Introduction

A secured loan for bad credit can be a lifeline for borrowers struggling to get approved for traditional financing.

Instead of being denied based on your credit score, a secured loan allows you to use an asset such as a car, savings, or home equity as collateral to secure funding. This reduces the lender’s risk and increases your chances of approval, often with lower interest rates and higher loan amounts than unsecured loans.

In this guide, we’ll cover everything you need to know about the best secured loans for bad credit, lender comparisons, and how to improve your chances of approval.

Key Takeaways

- Secured loans require collateral, such as a car, savings account, or home equity.

- Lenders offer lower interest rates and higher loan amounts compared to unsecured loans.

- Ideal for borrowers with bad credit who struggle to get approved for traditional financing.

- Approval is based on collateral value, income, and repayment ability, not just credit score.

- Failure to repay can result in losing your collateral, making responsible borrowing essential.

- Top secured loan lenders include OneMain Financial, Upgrade, Navy Federal Credit Union, LightStream, and Wells Fargo.

Disclaimer: This site contains affiliate links. If you make a purchase, we may earn a commission at no extra cost to you.

How Secured Loans Work

Secured loans give you a second chance when your credit score is working against you.

Instead of getting denied because of your credit history, you offer collateral, a vehicle, savings account, or home equity that reduces the lender’s risk. That risk shift changes everything. It means lenders are more willing to say yes, and often with better terms than you’d get with an unsecured loan.

Here’s what makes them different:

- Approval is based on asset value, not just credit score

- Interest rates are typically lower than personal loans for bad credit

- Loan amounts are higher, tied to your collateral’s worth

- Repayment terms are more flexible, depending on the lender

But the tradeoff is real. If you can’t repay the loan, the lender can seize the asset you put up. That’s why secured loans only make sense if you’ve got a clear repayment plan and you’re not borrowing more than you can manage.

This structure makes secured loans one of the few reliable paths to funding for bad credit borrowers but only if you understand what you’re offering and what’s at stake.

Top Secured Loan Lenders Compared

Not all secured loans are created equal. Some lenders accept cars or savings accounts as collateral. Others focus on speed, flexible terms, or helping bad credit borrowers rebuild trust.

That’s why comparing your options matters especially when your credit score already limits what you can qualify for.

Below, we’ve broken down the best secured loan providers for bad credit in 2025, including:

- Loan amounts

- Collateral requirements

- APR ranges

- Repayment terms

- What kind of borrower each lender works best for

Use this section to find the lender that matches your situation, not just the one offering the biggest number.

1. OneMain Financial

Best for: Bad credit borrowers who need quick, in-person support

- Loan Amounts: $1,500 – $20,000

- APR Range: 18.00% – 35.99%

- Collateral Accepted: Vehicle titles

- Repayment Terms: 24 to 60 months

OneMain Financial is one of the most accessible secured lenders for people with bad credit and they don’t shy away from high-risk borrowers.

Instead of relying on your credit score alone, OneMain lets you back your loan with a car title. That gives you a stronger shot at approval, and may qualify you for better rates than an unsecured loan from the same lender.

Another edge? Physical branches. If you’re not comfortable applying entirely online, you can walk into a local office and speak with a loan officer face-to-face.

But the tradeoff is cost. Interest rates can be steep, and loan terms aren’t always flexible. That makes OneMain a strong option only if you need funds fast, have limited online access, or want to speak directly with someone during the process.

If you’re confident in your ability to repay and your car has enough value, OneMain can work, just be sure to run the numbers first.

2. Upgrade

Best for: Bad credit borrowers who want lower APRs and flexible repayment options

- Loan Amounts: $1,000 – $50,000

- APR Range: 8.49% – 35.99%

- Collateral Accepted: Vehicles, personal assets

- Repayment Terms: 24 to 84 months

Upgrade offers secured personal loans that work well for borrowers trying to rebuild credit without getting buried in high interest.

