Introduction

Two people can apply for the same personal loan and receive very different offers. One may qualify for a lower APR, fewer fees, and flexible terms. Another may face a higher rate, a smaller loan amount, or a repayment plan that costs more over time.

Your credit score is one reason. Lenders use your credit history to help estimate repayment risk. A stronger credit profile can open the door to better rates and more lender options, while a weaker one can make borrowing more expensive.

That means your credit score can affect more than approval. It can shape your APR, fees, repayment term, monthly payment, and total repayment cost. Understanding that connection before you apply can help you compare offers more clearly and avoid choosing a loan that costs more than it seems.

Key Takeaways

- Your credit score can affect whether you qualify for a personal loan and what terms you receive.

- A higher credit score may help you qualify for a lower APR, better terms, and more lender options.

- A lower credit score may lead to higher borrowing costs because lenders may see more repayment risk.

- APR is one of the best numbers to compare because it includes the interest rate plus certain loan fees.

- Fees, repayment term, and monthly payment all affect the true cost of a personal loan.

- Prequalification can help you compare estimated rates and terms before submitting a full application.

- A lower credit score does not automatically make a personal loan a bad choice, but it makes careful comparison more important.

Disclaimer: This site contains affiliate links. If you make a purchase, we may earn a commission at no extra cost to you.

Standard Credit Score Ranges

A credit score tells lenders how you handle money.

Different numbers mean different things.

Here is a basic guide to credit scores.

| Score Range | Category |

|---|---|

| 300 to 579 | Poor |

| 580 to 669 | Fair |

| 670 to 739 | Good |

| 740 to 799 | Very Good |

| 800 to 850 | Excellent |

Why your credit score can change more than your approval odds

When people think about credit scores and personal loans, they often focus on one question: “Will I get approved?” That matters, but it is only part of the picture. Your credit score can also influence what the loan looks like after approval.

Lenders may use your credit score, credit report, income, debts, employment status, and other application details when deciding what interest rate and terms to offer. A stronger credit profile may help you qualify for more favorable loan options, while a weaker one may lead to a higher borrowing cost or fewer choices.

Your credit score may affect:

- APR: A lower score may lead to a higher rate, which can increase the total cost of the loan.

- Loan amount: Some lenders may approve you for less than you requested if they see more repayment risk.

- Repayment term: Your available term options may vary based on the lender’s requirements and your overall borrower profile.

- Lender options: A higher credit score can make it easier to qualify and may give you more lenders to compare.

- Fees and total cost: Some personal loans include fees, so it is important to review the full loan disclosure before accepting an offer.

This is why approval should not be the only goal. A loan can be approved and still be expensive. Before accepting an offer, compare the full cost of borrowing, not just whether the lender says yes.

