Introduction

Sick of banks grilling you about your job history, pay stubs, and tax returns only to slam the door in your face? You’re not alone. And honestly, you deserve better.

The traditional mortgage system was designed for 9-to-5 employees with perfect credit and boring lives. But real estate investors? Entrepreneurs? Self-employed hustlers? We play by different rules.

If you’ve ever dreamed about building wealth without begging a bank for approval, you’re about to discover a little-known strategy the pros use: DSCR loans.

In this brutally honest guide, you’ll learn exactly how to get approved without W-2s, without tax returns, and without explaining your life story to some banker behind a desk.

Ready to unlock the investor’s secret weapon? Let’s go.

Disclaimer: This site contains affiliate links. If you make a purchase, we may earn a commission at no extra cost to you.

Key Takeaways

- DSCR loans don’t care about your personal income only the property’s cash flow matters.

- You can get approved even if you’re self-employed, retired, or between jobs.

- Lenders only look at one simple number and you’ll learn exactly how to nail it.

- Most people get rejected because they don’t understand the hidden DSCR traps (you will).

- By the end of this guide, you’ll know how to find the right lender, qualify faster, and lock in better terms without jumping through endless hoops.

What Is a DSCR Loan?

A DSCR loan flips the traditional mortgage script on its head.

Instead of forcing you to prove how much money you personally make, a DSCR loan asks a far more important question: Can the property pay for itself?

DSCR stands for Debt Service Coverage Ratio, a fancy way of saying “Does the property’s income cover the loan payments?”

If the answer is yes, you’re in business.

Here’s the raw truth: Traditional banks don’t care about your dreams. They care about your job history, tax returns, and a thousand tiny documents. DSCR lenders? They care about the deal, the property’s cash flow. That’s it.

If the numbers make sense, you can get approved. Even if you’re self-employed. Even if your tax returns are messy. Even if you’re between jobs.

That’s why smart investors are quietly using DSCR loans to scoop up rental properties while everyone else is still fighting with bank underwriters.

How Does a DSCR Loan Work?

It all boils down to one simple number: your Debt Service Coverage Ratio (DSCR).

Here’s the formula lenders use:

DSCR = Net Operating Income (NOI) ÷ Debt Payments

Translation:

- Net Operating Income (NOI) = How much cash your rental property makes after expenses (but before paying the mortgage).

- Debt Payments = Your total loan payments principal + interest + taxes + insurance.

If your property’s income covers the loan payments (and then some), you’re golden.

Real-World Example: Imagine you own a rental house that pulls in $2,500/month in rent.

- After paying property management, taxes, and maintenance, your Net Operating Income is $2,000/month.

- Your monthly mortgage payment (loan + escrow) is $1,500/month.

Your DSCR would be:

20001500=1.33\frac{2000}{1500} = 1.3315002000=1.33

A DSCR of 1.33 means your property earns 33% more than needed to pay the loan. Lenders love that.

General Rule of Thumb:

- 1.0 = Property just covers the loan.

- 1.25+ = Property cash flows safely (most lenders want at least this).

- 1.5+ = You’re a rockstar in their eyes likely better rates.

The Bottom Line: If your property’s cash flow is strong enough, lenders don’t care about your day job, your side hustle, or even if you’re “technically unemployed.”

The deal funds itself and that’s all that matters.

Want to skip the math?

Use our free DSCR loan calculator to instantly see how your numbers stack up and whether your deal has a shot at approval.

DSCR Loan Requirements You Need to Know

DSCR loans are built for speed but if you think lenders hand out money without a checklist, think again.

They still want to know you and the property can play ball. Here’s exactly what you need to lock one down.

1. Credit Score (But Not Perfect)

Forget the old myth that you need a near-perfect credit score to get funded.

Most DSCR lenders want a minimum credit score of 620 to 680. The higher you are, the better the deal lower rates, smaller fees, fewer headaches.

If your credit is dragging near the bottom? Some investor-focused lenders will still work with you at 600–620 if your property’s cash flow is strong enough to make them look past it.

Smart move: If you’re flirting with a 700 score, spend a few weeks boosting it. Small tweaks can save you thousands over the life of the loan.

2. Down Payment (Bring Some Skin to the Game)

DSCR lenders want to see that you have real money on the line. The sweet spot is a 20%–25% down payment. Less skin = higher risk = higher rates.

Some lenders whisper about 15% down but trust this: it comes with painful pricing and tighter rules. Push for 25%, and doors open faster.

