Introduction

Most big banks will reject you if you do not have a Social Security Number. This makes many people feel stuck, but the money is available if you know where to look.

You can legally buy a home, finance a car, or get a personal loan using only your ITIN. Approval depends on your income and history, not just a standard credit score.

This guide explains exactly how to find the right lenders and what documents you need to get funded.

Key Takeaways

- You have options: ITIN holders can legally get mortgages, car loans, and business funding.

- Look locally: Big national banks often say no. Credit unions and community lenders often say yes.

- Your history counts: Lenders may check your rent and electric bills instead of a credit score.

- Paperwork is king: Approval depends on your tax returns and proof of steady income.

- The trade-off: Expect slightly higher interest rates or down payments in exchange for access without an SSN.

Disclaimer: This site contains affiliate links. If you make a purchase, we may earn a commission at no extra cost to you.

Types of Loans You Can Get With an ITIN

You have four main options. Each has different rules because the lender takes a different level of risk.

1. Home Loans (Mortgages)

You can buy a house, but the rules are stricter. Most big banks cannot sell ITIN loans to the government (Fannie Mae), so they keep the loan themselves. Because of this risk, they usually require:

- Higher Down Payment: Expect to pay 15% to 20% upfront.

- Two Years of Taxes: You must show steady income filed with your ITIN.

- Manual Underwriting: A human will review your bank statements to see how you spend money.

2. Auto Loans

Car loans are easier to get because the car acts as security. If you stop paying, they take the car.

- The Trap: Avoid “Buy Here, Pay Here” lots. They often charge 20%+ interest.

- The Strategy: Go to a credit union first. They often offer fair rates if you have a job and a local address.

- Down Payment: A larger down payment often lowers your interest rate.

3. Personal Loans

These are “unsecured” loans. This means you do not put up a house or car as collateral. Because the lender has no security, these are harder to get and cost more.

- Use For: Emergencies or consolidating high-interest debt.

- Do Not Use For: Luxury purchases or vacations. The interest rates are too high.

4. Business Loans

If you run a business, your revenue matters more than your credit score. Lenders want to see cash flow.

Micro-Loans: These are smaller loans ($500 to $50,000) meant to buy equipment or inventory.

Community Lenders: Look for CDFIs (Community Development Financial Institutions). These are non-profit banks designed to help local businesses grow.

Quick Comparison: Which Loan Fits Your Needs?

| Loan Type | Key Requirements | Best Place to Apply | Good For |

|---|---|---|---|

| Home Loan | 15–20% down payment + 2 years of tax returns. | Credit Unions & Community Banks | Buying a home for the long term. |

| Auto Loan | Proof of income + valid ID. (Down payment lowers rate). | Local Credit Unions (Avoid Dealers if possible) | Getting to work or family transport. |

| Personal Loan | Steady income + bank statements. | Online Lenders & Nonprofits | Emergencies or paying off credit card debt. |

| Business Loan | Business plan + 12 months of revenue. | CDFIs & Micro-loan programs | Buying equipment or inventory. |

How to Apply for a Loan with an ITIN

The application process is standard, but the verification rules are stricter. You must prove your identity and stability differently than someone with a Social Security Number. Follow these five steps to prepare your file and get approved.

1. Gather Your Documents First

Lenders will not wait for you to find missing papers. Have these items ready physically and digitally to speed up the process:

- ITIN Number: Your official IRS letter (CP565) or tax return.

- Government ID: A valid passport, consular ID, or national ID.

- Proof of Income: Recent pay stubs, bank statements, or tax returns.

- Proof of Address: A utility bill or lease agreement in your name.

- Down Payment: Often required for mortgage or auto loans.

2. Check Your “Alternative” Credit

If you do not have a FICO score, you must show you pay bills on time. Collect the last 12 months of payment history for:

- Rent.

- Utilities (water, electric, internet).

- Phone bills.

- Note: Some lenders will also accept international credit reports to verify your history.