Their secured loan program lets you use a vehicle or other personal asset as collateral giving you access to lower APRs than you’d see on most unsecured loans.

What stands out is flexibility. Upgrade offers longer terms (up to 7 years), which can help lower your monthly payments if you’re working with a tight budget. Their online application process is fast and user-friendly, making them a solid choice for people who want to avoid banks or in-person meetings.

But keep in mind: approval still depends on more than just collateral. If your income is inconsistent or your debt-to-income ratio is high, you may not get the best terms even if your asset qualifies.

If you’re looking for a balanced secured loan with more breathing room on repayment, Upgrade is worth considering.

3. Navy Federal Credit Union

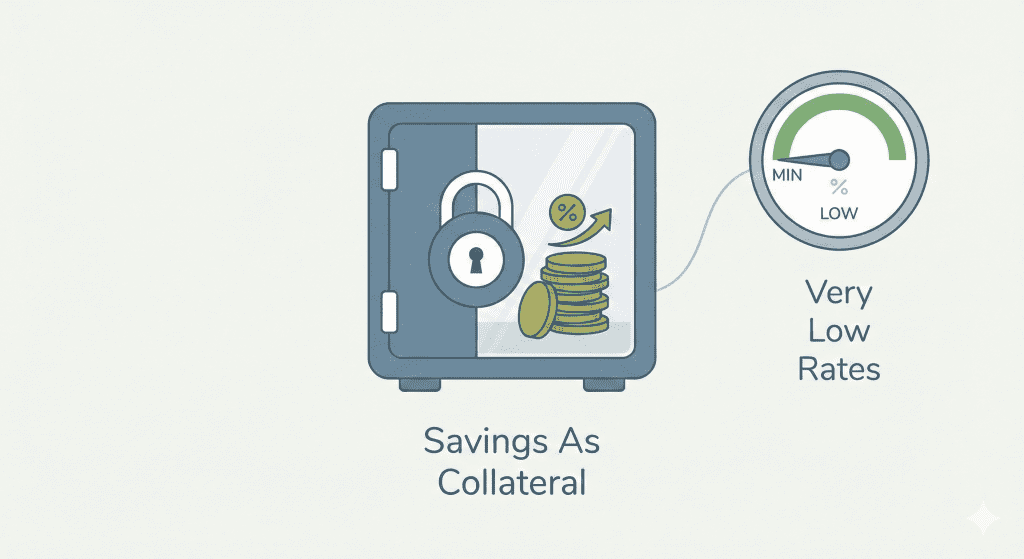

Best for: Military members and families who want ultra-low rates using savings as collateral