How credit score affects your personal loan APR

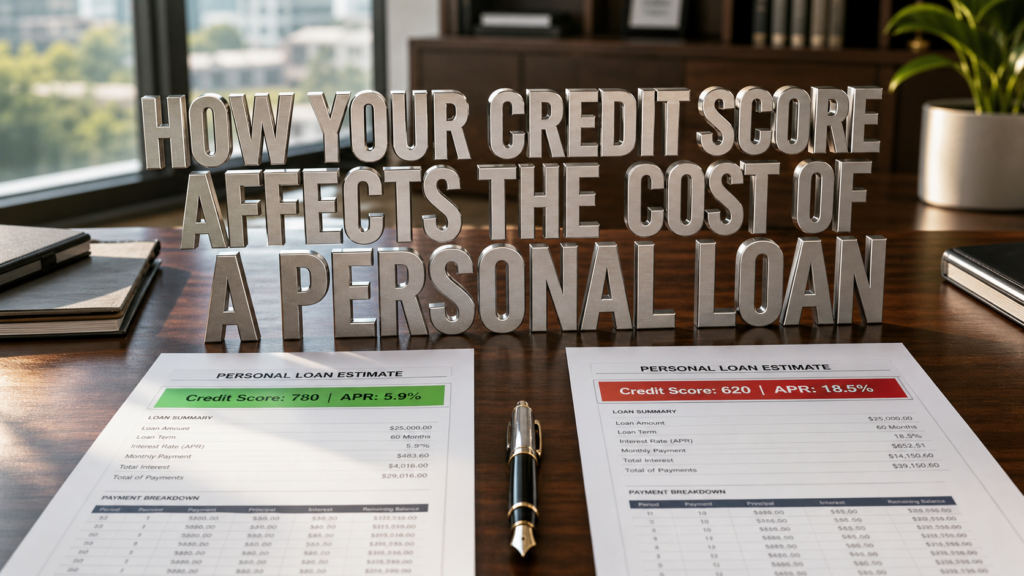

Your credit score can play a major role in the APR a lender offers. APR is especially important because it reflects the interest rate plus certain loan fees, which makes it a broader measure of borrowing cost than the interest rate alone.

In general, lenders charge more when they believe a borrower has a higher chance of missing payments or defaulting. This is often called risk-based pricing. A lender may offer less favorable terms, such as a higher interest rate, based on information in your credit report or application.

Here is a simple example. This assumes a $10,000 personal loan, a 36-month repayment term, fixed payments, and no added fees.

| Loan amount | APR | Repayment term | Estimated monthly payment | Estimated total interest |

| $10,000 | 8% | 36 months | $313 | $1,281 |

| $10,000 | 18% | 36 months | $362 | $3,015 |

| $10,000 | 30% | 36 months | $425 | $5,283 |

The loan amount and repayment term are the same in each example. The difference is the APR. At 8%, the estimated total interest is about $1,281. At 30%, the estimated total interest rises to about $5,283.

That is why even a loan with a manageable monthly payment can still be expensive. A higher APR does not only increase what you pay each month. It can also increase the total amount you repay over the full life of the loan.

Why lenders use credit scores to price personal loans

Lenders use credit scores because they need a way to estimate repayment risk before offering money. A credit score is not a complete picture of a borrower, but it can help lenders predict how likely someone is to repay a loan on time based on information in their credit reports.

That risk estimate can affect the price of the loan. When a lender sees a borrower as lower risk, it may be more comfortable offering a lower APR or more favorable terms. When a lender sees more risk, it may charge a higher rate to account for the greater chance that the loan may not be repaid as agreed. This type of pricing is commonly known as risk-based pricing.

This does not mean your credit score is the only thing that matters. Lenders may also review your income, existing debts, employment details, loan amount, and overall application. But your credit score often carries weight because it gives the lender a quick way to evaluate your past borrowing behavior.

It is also important to know that you do not have just one credit score. Different scoring models and credit reporting data can produce different scores, so the number you see through one app or service may not be exactly the same number a lender uses.

The practical takeaway is simple: lenders use credit scores to help decide how much risk they are taking. For borrowers, that means a stronger credit profile may lead to better loan options, while a weaker one may make it even more important to compare offers carefully before accepting.

The monthly payment is not the only number that matters

A lower monthly payment can make a personal loan look more affordable, but it does not always mean the loan is cheaper. A longer repayment term can reduce the monthly payment while increasing the total interest paid over time.

That is why borrowers should compare the full cost of the loan, not just the payment amount. APR is useful because it reflects the interest rate plus certain loan fees, giving borrowers a broader view of borrowing cost than the interest rate alone.

Here is a simple example comparing two $10,000 personal loan offers.

| Loan offer | Loan amount | APR | Repayment term | Estimated monthly payment | Estimated total interest | Origination fee |

| Offer A | $10,000 | 14% | 36 months | $342 | $2,304 | $0 |

| Offer B | $10,000 | 18% | 60 months | $254 | $5,236 | $500 |

Offer B has the lower monthly payment, which may seem better at first. But it also has a higher APR, a longer repayment term, more estimated interest, and an added fee. Personal installment loans may include fees, so borrowers should review the lender’s loan disclosure before accepting an offer.

The better loan is not always the one with the smallest monthly payment. It is the one that fits your budget while keeping the total cost reasonable. Before choosing a personal loan, compare the APR, repayment term, fees, monthly payment, and total repayment amount together.