3. Find ITIN-Friendly Lenders

Not every bank works with ITIN borrowers. Focus your search on institutions known for flexibility:

- Credit Unions: Specifically those in your local community.

- Community Banks: Smaller banks often have manual underwriting.

- Online Lenders: Look for platforms that advertise “No SSN” options.

- Nonprofits & CDFIs: These organizations exist to help underserved borrowers.

- The Rule: Always check the FAQ or call to confirm they accept ITINs before you apply.

4. Compare Offers Before You Commit

Do not accept the first loan you find. Predatory lenders target people who feel desperate. Compare these factors:

- Interest Rates: A lower rate saves you money over time.

- Loan Terms: Check the monthly payment and total payback amount.

- Fees: Watch for hidden costs or penalties.

- Strategy: Ask to pre-qualify. This allows you to see your potential rate without a hard credit check that lowers your score.

5. Submit Your Application

Once you select the best offer, fill out the application online or in person. Hand over your document package immediately. Approval times vary, but funding often happens within 1 to 5 business days.Recommendation: If possible, speak to a loan officer directly. Tell your story. Explain that you have a stable job and payment history, just no SSN. A human underwriter can often make exceptions that a computer cannot.

Document Checklist for ITIN Loan Applications

Approval often depends on the quality of your paperwork. Lenders appreciate borrowers who are organized. Use this checklist to ensure you have everything before you apply.

| Document | Why It Is Needed | Accepted Examples |

|---|---|---|

| ITIN Number | Replaces the Social Security Number for the application. | IRS Letter (CP565) or a tax return with your number. |

| Government ID | Verifies your identity. Required by law. | Passport, Consular ID card, Driver’s License, or state ID. |

| Proof of Income | Shows you can afford the monthly payments. | Pay stubs, employer letters, bank statements, or invoices. |

| Proof of Address | Confirms your current U.S. residence. | Utility bill, lease agreement, mortgage statement, or official mail. |

| Tax Returns | Shows income consistency (Required for mortgages). | Last 2 years of Federal tax returns (Form 1040). |

| Rent/Utility History | Builds “Alternative Credit” if you lack a score. | Receipts for rent, water, electric, or phone bills. |

| Business Plan | For business loans only. Outlines how you make money. | Written business plan and financial projections. |

Quick Tip: Organize these documents before you apply. Inconsistent paperwork or missing proof is the main reason ITIN loan applications get delayed or denied.

Common ITIN Loan Mistakes to Avoid

Most rejections happen because of simple errors, not because of your ITIN. Avoid these five common traps to improve your chances of approval.

| The Mistake | Why It Hurts You | The Smart Fix |

|---|---|---|

| Applying blindly | If the lender does not accept ITINs, you get a “hard inquiry” on your report for nothing. | Check first. Call the bank or check their website for “ITIN accepted” before you apply. |

| Taking the first offer | You might pay higher interest rates or hidden fees than necessary. | Shop around. Pre-qualify with 3 different lenders to compare the total cost. |

| Ignoring local banks | Online lenders are convenient but often more expensive or risky. | Look local. Credit unions and Community Banks often offer safer terms and lower rates. |

| Forgetting “Alternative” Credit | Without a credit score, you look like a risk to the bank. | Show proof. Submit your rent, phone, and utility receipts to prove you are reliable. |

| Missing paperwork | Incomplete applications are the #1 reason for delays. | Be ready. Upload all your documents (ID, ITIN, Income) at the same time you apply. |

Quick Insight: Most rejections aren’t due to bad credit. They stem from unprepared applications or choosing the wrong lender. Verify the requirements first, and you will save time and money.