- Loan Amounts: $250 – $100,000

- APR Range: Starting at 2.05%

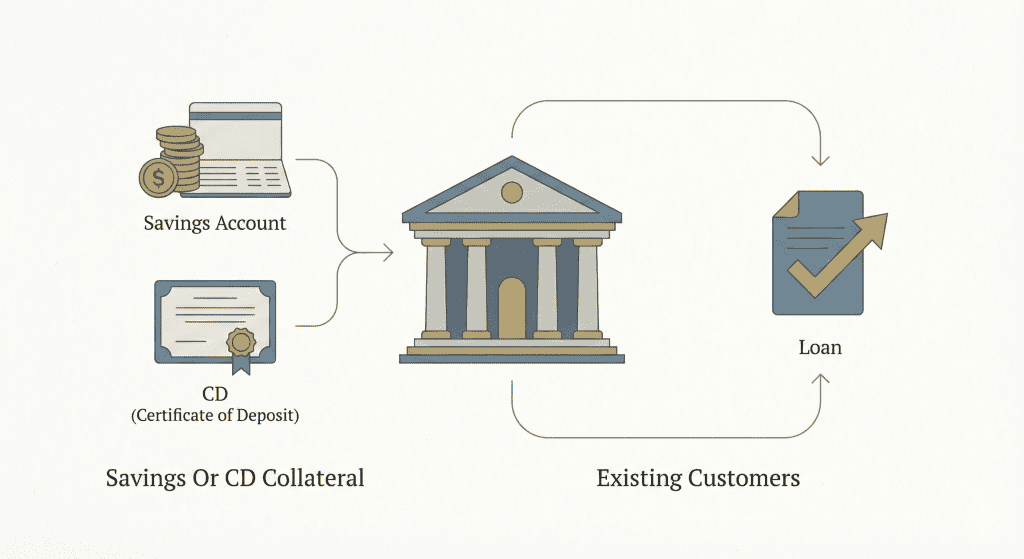

- Collateral Accepted: Savings accounts, Certificates of Deposit (CDs)

- Repayment Terms: Varies by loan type

Navy Federal Credit Union offers some of the lowest secured loan rates in the country but it’s only available to military members, veterans, and their families.

What makes this option stand out isn’t just the low starting APR. It’s how NFCU structures the loan: you can secure it using your own savings account or CD, and those funds continue to earn interest while held as collateral.

That means you get funding, build credit, and your money keeps working in the background, a triple benefit most lenders don’t offer.

The downside? Your savings or CD will be frozen until the loan is repaid. And if you’re not eligible for membership, you’re out of luck.

For qualified borrowers, though, this is easily one of the safest and most cost-effective ways to borrow with bad credit.

4. LightStream

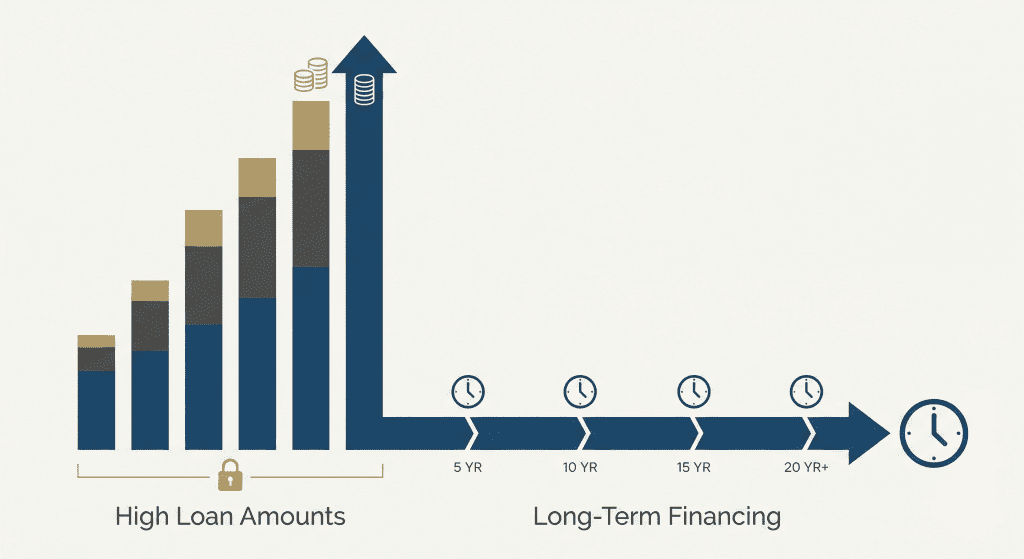

Best for: Borrowers with strong financials who need high loan amounts

- Loan Amounts: $5,000 – $100,000

- APR Range: 6.99% – 24.99%

- Collateral Accepted: High-value personal assets or home equity

- Repayment Terms: 24 to 144 months

LightStream isn’t built for everyone especially not for borrowers with unstable income or very low credit scores. But if you have solid financials and valuable assets, it offers some of the best secured loan terms available.

This division of Truist Bank focuses on high-limit loans with long repayment terms, going up to 12 years. That makes it ideal for large expenses like home improvements, medical costs, or consolidating bigger debts.

