Introduction

Payday Alternative Loans, often called PALs, give credit union members a safer way to borrow small amounts of money when cash is tight. They are designed to help borrowers avoid traditional payday loans, which can come with high costs, short repayment windows, and repeat borrowing risk.

A PAL is not a cash advance from a payday lender. It is a small-dollar loan offered by some federal credit unions under rules set by the National Credit Union Administration. The loan gives you a set amount, a clear repayment term, and a structured payment plan.

This guide explains how Payday Alternative Loans work, how PAL I and PAL II differ, who may qualify, what they can cost, and when a PAL makes sense compared with other short-term borrowing options.

Key Takeaways

- Payday loans may be fast, but the repayment can put pressure on your next paycheck.

- The best payday loan alternative depends on how much you need, how fast you need it, and what repayment will do to your budget.

- Some alternatives help you avoid borrowing, such as bill extensions, payment plans, local assistance, or employer support.

- Credit unions may offer small-dollar loans or Payday Alternative Loans with clearer repayment terms than many payday loans.

- Cash advance apps and paycheck advances can help with small gaps, but they still need a repayment plan.

- Before choosing any option, compare the fees, timing, total cost, and what happens if you cannot pay on time.

- If you need short-term cash every month, a loan may only cover the symptom. You may need a bigger fix, such as bill negotiation, budgeting help, or local support.

Disclaimer: This site contains affiliate links. If you make a purchase, we may earn a commission at no extra cost to you.

What Payday Alternative Loans Actually Are

Payday Alternative Loans are small-dollar loans offered by some federal credit unions. They are designed for borrowers who need short-term cash but want a safer option than a traditional payday loan.

A PAL gives you a fixed loan amount, a set repayment term, and scheduled payments. In plain English, that means you know how much you are borrowing, when payments are due, and how long you have to pay the loan back.

PALs are not the same as payday loans. Payday loans usually come from storefront or online payday lenders. PALs come from participating federal credit unions and follow specific rules around loan size, fees, repayment terms, and repeat borrowing.

That does not mean every PAL is automatically the right choice. You still need to check the cost, payment schedule, and whether the credit union offers the loan in the first place.

The simplest way to think about it is this: a payday loan is often built around fast cash, while a PAL is built around a clearer repayment plan. If you need short-term cash but want more predictable terms, a PAL may be worth checking before turning to a payday lender.

Why PALs Exist for Borrowers Who Need Short-Term Cash

PALs exist because many people need a small amount of money before their next paycheck, but traditional payday loans can be risky.

The problem is not just borrowing money. The problem is borrowing money with a short deadline, high costs, and little room to recover if your next paycheck is already spoken for.

A payday loan may seem like a quick fix when rent is due, the car breaks down, or a utility bill cannot wait. But if the repayment takes too much from your next paycheck, you may have to borrow again just to cover regular expenses.

That is the cycle PALs are meant to help borrowers avoid.

A Payday Alternative Loan gives credit union members a more structured option. Instead of focusing only on fast cash, PALs are built around clearer limits, scheduled repayment, and rules that reduce repeat borrowing.

This does not make PALs free money or risk-free debt. You still have to repay the loan, and the payment still needs to fit your budget.

The purpose is simple: PALs give borrowers a safer place to start when they need short-term cash but do not want to rely on a high-cost payday loan.

How PALs Work Through Federal Credit Unions

PALs are offered through participating federal credit unions. That means you usually need to join the credit union before you can apply.

Not every credit union offers PALs, so the first step is simple: ask whether the credit union has a Payday Alternative Loan program. Some may offer PALs, while others may offer different small-dollar loans instead.

The process usually works like this:

- You become a credit union member, if you are not one already.

- You ask whether the credit union offers PALs.

- You apply for the loan and provide basic information.

- The credit union reviews your ability to repay.

- If approved, you receive the loan and repay it through scheduled payments.

The credit union may look at your income, account history, current debt, and overall ability to make payments. The goal is not just to approve you. The goal is to make sure the loan fits your situation.

A PAL also has limits. The credit union cannot simply lend any amount, charge any fee, or set any repayment schedule it wants. PALs follow rules that shape how much you can borrow, how long repayment can last, and how the loan is structured.

This is where PALs can feel different from payday loans. You are working with a credit union that already has rules around the loan, instead of a lender built mainly around fast cash.

Still, approval is not automatic. You need to qualify, and the credit union must offer the loan. If your credit union does not offer PALs, ask whether it has another small-dollar loan, hardship loan, or emergency loan option.

Next, it helps to understand the two main PAL types: PAL I and PAL II. They have different rules, and those rules can shape which option fits your situation.