Pro tip: If your DSCR ratio is looking weak, throwing more cash down can save a deal that would otherwise crash.

3. Strong Property Income (Cash Is King)

At the end of the day, lenders care about one thing: can the property pay for itself?

They expect your property to hit at least a 1.00–1.25 DSCR. Anything less makes them nervous. They’ll run an appraisal based on market rents or actual leases. And if you’re banking on Airbnb or VRBO income? Brace yourself. Not all lenders recognize short-term rental numbers unless you can back them up with proof.

The safer your cash flow looks on paper, the better your deal gets.

4. Cash Reserves (Your Safety Net)

Some lenders want to see three to six months’ worth of mortgage payments sitting in reserve.

Think of it as a backup parachute. Even if rental income dries up for a few months, they want proof you can float without panicking.

Good news: You can often use retirement accounts or stock portfolios to meet this requirement. You don’t even need to move the money, just prove it exists.

5. Property Type (Choose Your Weapon Wisely)

Not every property qualifies for a DSCR loan.

Stick to cash-flowing assets like:

- Single-family homes

- Condos

- Townhomes

- 2–4 unit multifamily properties

Some lenders allow short-term rentals but luxury vacation homes, undeveloped land, and major fix-and-flips? Forget it. They want income machines, not risky projects.

Watch out for properties with ridiculous HOA fees or ones sitting in declining neighborhoods. Those can quietly kill your deal before you even make an offer.

Bottom line on Requirements

DSCR loans move fast, but only if you bring the right ammo. Good credit, solid cash flow, real skin in the game that’s how you get lenders chasing you instead of the other way around.

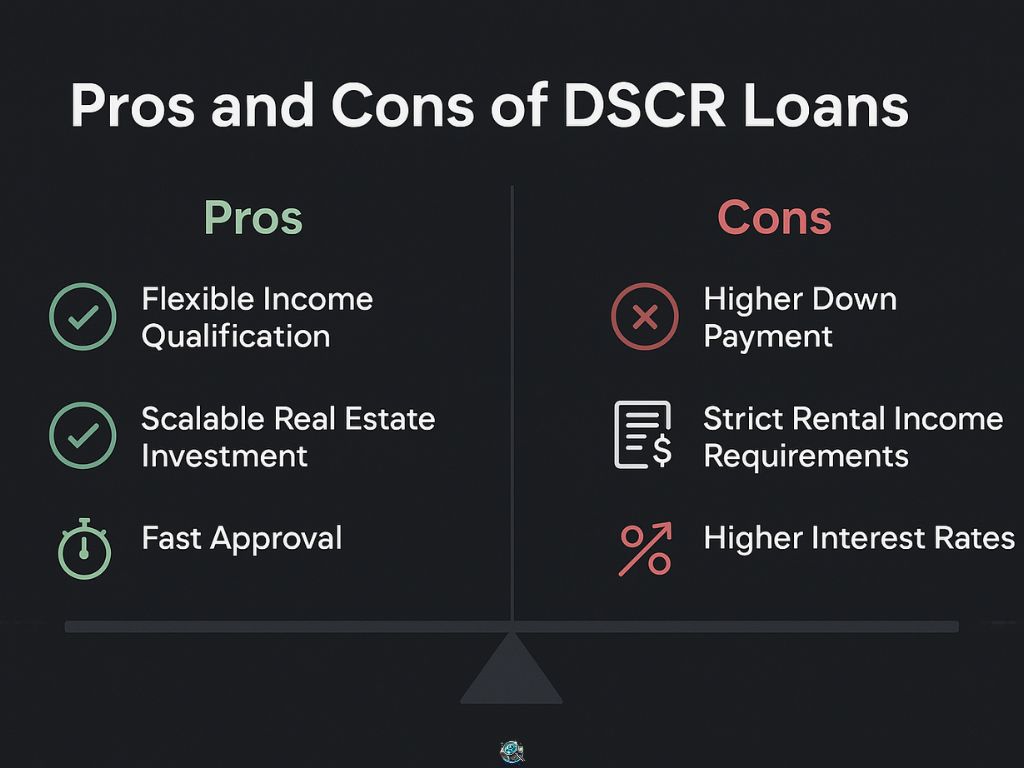

Pros and Cons of DSCR Loans

DSCR loans are powerful but like any tool, they can build an empire or wreck it if you are not careful.

Here’s what you need to know before you sign anything.