The key advantage: competitive interest rates even on large balances but only if your credit profile and collateral are strong enough to qualify.

Don’t expect hand-holding or flexible approval. LightStream doesn’t accept co-signers, and they rarely approve applicants with spotty financial history.

Bottom line: If your credit is recovering but your income is stable and your asset is valuable, LightStream can deliver serious funding at fair rates.

5. Wells Fargo

Best for: Existing Wells Fargo customers using savings or CDs as collateral

- Loan Amounts: $3,000 – $100,000

- APR Range: 5.99% – 22.99%

- Collateral Accepted: Savings accounts, Certificates of Deposit (CDs)

- Repayment Terms: Up to 84 months

Wells Fargo is one of the few traditional banks still offering secured personal loans but access is limited. These loans are typically available only to existing Wells Fargo customers, and they’re not actively promoted online.

What makes them worth considering is the structure. Like Navy Federal, you can back your loan with a savings account or CD. This often leads to lower rates and better terms compared to unsecured options, especially if you have a strong banking history with them.

Loan amounts are generous, repayment terms are flexible, and rates can be competitive. But don’t expect the same streamlined experience you’d get with online lenders; you’ll likely need to speak with a banker or visit a branch to explore your options.

For long-time Wells Fargo clients with cash on hand and bad credit, this can be a smart, low-risk way to secure funding.

Which Secured Loan Lender Is Right for You?

You’ve seen the details but side-by-side comparison makes it easier to spot what actually fits your situation. Use the table below to compare the best secured loan options for bad credit in terms of loan size, APR range, collateral type, and who each lender is best suited for. Focus on the match, not just the numbers.

| Lender | Best For | Collateral Required | Loan Amounts | APR Range |

|---|---|---|---|---|

| OneMain Financial | Borrowers with bad credit needing quick funds | Car title | $1,500 – $20,000 | 18.00% – 35.99% |

| Upgrade | Borrowers looking for lower APRs | Personal assets, vehicles | $1,000 – $50,000 | 8.49% – 35.99% |

| Navy Federal Credit Union | Military members and families | Savings accounts, CDs | $250 – $100,000 | Starting at 2.05% |

| LightStream | Borrowers needing large loan amounts | Various high-value assets | $5,000 – $100,000 | 6.99% – 24.99% |

| Wells Fargo | Existing Wells Fargo customers | Savings accounts, CDs | $3,000 – $100,000 | 5.99% – 22.99% |

Each lender has different loan limits, interest rates, and collateral requirements.

The best choice depends on your financial situation, the collateral you can provide, and the loan terms that fit your needs.

How to Apply for a Secured Loan with Bad Credit

Applying for a secured loan with bad credit requires careful preparation.

While secured loans are easier to qualify for than unsecured loans, lenders still assess factors like income, collateral value, and ability to repay before approving an application.

Here’s a step-by-step guide to help you navigate the application process and increase your approval chances.

1. Determine Your Loan Needs

Before applying, ask yourself:

- How much money do you need? Borrow only what you can afford to repay.

- What will you use as collateral? Choose an asset that meets the lender’s requirements.

- How soon do you need the funds? Some lenders offer same-day funding, while others take longer.

- What repayment term works best for you? Shorter terms mean higher payments but lower interest costs, while longer terms mean smaller payments but more interest over time.

Understanding your financial needs before applying will help you select the right lender and loan type.

2. Check Your Credit Score

Even though secured loans focus on collateral, lenders still review your credit score to assess risk. Knowing your score in advance helps you:

- Identify lenders that fit your credit profile (some lenders have minimum credit score requirements).

- Check for errors on your credit report and correct them before applying.

- Avoid unnecessary rejections by applying only to lenders that align with your financial situation.

If your credit score is below 580, consider improving it by paying down existing debt or making on-time payments before applying.