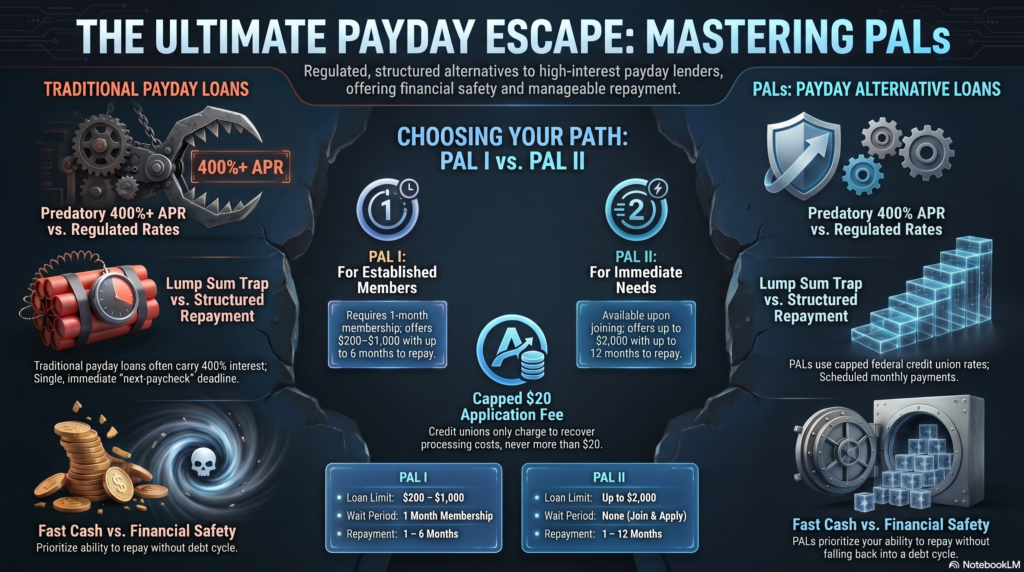

PAL I vs. PAL II: The Rules That Shape Your Loan Options

PALs come in two main versions: PAL I and PAL II. Both are offered by participating federal credit unions, but they are not exactly the same.

The biggest differences are the loan amount, how soon you can apply after joining the credit union, and how long you may have to repay the loan.

| Feature | PAL I | PAL II |

|---|---|---|

| Loan amount | $200 to $1,000 | Up to $2,000 |

| Membership requirement | You must be a credit union member for at least one month before applying | You may be able to apply as soon as you become a member |

| Repayment term | One to six months | One to 12 months |

| Application fee | May be charged, but cannot be more than $20 | May be charged, but cannot be more than $20 |

| Rollovers | Not allowed | Not allowed |

| Best for | Smaller short-term needs when you already belong to a credit union | Larger short-term needs or borrowers who recently joined a credit union |

The rules for PAL I and PAL II loans come from the National Credit Union Administration, which regulates federal credit unions and sets the framework for loan amounts, application fees, repayment terms, and membership timing.

PAL I is the older and smaller version. It may work if you already belong to a credit union and need a smaller amount of money for a short-term expense.

PAL II gives credit unions more flexibility. It can allow a larger loan amount and a longer repayment term, which may make the payment easier to manage.

The important thing to remember is that your credit union decides what it offers. Some credit unions may offer PAL I, some may offer PAL II, and some may not offer PALs at all.

Before you apply, ask the credit union three simple questions:

- Do you offer PAL I, PAL II, or both?

- How much can I borrow?

- What would my payment schedule look like?

This helps you understand the loan before you apply, instead of guessing from the name alone.

What PALs Cost Compared With Payday Loans

PALs usually cost less than payday loans because they have limits on interest, fees, and repayment terms. They are also repaid through scheduled payments instead of one short payoff deadline.

A federal credit union may charge interest on a PAL, but the rate must follow federal credit union rules. The credit union may also charge an application fee, but that fee cannot be more than $20 and must be tied to the cost of processing the application.

Payday loans often work differently. The cost is usually shown as a fee for every $100 borrowed, which can make the loan look smaller than it really is. The CFPB says a common payday loan fee is $15 for every $100 borrowed, which can equal an APR of almost 400% on a two-week loan.

The real difference is how the cost hits your budget.

With a payday loan, the full amount may come due very quickly. If that payment takes too much from your next paycheck, you may need to borrow again.

With a PAL, repayment is spread across a set term. That can give you more room to plan, especially if the payment fits your regular budget.

A PAL is not free money, and it is not always the cheapest option. You still need to check:

- The APR

- The application fee

- The payment amount

- The repayment term

- The total amount you will repay

- Whether the credit union offers a cheaper option

The safer choice is not just the loan with the lowest fee. It is the loan that gives you a clear cost, a realistic payment, and enough breathing room to avoid borrowing again.