Major Advantages

1. No Personal Income Verification

Forget W-2s, tax returns, and endless explanations. If the property cash flows, you are in the game.

2. Fast Approvals and Closings

Less paperwork means faster decisions. Investors can close deals in weeks not months.

3. Scale Your Portfolio Quickly

No personal debt-to-income ratio holding you back. As long as each property cash flows, you can stack assets faster than with traditional loans.

4. Flexible Loan Structures

Many DSCR lenders offer interest-only options, 30-year fixed terms, and even no-prepayment-penalty setups if you negotiate right.

5. Perfect for Self-Employed Investors

If you run your own business, freelance, or earn “non-traditional” income, DSCR loans are your shortcut around the banks’ red tape.

Potential Drawbacks

1. Higher Interest Rates

You are paying for flexibility. DSCR loans often run 1–2% higher than conventional mortgage rates.

2. Larger Down Payments

Expect to bring 20%–25% cash to the table sometimes more if the lender feels nervous about the deal.

3. Strict Cash Flow Requirements

If your property barely covers the mortgage (DSCR around 1.0), expect tougher terms or higher reserves demanded.

4. Limited Property Types

No flips, no empty lots, no luxury dream homes. If it does not cash flow on day one, lenders will not touch it.

5. Short-Term Rental Scrutiny

If you are buying an Airbnb or VRBO property, know this: many lenders will only count long-term rental income unless you can show a proven track record.

Bottom Line on Pros and Cons

DSCR loans are not for everybody. They are for investors who understand one thing: money follows math, not emotions.

If you play the cash flow game right, DSCR loans can help you scale your portfolio faster, safer, and smarter than you ever could by begging a traditional bank for approval.

But if you ignore the numbers or overestimate your property’s income, you will pay literally.

Choose wisely.

How to Find a DSCR Loan Lender (Without Getting Ripped Off)

Finding a DSCR lender is easy. Finding a good DSCR lender who does not bleed you dry is another story.

Here’s how the smart investors do it.

1. Look for Investor-First Lenders

You want lenders who actually understand investors not retail banks that treat you like you are applying for your first car loan.

Good DSCR lenders:

- Focus on property cash flow, not personal income

- Know how to work with short-term rentals, multi-family, and unique properties

- Offer flexible structures like interest-only periods or ARM products

- Speak your language fast closings, investor-focused advice, real options

If they start asking you about your employer or annual salary, you are wasting your time.

2. Ask the Right Questions

Before you hand over any documents, grill the lender.

Questions to ask:

- What is your minimum DSCR requirement?

- Do you allow short-term rental income in underwriting?

- What credit score minimum do you work with?

- How fast can you close?

- What are your prepayment penalties, if any?

If they stumble or dodge clear answers, move on. There are too many good lenders out there to waste time.

3. Watch for Red Flags

Bad DSCR lenders are easy to spot if you know what to look for.

Warning signs:

- Ridiculously high fees hidden deep in the fine print

- Vague answers about rates or terms

- Excessive documentation demands (they should not need your full tax history)

- Loan officers who sound like they barely know what DSCR means

If they seem confused, lazy, or secretive, run.

4. Compare, Then Commit

Do not stop at the first “yes.” Talk to at least two or three lenders, compare their offers side by side, and see who treats you like a business partner not just a transaction.

A slightly higher interest rate might be worth it if it comes with better speed, flexibility, and support.

Pick the lender that helps you close deals, not just the one dangling the lowest rate.

Choosing the Right Lender

Smart investors know this truth: your lender can make or break your entire deal.

Choose fast, and you might regret it. Choose right, and you will wonder why you did not use DSCR loans sooner.

Tips to Qualify for the Best DSCR Loan

Getting a DSCR loan is one thing. Getting a great DSCR loan fast, clean, and on your terms is another.

Here’s how the smart money gets it done.

1. Boost Your Property’s Cash Flow

Your property’s numbers are your credit report in a DSCR loan.

A higher DSCR score (think 1.25 or above) gets you better rates and lower fees.

Simple ways to boost cash flow before applying:

- Raise rent if the property is underpriced.

- Reduce expenses (negotiate lower management or maintenance costs).

- If buying, target properties with strong rental demand, not emotional appeal.

A $100 increase in monthly cash flow can be the difference between approval and rejection.

2. Polish Your Credit Score

Even though DSCR loans focus on the property, your credit still matters.

Before applying:

- Pay down high credit card balances.