3. Compare Lenders and Loan Terms

Not all lenders offer the same terms, even if they accept bad credit borrowers. When comparing secured loan options, look at:

- Loan amounts: Minimum and maximum limits

- Interest rates: Lower is better, but rates depend on creditworthiness

- Collateral requirements: Some lenders only accept vehicles, while others accept savings accounts or other assets

- Repayment terms: Short-term vs. long-term options

- Fees: Origination fees, late fees, and prepayment penalties

Example: If you need $10,000 and want the lowest possible interest rate, Navy Federal Credit Union (for eligible members) may be a better option than OneMain Financial, which has higher APRs.

4. Gather Required Documents

- Lenders will ask for documents to verify your identity, income, and collateral ownership. Be prepared to provide:

- Government-issued ID (driver’s license, passport)

- Proof of income (pay stubs, tax returns, bank statements)

- Collateral documentation (vehicle title, savings account statement, home appraisal)

- Proof of residence (utility bill, lease agreement)

Having these documents ready speeds up the approval process and reduces delays.

5. Submit Your Loan Application

Most lenders allow online applications, but some require in-person visits (e.g., OneMain Financial and Wells Fargo). When filling out your application:

- Be accurate with personal and financial details.

- Ensure your collateral meets the lender’s requirements.

- Double-check all information before submitting to avoid rejections due to errors.

Some lenders offer prequalification, allowing you to see potential loan offers without affecting your credit score.

6. Wait for Approval and Collateral Evaluation

Approval time varies by lender:

- Online lenders like Upgrade may provide a decision within 24 hours.

- Traditional banks like Wells Fargo may take a few days to process applications.

- Lenders requiring collateral appraisal (such as car title loans) may take longer.

During this stage, the lender assesses the value of your collateral to ensure it meets the loan requirements.

7. Review Loan Terms Before Accepting

Once approved, carefully review:

- Interest rate and total loan cost

- Monthly payment amount and due date

- Repayment period and early payoff options

- Collateral terms and repossession policies

Never sign a loan agreement without fully understanding the terms. If anything seems unclear, ask the lender for clarification.

8. Receive Funds and Begin Repayments

Once you accept the loan terms:

- Funds are deposited into your account (timing varies by lender).

- Repayments start according to the agreed schedule (weekly or monthly).

- Set up automatic payments to avoid late fees and potential damage to your credit score.

How to Increase Your Approval Chances

If you want to improve your chances of getting approved with better loan terms:

- Offer a valuable asset – Lenders prefer collateral with a stable value, such as savings accounts or high-value vehicles.

- Choose a lender that specializes in bad credit loans – Some lenders are more flexible than others.

- Apply for a smaller loan amount – Asking for less reduces lender risk.

- Consider a co-signer – A co-signer with better credit can strengthen your application.

- Reduce existing debt – Lowering your debt-to-income ratio can make approval easier.

A secured loan can be an effective way to get financing with bad credit, but it’s essential to borrow responsibly and understand the risks involved.

Alternative Financing Options Beyond Secured Loans

Secured loans are a great option for borrowers with bad credit, but they’re not the only choice.

If you’re hesitant to use collateral or want to explore other ways to secure funding, several alternatives may work better for your situation.

Below are alternative financing options, along with their benefits and potential drawbacks.

1. Credit Union Loans

How They Work:

Credit unions often offer personal loans with more flexible approval criteria compared to traditional banks. Many credit unions provide secured and unsecured loans at lower interest rates, and they may be more willing to approve borrowers with bad credit if they have a history of responsible banking.

Pros:

Lower interest rates than traditional banks

More lenient credit requirements

Personalized service and local decision-making

Cons:

Must be a credit union member to apply

Loan amounts may be smaller than secured loans

Some credit unions require savings deposits before loan approval

Best for: Borrowers who are credit union members or willing to join one and prefer a relationship-based lending approach.