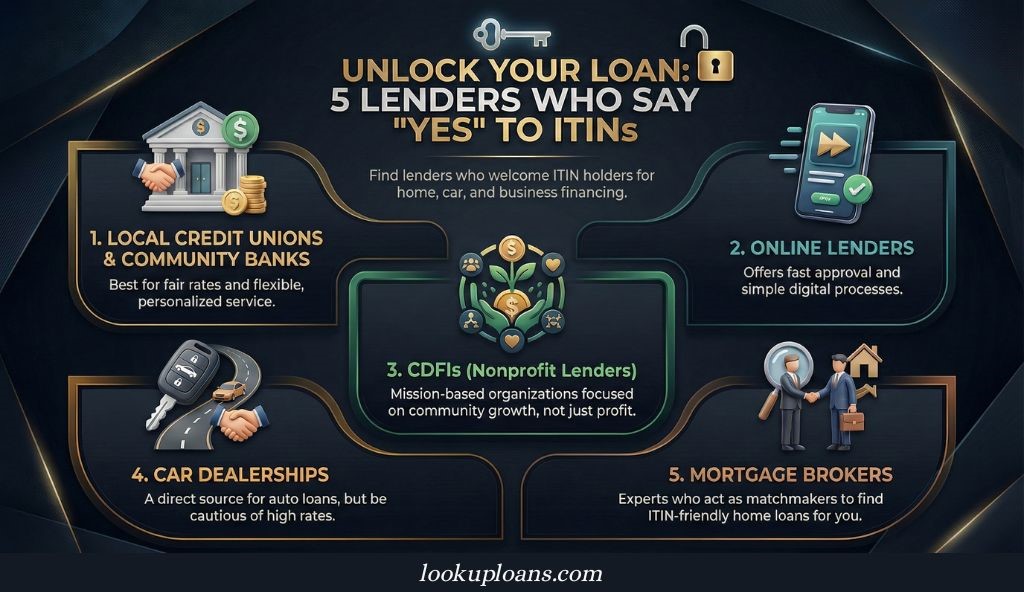

Where to Find Lenders That Accept ITINs

Finding the right lender is the hardest part. Most big national banks will reject you. You must look for institutions that understand your financial situation. Focus your search on these five specific categories.

1. Local Credit Unions & Community Banks (Your Best Option)

These are often the most friendly institutions for ITIN holders. Unlike big banks, they serve their local community and can be flexible with documentation.

- Why choose them: They often have bilingual staff and fair interest rates.

- Examples to check:

- Self-Help Federal Credit Union (CA, IL, WI).

- Latino Community Credit Union (NC).

- Guadalupe Credit Union (NM).

- Notre Dame Federal Credit Union (National reach).

- Pro Tip: Even if they do not advertise it online, walk into a branch or call them. Many offer ITIN loans in person only.

2. Online Lenders

Technology companies are making it easier to apply without visiting a bank. They are fast and often have mobile apps.

- Why choose them: Fast approval and simple processes.

- Examples to check:

- Oportun: Offers personal loans and bilingual service.

- Stilt: Great for immigrants with no U.S. credit history.

- Camino Financial: Focuses on business and personal loans for Latinos.

- Lendistry: Strong support for business loans.

- DreamSpring: Mission-based lending with flexible rules.

- Warning: Watch the interest rates. Online loans can be more expensive than credit unions. Always check for fixed rates and no hidden fees.

3. CDFIs (Community Development Financial Institutions)

These are nonprofit organizations designed to help people who are overlooked by traditional banks.

- Why choose them: They focus on helping you grow, not just making a profit. They often offer financial coaching.

- Examples to check:

- Accion Opportunity Fund: Supports immigrant entrepreneurs.

- Mission Asset Fund: Offers zero-interest loans and credit-building tools.

- Justine PETERSEN: Focuses on business owners with credit challenges.

- LiftFund: Operates in 14+ states (including TX and FL).

- Venturize.org: Use this directory to find a CDFI near you.

4. Car Dealerships

If you need a vehicle, many dealerships work with financing companies that accept ITINs.

- The Strategy: Ask upfront, “Do you work with lenders that accept ITINs?”

- The Trap: Avoid “Buy Here, Pay Here” lots unless you have no other choice. Their interest rates are often predatory.