What borrowers with fair or bad credit should watch closely

Having fair or bad credit does not automatically mean you should avoid a personal loan. It does mean you may need to review each offer more carefully. Lenders may offer less favorable terms, such as a higher interest rate, when they see more risk based on information in your credit report or application.

The goal is not just to find a lender that will approve you. The goal is to find a loan you can repay without creating a bigger financial problem.

Watch closely for:

- High APRs: A higher APR can make the loan much more expensive, even if the monthly payment looks manageable.

- Origination fees: Some lenders subtract this fee from the loan amount or add it to the cost of borrowing. That means you may receive less money than expected or pay more overall.

- Short repayment options: A shorter term can raise the monthly payment, which may make the loan harder to manage.

- Long repayment options with high rates: A longer term may lower the monthly payment, but it can also increase the total interest paid over time.

- Guaranteed approval claims: Be careful with lenders or ads that promise credit no matter your history. The FTC warns that “bad credit” or “guaranteed” loan language can be a sign of an advance-fee loan scam.

- Upfront payment requests: A lender that asks you to pay money before receiving the loan should raise concern, especially if the offer sounds unusually easy or pressure-filled.

- Unclear loan terms: If you cannot easily understand the APR, fees, repayment schedule, and total cost, pause before accepting.

Borrowers with lower credit scores are often looking for relief, and that can make fast approval offers feel tempting. But a personal loan should make your situation more manageable, not harder. Before signing, compare the APR, fees, monthly payment, repayment term, and total repayment amount so you know what the loan will actually cost.

How to improve your loan offer before applying

You may not be able to change your credit score overnight, but you can take steps that may help you apply from a stronger position. The goal is to reduce avoidable risk signals, understand what lenders may see, and compare offers before committing to a full application.

- Check your credit reports for errors.

Review your credit reports before applying so you can look for inaccurate or outdated information. The CFPB recommends checking your credit reports at least once a year to make sure errors do not keep you from getting credit or better loan terms. - Dispute inaccurate information.

If you find information you believe is wrong, you can dispute it with the credit reporting company and the company that provided the information. Credit reporting companies are required to investigate disputes and correct errors they find. - Lower credit card balances when possible.

Paying down credit card balances may help because credit scoring models often consider how much credit you are using compared with how much credit is available to you. The CFPB explains that paying off your credit card balance every month is one factor that can help improve your scores. - Use prequalification before submitting a full application.

Prequalification can help you estimate potential loan amounts, rates, and terms before you formally apply. It often uses a soft credit inquiry, which typically does not affect your credit score. - Compare more than one lender.

Different lenders may evaluate the same borrower differently, so one offer is not enough to know whether you are getting a fair deal. Compare APR, fees, repayment term, monthly payment, and total repayment cost before choosing. - Consider a co-borrower only when it makes sense.

A co-borrower or co-signer may strengthen an application in some cases, but that person also takes on repayment responsibility. The CFPB notes that a co-signer agrees to repay a loan and that co-signing carries obligations and risks. - Borrow only what you need.

A larger loan may feel helpful upfront, but it can also increase the amount of interest you pay. Before applying, decide how much you actually need and whether the monthly payment fits your budget.

Improving your loan offer is not just about raising your score. It is also about applying with cleaner information, lower balances where possible, and a clear comparison of what each lender is offering.

When a personal loan may still make sense with a lower credit score

A lower credit score does not automatically make a personal loan a bad choice. What matters most is whether the loan improves your situation after you account for the APR, fees, repayment term, monthly payment, and total cost.

A personal loan may make sense if it helps you replace more expensive debt with a more structured repayment plan. For example, a debt consolidation loan lets you borrow money to pay off separate debts and repay one loan over time. This can simplify the number of payments you manage, and in some cases, the new loan may have a lower interest rate than your existing debts.

A personal loan may be worth considering when it helps you:

- Consolidate higher-interest debt into one fixed monthly payment.

- Create a clear payoff timeline instead of carrying revolving debt with no set end date.

- Cover a necessary expense when the loan is more affordable than other borrowing options.