2. Peer-to-Peer (P2P) Lending

How It Works:

Peer-to-peer lending platforms connect borrowers directly with individual investors rather than banks. Borrowers submit loan applications, and investors fund the loan based on risk assessment.

Popular P2P lending platforms include:

- LendingClub

- Prosper

- Upstart

Pros:

- Loans may be available for borrowers with lower credit scores

- Competitive interest rates based on risk level

- Online application with quick funding

Cons:

- Interest rates may be higher for bad credit borrowers

- Not all applications receive full funding

- Fees may apply for loan origination or late payments

Best for: Borrowers who want to avoid traditional banks and prefer an alternative online lending platform.

3. Secured Credit Cards

How They Work:

A secured credit card works similarly to a secured loan, but instead of receiving a lump sum of cash, borrowers put down a refundable deposit that serves as their credit limit. Over time, responsible use can help build or repair credit, making future borrowing easier.

Pros:

- Helps improve credit score with responsible use

- Lower risk than traditional secured loans

- No need for income verification in most cases

Cons:

- Requires an upfront cash deposit

- Low credit limits compared to personal loans

- Some cards have high fees

Best for: Individuals who need to build or rebuild credit before applying for larger loans.

4. Co-Signed Loans

How They Work:

A co-signed loan allows borrowers with bad credit to qualify for financing by adding a co-signer with good credit. The co-signer takes equal responsibility for the loan, reducing risk for the lender.

Pros:

- Lower interest rates due to co-signer’s strong credit

- Higher approval chances for borrowers with bad credit

- Can help improve credit score with on-time payments

Cons:

- Co-signer is responsible if the borrower fails to repay

- Could damage both parties’ credit if payments are missed

- Not all lenders accept co-signers for secured loans

Best for: Borrowers who have a trusted family member or friend with good credit willing to co-sign.

5. Home Equity Loans and HELOCs

How They Work:

Homeowners with equity in their property can borrow against their home’s value through a home equity loan (lump sum) or a home equity line of credit (HELOC).

These loans typically offer lower interest rates than personal loans but require using the home as collateral.

Pros:

- Lower interest rates than most personal loans

- Large borrowing amounts available

- Flexible repayment terms

Cons:

- Risk of foreclosure if you cannot repay

- Requires sufficient home equity

- Longer approval process

Best for: Homeowners who need larger loan amounts at lower rates and are comfortable using their home as collateral.

6. Payday Alternative Loans (PALs)

How They Work:

Some credit unions offer Payday Alternative Loans (PALs), which are small-dollar loans designed as a safer alternative to payday loans.

These loans typically have lower fees and interest rates and must be repaid within a short period.

Pros:

- Lower interest rates than traditional payday loans

- Fast approval and funding

- Regulated by the National Credit Union Administration (NCUA)

Cons:

- Low loan amounts (usually up to $2,000)

- Short repayment terms (1 to 12 months)

- Requires credit union membership

Best for: Borrowers who need small, short-term loans but want to avoid payday loan traps.

7. Employer-Based Loan Programs

How They Work:

Some employers offer paycheck advance programs or employee loans as a benefit to workers.

These programs allow employees to borrow small amounts against their future paycheck, often at little to no interest.

Pros:

- No credit check required

- Fast approval and direct paycheck deductions

- Interest-free or low-cost borrowing options

Cons:

- Loan amounts are typically small

- Limited to employers who offer this benefit

- Reduces future paychecks

Best for: Employees who need short-term financial relief without high-interest borrowing.