- Fix any errors on your credit report.

- Avoid opening new credit accounts.

A small bump from a 660 to a 700 could slash your interest rate by half a point or more. That is real money staying in your pocket.

3. Prepare Proof of Rental Income

If the property is already rented, gather the leases, rental history, and payment records early.

If it is a short-term rental, be ready to show income statements or 12 months of booking data.

Do not assume the lender will chase this down for you bring it to the table upfront and make their job easier.

The smoother your documentation, the faster your approval.

4. Choose the Right Property

Not every deal is a DSCR winner.

Stick to properties that:

- Are move-in ready, not fixer-uppers.

- Have strong local rental demand.

- Are in areas with stable or rising property values.

If you chase flashy vacation homes or fixer-uppers in weak markets, expect headaches or outright denials.

Pick properties that make lenders nod, not scratch their heads.

5. Negotiate Smartly

Once you have a few loan offers in hand, do not just accept the first terms thrown at you.

Push for:

- Lower origination fees

- Waived prepayment penalties

- Better interest rates in exchange for a higher down payment

Lenders expect you to negotiate. If you come in prepared, you will often walk away with better terms and a stronger position for future deals.

Qualifying

DSCR loans reward prepared investors.

If you show up with clean numbers, strong properties, and a smart plan, you will not just get approved, you will get the kind of deal other investors wish they knew how to pull off.

Preparation wins every time.

Frequently Asked Questions About DSCR Loans

What is a good DSCR ratio for a loan?

Most lenders want to see a DSCR of at least 1.20. The higher, the better. A DSCR of 1.25 or above puts you in a strong position for better rates and faster approvals. If your DSCR is under 1.0, meaning your property does not fully cover the loan payments, expect higher scrutiny or outright rejection.

Can I get a DSCR loan with bad credit?

Yes, but it will cost you. Some lenders will work with credit scores as low as 600–620, especially if the property cash flows strongly. However, expect higher interest rates, bigger down payments, and more reserve requirements if your credit score is on the low side.

Do I need to show personal income for a DSCR loan?

No. That is the point of a DSCR loan. Lenders approve you based on the property’s income, not your W-2s, tax returns, or personal bank statements.

If the property covers the debt, you are in the game.

How much do I need for a DSCR loan down payment?

Plan for at least 20%–25% down.

Some lenders allow less, but you will pay for it through higher rates and tougher loan terms. A bigger down payment can also help offset a weaker DSCR or lower credit score.

Are DSCR loans only for rental properties?

Mostly, yes.

DSCR loans are designed for income-producing properties like:

- Single-family rentals

- Duplexes, triplexes, fourplexes

- Condos and townhomes

They are not made for flips, raw land, personal residences, or heavy rehab projects.

Can I use a DSCR loan for a vacation rental or Airbnb?

Sometimes. Some lenders allow short-term rental properties under DSCR loans but many will only count long-term market rent in their income calculations unless you can prove consistent short-term rental earnings with documentation. If you are buying an Airbnb, check the lender’s policy carefully before you apply.

What happens if my property’s DSCR drops after I get the loan?

If you make your payments, nothing happens. Lenders care about your DSCR at the time of underwriting and approval. Once the loan closes, they are not checking your property’s income every month. Stay current on your payments, and you stay in control.

Final Thoughts: Why DSCR Loans Are Reshaping Real Estate Investing

The old way of building wealth begging a bank to approve your dreams is broken. DSCR loans are the blueprint for a new era.

When you control cash flow, you control the deal. You are no longer judged by your job title, your W-2, or how neat your tax returns look. You are judged by the numbers that matter the numbers you can build, shape, and scale.

That is why smart investors are using DSCR loans to stack rental properties faster, safer, and with fewer limits than ever before.

It is not about asking for permission anymore. It is about showing up with strong deals, confident numbers, and the right lenders by your side.

If you understand the rules, you can write your own future. And DSCR loans? They are one of the sharpest tools you will ever carry into the fight.

2 Comments

How to Calculate DSCR (Simple Formula + Real Examples) - Look Up Loans · April 15, 2025 at 11:38 am

[…] Learn more about DSCR loans in our complete approval guide. […]

Best DSCR Loan Lenders in 2025 (Reviewed + Compared) - Look Up Loans · April 17, 2025 at 1:41 pm

[…] a broader look at how DSCR loans work and what lenders actually look for, our complete DSCR loan guide is a useful companion to this […]