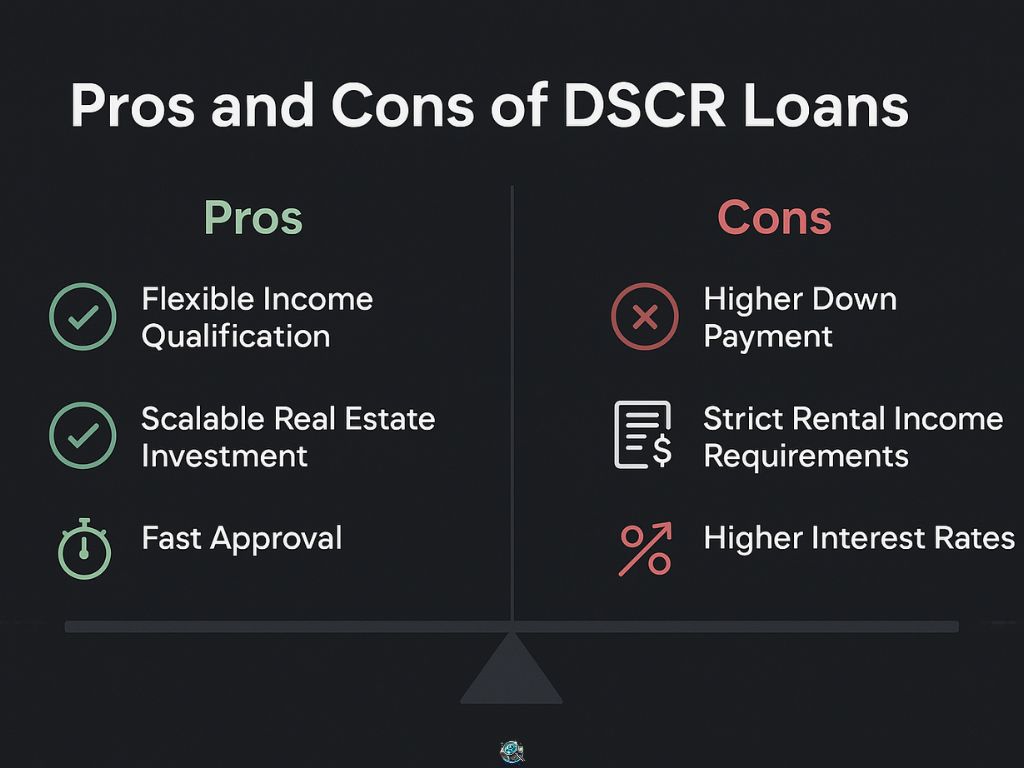

Pros and Cons of DSCR Loans

DSCR loans offer a different way to access real estate financing. They remove some barriers, but they introduce new constraints.

Understanding both sides is critical before using this strategy.

Advantages of DSCR Loans

No Personal Income Verification

The primary advantage is structural.

You are not required to provide:

- W-2s

- Tax returns

- Employer verification

Approval is based on the property’s ability to generate income. This makes DSCR loans accessible to borrowers with non-traditional income profiles.

Faster Approval and Closing

With fewer personal documents required, the process is typically more efficient.

This can be valuable in competitive markets where speed affects deal outcomes.

Scalable for Portfolio Growth

Traditional loans limit borrowers through debt-to-income ratios.

DSCR loans remove that constraint. Each property is evaluated independently, which allows investors to expand their portfolios more efficiently, assuming each asset performs.

Flexible Loan Structures

Many DSCR lenders offer options such as:

- Interest-only periods

- Fixed or adjustable rates

- Prepayment flexibility (varies by lender)

These structures can be aligned with different investment strategies.

Limitations of DSCR Loans

Higher Interest Rates

DSCR loans typically carry higher rates than conventional mortgages.

This reflects the lender’s reliance on property performance rather than personal income stability.

Larger Down Payments

Most DSCR loans require 20% to 25% down.

This increases the upfront capital required to enter or scale.

Strict Cash Flow Requirements

If the property does not meet minimum DSCR thresholds, the deal becomes difficult.

Marginal deals often result in:

- Worse loan terms

- Additional reserve requirements

- Or denial

Property Restrictions

Not all real estate qualifies.

Properties that lack stable income or require significant renovation are often excluded. The loan is designed for income-producing assets, not speculative projects.

Short-Term Rental Limitations

Some lenders restrict or discount short-term rental income.

If you are relying on Airbnb-style projections, you may need:

- Documented income history

- Or acceptance of conservative rent estimates

Balanced Perspective

DSCR loans trade flexibility for cost.