- Requirement: You usually need proof of steady income and a down payment.

5. Mortgage Brokers

If you want to buy a home, do not go it alone. A mortgage broker acts as a matchmaker.

The Benefit: They help you prepare your document package so you get approved the first time. They can explain the closing costs and down payment rules in your language.

Why choose them: They know exactly which banks offer ITIN mortgage programs and which ones do not.

Pros and Cons of ITIN Loans

ITIN loans open doors, but they come with a cost. Understanding the trade-offs helps you avoid surprises.

| The Good News (Pro) | The Bad News (Con) | The Smart Move |

|---|---|---|

|

No SSN Required You can access legal funding using just your Tax ID number. |

Higher Rates Interest rates are often higher than standard loans. |

Refinance later. Use the loan to build credit, then refinance for a cheaper rate once your score improves. |

|

Open to Everyone Accessible to immigrants, non-citizens, and new residents. |

Harder to Find Most big banks do not offer these loans. |

Go Local. Start your search with Credit Unions and CDFIs. They are more likely to say yes. |

|

Flexible Rules Many lenders accept “Alternative Credit” (rent/bills) instead of a FICO score. |

Larger Down Payments Mortgage lenders often require 15%–20% cash upfront. |

Prepare early. Start saving for the down payment before you apply to show financial strength. |

|

Wide Availability Available for homes, cars, business, and personal needs. |

Predatory Lenders Scammers target ITIN holders with hidden fees. |

Compare offers. Never sign the first paper. Get 3 quotes and check for “Origination Fees.” |

Quick Insight: The goal is not just to get the loan, but to use it as a stepping stone. A slightly higher rate today is the price of admission to build a credit history for tomorrow.

Final Thoughts: Getting Approved Is a Strategy, Not Luck

Getting a loan without a Social Security Number is not impossible. It is simply a stricter process. If you have steady income and organized paperwork, you can access the same capital as anyone else.

The banks want to lend money; they just need proof that you are safe. Your job is to give them that proof. Do not settle for predatory loans out of fear. You have the right to shop around, ask questions, and demand a fair rate.

Your Next Moves:

- Gather your files: Find your ITIN letter, tax returns, and ID today.

- Start local: Call three credit unions and ask about their ITIN programs.

- Compare costs: Look at the APR and total fees before you sign anything.

Financial growth is available to you. Your ITIN is a valid tool, use it to build the asset you deserve.

Frequently Asked Questions About ITIN Loans

Is it legal to get a loan with just an ITIN?

Yes. Major banks and federal laws allow lending to ITIN holders. It is not a loophole; it is a standard banking product. Your approval depends on your ability to repay, not your citizenship status.

Do I need a credit score to apply?

Not always. While a credit score helps, many ITIN lenders use “Alternative Credit” instead. This means they look at your history of paying rent, electricity, and phone bills to decide if you are trustworthy.

Will these loans cost more than a regular loan?

Often, yes. Because the lender cannot easily sell the loan to the government or check a standard credit score, they take more risk. They charge a higher interest rate or require a larger down payment to cover that risk.

What is the minimum income required?

There is no single number. It depends on the loan size. However, you must prove your income is steady. Lenders usually require your last two years of tax returns (W-7) or 3 months of bank statements to prove stability.

Can I apply for these loans online?

Yes, but be careful. Many online lenders accept ITINs, but some are predatory. Always check the interest rate (APR) before applying. We recommend starting with a local Credit Union first, even if you have to visit in person.

What specific loans can I get?

You have access to almost every major loan type. This includes mortgages (home loans), car financing, personal emergency loans, and business start-up capital.

1 Comment

ITIN Personal Loans: How To Qualify, Apply, And Get Funded - Look Up Loans · December 29, 2025 at 3:46 am

[…] you understand how to manage short-term debt, you are ready to look at the long-term goal. Read our Master Guide to ITIN Loans to learn how to prepare for buying a […]