Which Alternative is Best for You?

| Alternative Loan Option | Best For | Main Benefits | Potential Downsides |

|---|---|---|---|

| Credit Union Loans | Credit union members | Lower rates, flexible approval | Membership required, smaller loan limits |

| Peer-to-Peer Lending | Borrowers seeking online funding | May approve bad credit applicants | Higher rates for bad credit, funding not guaranteed |

| Secured Credit Cards | Credit-building | Improves credit with responsible use | Requires a security deposit, low limits |

| Co-Signed Loans | Borrowers with a co-signer | Lower rates, better approval chances | Co-signer is responsible for repayment |

| Home Equity Loans/HELOCs | Homeowners | Low rates, large loan amounts | Risk of foreclosure, longer approval process |

| Payday Alternative Loans (PALs) | Small-dollar emergency loans | Lower rates than payday loans | Limited availability, short terms |

| Employer-Based Loans | Employees with financial hardship | No credit check, quick access | Reduces future paychecks |

Alternative Financing Options

Secured loans for bad credit can be a useful tool, but they are not the only option. If you:

- Do not want to risk collateral, consider credit union loans, peer-to-peer lending, or co-signed loans.

- Need to build or repair credit, a secured credit card can help establish positive payment history.

- Own a home with equity, a home equity loan or HELOC may offer lower interest rates and larger loan amounts.

- Need a short-term emergency loan, consider Payday Alternative Loans (PALs) or employer-based loan programs.

Choosing the right financing option depends on your financial situation, borrowing needs, and risk tolerance.

Carefully compare your choices and ensure you can meet repayment terms before committing to any loan.

Final Thoughts

Before taking out a secured loan, it’s important to weigh your options and understand the details.

Compare different lenders to find the best rates and loan terms.

Make sure your collateral meets lender requirements and is valued fairly.

Only borrow what you know you can repay to avoid financial stress. A secured loan can be a great option when used wisely, but it’s not without risks.

Take the time to read the fine print and be sure it’s the right fit before committing.

Frequently Asked Questions (FAQs)

Can I Get Approved for a Secured Loan with Bad Credit?

Yes. Since secured loans use collateral, lenders are more willing to approve borrowers with low credit scores. However, your income, collateral value, and repayment ability still play a role in approval.

Who Offers the Best Secured Loans?

The best lender depends on your collateral type and loan needs:

- OneMain Financial: Best for borrowers with bad credit needing car title loans.

- Upgrade: Best for lower APRs and flexible repayment.

- Navy Federal Credit Union: Best for military members using savings as collateral.

- LightStream: Best for large loan amounts with competitive APRs.

- Wells Fargo: Best for existing customers using savings accounts as collateral.

What Credit Score is Needed for a Secured Loan?

There is no fixed minimum since secured loans depend more on collateral value. However:

- 580+ Credit Score: Better rates and higher approval chances.

- Below 580: May still qualify but may face higher APRs or stricter loan terms.

Can I Be Denied for a Secured Loan?

Yes, even with collateral, a lender can deny your application for reasons such as:

- Insufficient collateral value (not worth enough to secure the loan).

- Low income or high debt-to-income ratio (risk of default).

- Past loan defaults or bankruptcies on your credit history.

To improve approval odds, offer high-value collateral and show stable income.

What Happens If I Can’t Repay My Secured Loan?

- Missed payments can hurt your credit score.

- Lender may repossess and sell your collateral.

- Some lenders allow restructuring or payment deferrals contact them before missing a payment.

How Quickly Can I Get a Secured Loan?

Approval time varies by lender:

- Online lenders (Upgrade, LightStream): 1-2 business days.

- Banks & credit unions: 3-7 business days.

- Car title loans (OneMain Financial): Same-day funding possible.

Can I Use a Secured Loan to Pay Off Debt?

Yes, many borrowers use secured loans for debt consolidation. However, ensure the new loan offers lower interest rates than your current debts.

- Good Idea: If you get a lower APR secured loan to replace high-interest debt.

- Bad Idea: If you risk losing collateral while still struggling to make payments.

Is a Secured Loan Bad for My Credit?

A secured loan can help or hurt your credit depending on how you manage payments:

- Helps Credit: On-time payments improve your score over time.

- Hurts Credit: Late or missed payments damage your score.

0 Comments