- You gain access without traditional income verification

- You pay through higher rates and stricter deal requirements

This is not inherently good or bad. It depends on how well the property performs.

Key Insight

DSCR loans reward disciplined investing.

Strong cash-flowing properties benefit from this structure. Weak or speculative deals are exposed quickly.

Common Misunderstandings About DSCR Loans

DSCR loans are often simplified in ways that lead to poor decisions. These misunderstandings can result in rejected applications, weak deals, or unexpected loan terms.

Clarifying them is essential.

“No Income Verification Means No Qualification”

This is the most common misconception.

DSCR loans do not require personal income verification, but that does not mean approval is automatic.

Lenders still evaluate:

- Property cash flow

- Credit profile

- Down payment

- Cash reserves

The qualification standard shifts from personal income to deal strength. It does not disappear.

“If the DSCR Is Above 1.0, You Are Approved”

A DSCR above 1.0 only means the property covers its debt.

Most lenders require 1.20 to 1.25 or higher to approve a loan under standard terms.

A DSCR near 1.0 may still be considered, but it often leads to:

- Higher interest rates

- Larger down payments

- Additional reserve requirements

The margin matters as much as the threshold.

“Any Rental Property Qualifies”

Not all income-producing properties meet DSCR standards.

Lenders prefer:

- Stable rental demand

- Predictable income

- Move-in-ready condition

Properties that often face challenges:

- Major renovation projects

- Unstable rental markets

- Unproven income models

The property must demonstrate reliability, not just potential.

“Short-Term Rental Income Is Always Accepted”

Short-term rental income is not treated consistently.

Some lenders:

- Ignore it entirely

- Discount it heavily

- Require documented history

Relying on projected Airbnb income without verification can weaken or invalidate a deal.

“DSCR Loans Are Always Easier to Get”

DSCR loans remove one barrier, but they introduce another.

They are easier for:

- Investors with strong cash-flowing properties

- Borrowers with non-traditional income

They are harder for:

- Low-margin deals

- Properties with uncertain income

- Investors relying on optimistic projections

The difficulty depends on the quality of the deal.

“Lenders Only Care About One Number”

The DSCR ratio is the primary metric, but it is not the only factor.

Lenders still assess:

- Credit history

- Liquidity

- Property quality

- Market conditions

A strong DSCR improves approval odds, but it does not override all other risks.

Key Insight

Most DSCR loan mistakes come from oversimplification.

The loan is not “easy.” It is precise. Strong deals pass. Weak deals fail.

When a DSCR Loan Makes Sense (And When It Doesn’t)

A DSCR loan is not universally better than a traditional mortgage. It is effective in specific situations and inefficient in others.

The key is knowing when the structure aligns with your goals.

When a DSCR Loan Makes Sense

You Are Buying or Scaling Rental Properties

DSCR loans are designed for income-producing real estate.

They work best when:

- The property generates stable rental income

- Each deal can stand on its own cash flow

This makes them well-suited for investors building or expanding a portfolio.

You Are Self-Employed or Have Irregular Income

If your income is inconsistent or heavily reduced by tax strategies, traditional loans may undervalue your financial position.

DSCR loans bypass that issue by focusing on the asset instead of your reported income.

You Want to Avoid Debt-to-Income Limitations

Traditional lenders cap how much you can borrow based on your personal debt ratios.

DSCR loans remove that constraint. As long as each property performs, additional acquisitions remain possible.

This is a key advantage for long-term investors.

Your Deal Has Strong Cash Flow

DSCR loans reward clean numbers.

If your property shows:

- Solid rental demand

- A DSCR above 1.25

- Predictable expenses

You are likely to receive better terms and smoother approval.

When a DSCR Loan Does Not Make Sense

You Are Buying a Primary Residence

DSCR loans are not designed for owner-occupied homes.

Traditional mortgages typically offer:

- Lower interest rates

- Better consumer protections

For personal residences, conventional financing is usually the better option.

The Property Has Weak or Unstable Income

If the deal barely covers the loan or relies on optimistic projections, it will struggle under DSCR evaluation.

Low-margin properties often lead to:

- Higher costs

- Stricter conditions

- Or denial

You Are Planning a Fix-and-Flip Strategy

DSCR loans are built for stabilized, income-producing assets.

Properties that require heavy renovation or repositioning typically do not qualify. Other financing types are more appropriate for these strategies.

You Qualify Easily for Conventional Financing

If you have:

- Strong, stable income

- Low debt

- High credit

A traditional loan may offer:

- Lower interest rates

- Lower upfront costs

In this case, a DSCR loan may not be the most efficient choice.