- Avoid higher-cost products that could create faster or more severe financial pressure.

Still, the loan should work on paper before it works in real life. APR includes the interest rate plus certain fees, so it gives a broader view of borrowing cost than the interest rate alone.

Before accepting a loan with a lower credit score, ask one simple question: does this loan make the debt easier and less expensive to manage, or does it only move the problem into a new payment? If the payment strains your budget or the total repayment cost is too high, it may be better to wait, improve your credit profile, or explore another option.

Common mistakes that make personal loans more expensive

A personal loan can look simple on the surface: borrow a set amount, make fixed payments, and pay it off over time. But small choices can change how much the loan actually costs. The mistake many borrowers make is focusing on approval first and cost second.

Before accepting an offer, watch for these common mistakes:

- Looking only at the monthly payment:

A lower monthly payment may feel easier to manage, but it can come with a longer repayment term. That may increase the total amount of interest you pay over the life of the loan. - Ignoring the APR:

The interest rate tells you part of the cost, but APR gives a broader view because it includes the interest rate plus certain loan fees. Comparing APR can help you understand which offer is actually more expensive. - Overlooking origination fees:

Some personal installment loans include fees that add to the total cost of borrowing. Review the lender’s disclosure carefully so you understand what fees apply and whether they reduce the amount of money you receive. - Skipping prequalification:

Prequalification can help you compare estimated loan amounts, rates, and terms before submitting a full application. Lenders often use a soft credit inquiry for prequalification, which typically does not affect your credit scores. - Submitting too many full applications without comparing first:

A full loan application may involve a hard credit inquiry, and hard inquiries can affect your credit score. That is why it helps to compare prequalified offers first, then apply when you have narrowed down your options. - Borrowing more than you need:

A larger loan can give you more cash upfront, but it also increases the amount you have to repay. If the extra money is not necessary, it may only add more interest and a larger payment obligation. - Choosing speed over clarity:

Fast funding can be helpful, especially for urgent expenses. But speed should not replace careful review. If the APR, fees, repayment term, or total cost are unclear, slow down before signing.

The best personal loan is not just the one that gets approved. It is the one with terms you understand, payments you can afford, and a total cost that makes sense for your situation.

Conclusion

Your credit score can affect far more than whether a lender approves your personal loan application. It can influence your APR, fees, repayment term, lender options, monthly payment, and total repayment cost.

That makes it important to look beyond the first offer you receive. A loan with a lower monthly payment may not always be cheaper, and a loan that gets approved quickly may not always be the best fit. The real question is whether the full cost makes sense for your budget and your reason for borrowing.

Before accepting a personal loan, compare APR, fees, repayment terms, monthly payments, and total repayment amounts across lenders. Your credit score may shape the offers available to you, but careful comparison can help you make a more informed decision and avoid paying more than necessary.

Frequently Asked Questions

What credit score do you need for a personal loan?

There is no single credit score required for every personal loan. Each lender sets its own approval standards, and lenders may also consider your income, debt, loan amount, and overall application. In general, a higher credit score can make it easier to qualify and may help you get a lower interest rate.

Does checking personal loan rates hurt your credit?

Checking rates through prequalification usually does not hurt your credit if the lender uses a soft credit inquiry. A soft inquiry does not affect your credit scores. However, submitting a full loan application may lead to a hard credit inquiry, which can have an impact.

Can you get a personal loan with bad credit?

It may be possible to get a personal loan with bad credit, but the offer may be more expensive. Lenders often use risk-based pricing, which means they may offer less favorable terms, such as a higher interest rate, based on information in your credit report or application.

How much does credit score affect personal loan interest rates?

The exact impact depends on the lender, loan amount, repayment term, and your full borrower profile. But credit score can matter because lenders use it to help estimate how likely you are to repay borrowed money. A higher score can make it easier to qualify for lower interest rates, while a lower score may lead to higher borrowing costs.

Is it better to improve your credit before applying?

It can be, especially if you are not in a rush to borrow. Improving your credit profile may help you qualify for better loan options, and checking your credit reports before applying can help you find errors that may affect your ability to get credit or better terms.

0 Comments