The Consumer Financial Protection Bureau notes that a common payday loan fee of $15 per $100 borrowed can equal an APR of almost 400% on a two-week loan, which is why comparing the full cost matters before borrowing.

Who Qualifies for a Payday Alternative Loan

To qualify for a Payday Alternative Loan, you usually need to be a member of a federal credit union that offers PALs. That is the first thing to check because not every credit union has this type of loan.

Membership rules depend on the credit union. Some serve people who live in a certain area, work for a certain employer, belong to a certain group, or have a family connection to an existing member.

Once you qualify for membership, the credit union may review your loan request.

Credit Union Membership

You need to join the credit union before you can get a PAL. For PAL I, you usually need to be a member for at least one month before applying.

PAL II may be different. Some credit unions may let you apply for PAL II as soon as you become a member.

That is why it helps to ask the credit union which version it offers before you start the application.

Income and Ability to Repay

The credit union wants to know that you can pay the loan back. You may need to show income from a job, benefits, retirement payments, self-employment, or another regular source.

You do not need to have a perfect financial life. But the credit union still needs to see that the payment will not put too much pressure on your budget.

Loan Amount Limits

PALs are small-dollar loans, so they are not meant for large expenses. They are usually used for short-term needs like car repairs, utility bills, medical costs, or emergency gaps between paychecks.

Before applying, know how much you actually need. Borrowing more than necessary can make repayment harder.

Credit Union Approval

Joining a credit union does not guarantee approval. The credit union may look at your income, account history, current debts, and past borrowing behavior.

This review can protect both sides. It helps the credit union decide whether the loan is reasonable, and it helps you avoid taking on a payment that does not fit your budget.

What to Ask Before You Apply

Before starting the application, ask the credit union:

- Do you offer PAL I, PAL II, or both?

- How long do I need to be a member before applying?

- What loan amounts are available?

- What fees do you charge?

- What will the repayment schedule look like?

- Do you offer other small-dollar loans if I do not qualify?

A PAL can be easier to understand than many high-cost short-term loans, but you still need to qualify. The best first step is to contact the credit union, confirm that PALs are available, and ask what the application requires.

When a PAL Makes Sense and When It Does Not

A PAL can make sense when you need a small amount of money for a real short-term expense and want to avoid a high-cost payday loan. It works best when the loan amount covers the problem, the repayment schedule fits your budget, and you can pay it back without falling behind on other bills.

A PAL may be a good fit if you need help with a car repair, utility bill, medical cost, or another expense that cannot wait. It can also be useful if you already belong to a federal credit union that offers PALs or can join one without a long delay.

A PAL may make sense when:

- You need a small loan for a short-term expense.

- You want an alternative to a payday loan.

- You belong to a credit union that offers PALs.

- You can afford the scheduled payments.

- You understand the APR, fees, and repayment term.

- You only need to borrow a limited amount.

A PAL may not be the right fit if your credit union does not offer them, the loan limit is too small, or you need money faster than the credit union can approve the loan. It may also be the wrong choice if the payment would make rent, groceries, utilities, or other basic bills harder to cover.

A PAL may not make sense when:

- Your credit union does not offer PALs.

- You need more than the loan limit allows.

- You cannot afford the scheduled payments.

- You need money immediately and cannot wait for approval.

- A grant, payment plan, or employer advance would solve the problem without new debt.

- You are using short-term loans repeatedly to cover regular bills.

The key is to treat a PAL as a bridge, not a habit. It can help with a temporary cash shortage, but repeated borrowing may point to a larger budget problem that needs a different solution.

Common Mistakes to Avoid Before Applying for a PAL

A PAL can be a safer option than a payday loan, but only if you use it carefully. The loan still needs to fit your budget, and the terms still need to make sense before you apply.

Assuming Every Credit Union Offers PALs

Not every federal credit union offers Payday Alternative Loans. Some offer PAL I, some offer PAL II, some offer both, and some do not offer PALs at all.

Before you plan around a PAL, call the credit union and ask what small-dollar loan options are available.

Looking Only at the Loan Amount

The amount you can borrow matters, but it is not the only thing to check. You also need to know the payment amount, repayment term, APR, and any application fee.

A loan can cover your emergency and still be a poor fit if the payment is too hard to manage.

Borrowing More Than You Need

A PAL is meant to solve a short-term cash problem. Borrowing extra can raise your payment and make the loan harder to repay.

Start with the exact amount you need. If the expense is $600, do not borrow more unless you have a clear reason and a safe repayment plan.

Ignoring the Payment Schedule

Before you accept the loan, make sure you know when each payment is due. The payment should fit around your normal bills, not compete with them.