Decision Framework

The choice comes down to alignment:

- Use a DSCR loan when the property is the strength

- Use a traditional loan when your personal income is the strength

Key Insight

A DSCR loan is a tool, not a shortcut.

It works best when the deal is strong enough to stand on its own, without relying on your personal finances to justify it.

Real-World Example of a DSCR Loan

Understanding the structure is useful. Seeing how a deal is evaluated in practice makes it clear.

Scenario

An investor is purchasing a single-family rental property.

- Purchase price: $300,000

- Down payment: 25% ($75,000)

- Loan amount: $225,000

The property is expected to generate $2,400 per month in rent.

Step 1: Estimate Net Operating Income (NOI)

Monthly rental income: $2,400

Estimated expenses:

- Property management: $200

- Maintenance: $200

Remaining income before debt:

- NOI = $2,000 per month

Step 2: Calculate Monthly Debt Service

Loan payment (including taxes and insurance):

- $1,500 per month

Step 3: Calculate DSCR

- DSCR = 2,000 ÷ 1,500 = 1.33

Step 4: Interpret the Result

A DSCR of 1.33 means the property generates 33% more income than required to cover the loan.

From a lender’s perspective:

- The deal exceeds the typical 1.25 threshold

- There is a reasonable buffer for risk

- The property demonstrates stable cash flow

This would generally qualify for standard DSCR loan terms, assuming other factors are acceptable.

What If the Numbers Change?

Small changes can significantly impact the outcome.

Scenario A: Lower Rent

If rent drops to $2,100:

- NOI becomes approximately $1,700

- DSCR = 1,700 ÷ 1,500 = 1.13

This falls below most lender thresholds. The deal becomes weaker and may require adjustments.

Scenario B: Higher Down Payment

If the investor increases the down payment:

- Loan amount decreases

- Monthly payment drops

This improves the DSCR, even if rent stays the same.

Scenario C: Higher Expenses

If maintenance or management costs increase:

- NOI decreases

- DSCR drops

This reduces the margin of safety and can affect approval or loan terms.

What This Example Shows

A DSCR loan is highly sensitive to inputs.

- Rental income

- Expenses

- Loan structure

Each variable directly affects the outcome.

Key Insight

A DSCR loan is not just about qualifying.

It is about structuring a deal where the numbers remain strong under realistic conditions.

How to Find the Right DSCR Lender

Not all DSCR lenders operate the same way. Differences in underwriting, pricing, and flexibility can significantly impact your deal.

Choosing the right lender is part of the investment strategy, not just a final step.

1. Focus on Investor-Oriented Lenders

Start with lenders that specialize in investment properties.

These lenders are more likely to:

- Understand DSCR-based underwriting

- Work with rental-focused scenarios

- Offer flexible loan structures

General retail banks often follow stricter, conventional frameworks, even when offering DSCR products.

2. Compare Core Loan Criteria

Before committing, evaluate how each lender defines risk.

Key areas to compare:

- Minimum DSCR requirement

- Credit score thresholds

- Down payment expectations

- Reserve requirements

- Treatment of short-term rental income

Small differences in these criteria can determine whether a deal is approved or declined.

3. Evaluate Pricing and Terms

Interest rate is only one part of the equation.

You should also review:

- Origination fees

- Closing costs

- Prepayment penalties

- Loan structure (fixed, adjustable, interest-only)

A lower rate with restrictive terms may be less valuable than a slightly higher rate with better flexibility.

4. Assess Speed and Execution

In competitive markets, execution matters.

Consider:

- Average closing timeline

- Responsiveness during underwriting

- Clarity of communication

A lender who can close reliably and quickly can improve your ability to secure deals.

5. Ask Direct Questions

Clarity upfront prevents issues later.

Ask:

- What DSCR threshold do you require?

- How do you calculate rental income?

- Do you allow short-term rental projections or only historical income?

- What conditions could delay or deny approval?

Clear answers indicate a structured and experienced lender.

6. Watch for Warning Signs

Some issues indicate poor fit or elevated risk.

Be cautious if a lender:

- Provides vague or inconsistent answers

- Avoids clear pricing details

- Requires excessive documentation unrelated to DSCR lending

- Changes terms late in the process without explanation

These signals often lead to delays or unfavorable outcomes.

7. Compare Multiple Offers Before Deciding

Do not rely on a single option.

Review at least two to three lenders and compare:

- Total cost of the loan

- Approval conditions

- Flexibility for your specific deal

The goal is not just approval. It is alignment with your investment strategy.

Key Insight

The lender influences more than financing.

The right lender improves execution, flexibility, and long-term scalability. The wrong one can limit all three.

Tips to Qualify for Better DSCR Loan Terms

Getting approved is one outcome. Getting favorable terms is another.

Lenders adjust pricing and flexibility based on how strong your deal appears on paper. Small improvements can materially change your loan.

1. Increase the Property’s Cash Flow

The DSCR ratio drives the deal. Improving it improves everything else.

You can strengthen cash flow by:

- Setting rent at market rate

- Reducing operating expenses

- Selecting properties in high-demand rental areas

Even modest improvements in monthly income can increase your DSCR and shift your loan into a better tier.

2. Improve Your Credit Profile

Credit does not determine approval, but it directly impacts pricing.

Before applying:

- Pay down high credit balances

- Resolve errors on your credit report

- Avoid opening new credit lines

Moving from the mid-600s to 700+ can reduce your interest rate and fees.

3. Increase Your Down Payment

A larger down payment reduces lender risk.

This leads to:

- Lower loan-to-value ratio

- Improved DSCR (through smaller loan payments)

- Better loan terms

If your DSCR is borderline, increasing your equity can stabilize the deal.

4. Maintain Strong Cash Reserves

Reserves signal financial stability.

Lenders are more confident when you can cover several months of payments without relying on rental income.

Stronger reserves can:

- Improve approval odds

- Reduce required conditions

- Strengthen your negotiating position

5. Choose the Right Property

Not all deals are equal under DSCR evaluation.

Focus on properties that:

- Have stable, predictable rental demand

- Require minimal immediate repairs

- Are located in consistent rental markets

Avoid deals that depend on aggressive assumptions or future improvements to justify the numbers.

6. Present Clean, Organized Documentation

Even though DSCR loans require less personal documentation, clarity still matters.

Prepare:

- Lease agreements or rent estimates

- Expense breakdowns

- Asset statements for reserves

Well-organized information speeds up underwriting and reduces friction.

7. Negotiate Based on Strength

Once you receive loan offers, use your deal quality as leverage.

You may be able to negotiate:

- Lower origination fees

- Reduced prepayment penalties

- Slight rate improvements

Stronger deals create more room for negotiation.

Key Insight

Better DSCR loan terms are not random.

They are the result of stronger numbers, cleaner presentation, and lower perceived risk.

Conclusion

DSCR loans represent a shift in how real estate financing is evaluated. Instead of relying on personal income, they focus on whether the property itself can support the debt.

This structure creates a clear standard. If the numbers work, the deal works. If they do not, no amount of explanation will compensate.

For investors, this offers both opportunity and discipline. It removes barriers tied to income verification and debt ratios, but it also demands stronger deal selection and realistic assumptions.

Used correctly, DSCR loans can support portfolio growth and provide access to financing that traditional loans may restrict. Used carelessly, they can expose weak investments quickly.

The key is alignment.

When the property performs on its own, a DSCR loan becomes a powerful and efficient financing tool.

Frequently Asked Questions

What is a good DSCR ratio for approval?

Most lenders look for a DSCR between 1.20 and 1.25 or higher. Stronger ratios can improve loan terms and reduce perceived risk.

Can you get a DSCR loan with low credit?

Some lenders accept scores in the 600–620 range, but lower credit typically results in higher interest rates, larger down payments, and stricter conditions.

Do DSCR loans require any income verification?

They generally do not require personal income verification such as W-2s or tax returns. However, lenders still verify assets, credit, and property income.

Are DSCR loans only for rental properties?

Yes. These loans are designed for income-producing real estate, such as long-term rentals and, in some cases, short-term rentals.

Can DSCR loans be used for Airbnb properties?

Some lenders allow it, but many require:

- Documented income history, or

- Conservative market rent estimates

Policies vary, so this must be confirmed before applying.

What happens if the DSCR drops after closing?

Nothing changes as long as you continue making payments. DSCR is evaluated during underwriting, not monitored continuously after the loan is issued.

2 Comments

How to Calculate DSCR (Simple Formula + Real Examples) - Look Up Loans · April 15, 2025 at 11:38 am

[…] Learn more about DSCR loans in our complete approval guide. […]

Best DSCR Loan Lenders in 2025 (Reviewed + Compared) - Look Up Loans · April 17, 2025 at 1:41 pm

[…] a broader look at how DSCR loans work and what lenders actually look for, our complete DSCR loan guide is a useful companion to this […]