If the payment would make it hard to cover rent, groceries, utilities, or transportation, the loan may not be the right fit.

Using PALs Again and Again

A PAL can help with a one-time emergency. It should not become a regular way to cover monthly bills.

If you keep needing short-term loans, the real problem may be a budget gap. In that case, a payment plan, local assistance program, or credit counseling support may help more than another loan.

Not Comparing Other Options

A PAL may be a good choice, but it is still worth checking other low-cost options. Your credit union may offer another small loan, hardship loan, or payment plan that fits better.

The goal is not just to avoid payday loans. The goal is to choose the option that solves the problem with the least stress on your budget.

A Real-World Example of How a PAL Could Help

Imagine Maria needs $600 for an urgent car repair. She needs the car to get to work, but she does not have enough cash to cover the bill today.

One option is a payday loan. It may be fast, but the repayment could come due very quickly. If that payment takes too much from her next paycheck, she may need to borrow again to cover rent, groceries, or gas.

Another option is a PAL through her credit union. If Maria qualifies, she may be able to borrow the $600 and repay it through scheduled payments over several months.

That gives her a clearer plan:

- She knows how much she borrowed.

- She knows when payments are due.

- She knows how long repayment will take.

- She has time to fit the payment into her regular budget.

The PAL does not erase the cost of the repair. Maria still has to repay the loan. The difference is that the loan is structured around a payment plan instead of a quick payoff that may leave her short again.

This is where a PAL can help most. It gives borrowers a way to handle a short-term expense without turning one emergency into a repeat borrowing cycle.

Conclusion

Payday Alternative Loans can give credit union members a safer way to handle short-term cash needs. They are not free money, but they offer more structure than many traditional payday loans.

The biggest advantage is clarity. With a PAL, you can see the loan amount, repayment term, fees, and payment schedule before you agree. That makes it easier to plan and harder to get pulled into a repeat borrowing cycle.

Still, a PAL is not the right fit for everyone. Your credit union must offer the loan, you need to qualify, and the payment must fit your budget.

Before applying, ask your credit union which PAL options are available, how much you can borrow, what the loan will cost, and when payments are due. If the terms are clear and the payment is manageable, a PAL may be a smart place to start before considering a payday loan.

Frequently Asked Questions About Payday Alternative Loans

What does PAL stand for?

PAL stands for Payday Alternative Loan. It is a small-dollar loan offered by some federal credit unions as an alternative to traditional payday loans.

Are Payday Alternative Loans the same as payday loans?

No. Payday Alternative Loans come from participating federal credit unions, not payday lenders. PALs follow federal credit union rules around loan amounts, fees, repayment terms, and repeat borrowing.

Do all credit unions offer PALs?

No. Not every credit union offers PALs. Some may offer PAL I, PAL II, both options, or a different small-dollar loan instead.

What is the maximum amount you can borrow with a PAL?

PAL I loans can range from $200 to $1,000. PAL II loans can go up to $2,000 through participating federal credit unions.

What is the difference between PAL I and PAL II?

PAL I is smaller and usually requires at least one month of credit union membership before you apply. PAL II can allow a larger loan amount, a longer repayment term, and may be available as soon as you become a credit union member.

Can you get a PAL with bad credit?

You may be able to get a PAL with bad credit, but approval is not guaranteed. The credit union may review your income, account history, current debt, and ability to repay before making a decision.

How fast can you get a Payday Alternative Loan?

The timeline depends on the credit union. Some borrowers may need to join the credit union first, confirm that PALs are available, submit an application, and wait for approval before receiving funds.

How much does a PAL cost?

A PAL may include interest and an application fee. Federal credit unions may charge an application fee only to recover processing costs, up to $20.

Are PALs cheaper than payday loans?

PALs are often designed to be a lower-cost alternative, but you still need to compare the full cost. The CFPB says a common payday loan fee of $15 per $100 borrowed can equal an APR of almost 400% on a two-week loan.

Are PALs better than cash advance apps?

It depends on the cost, speed, and repayment setup. A PAL may offer a clearer loan structure through a credit union, while a cash advance app may be faster for a smaller gap. Compare fees, repayment timing, and whether the payment will fit your next paycheck before choosing.

2 Comments

Title Loans Explained: What You Need to Know Before You Apply - Look Up Loans · May 29, 2026 at 8:03 pm

[…] Payday Alternative Loan, or PAL, is a small-dollar loan offered by some federal credit unions. PALs are designed as a safer […]

Title Loan Requirements: What You Need Before You Apply - Look Up Loans · May 31, 2026 at 8:05 pm

[…] federal credit unions offer Payday Alternative Loans, also called PALs. These are small-dollar loans designed to give borrowers a safer option than […]