Introduction

When money is short and a bill cannot wait, a payday loan can feel like the only move left. It is fast, easy to find, and built for urgent cash needs. But the problem is what happens after you borrow, especially if the repayment leaves you short again on your next paycheck.

Before you go that route, it is worth looking at payday loan alternatives that may cost less, give you more time, or help you avoid borrowing altogether. Some involve credit unions or small-dollar loans. Others involve payment plans, bill extensions, employer advances, or local support.

The best choice depends on how much money you need, how quickly you need it, and whether the repayment will fit your budget. This guide explains which Payday Loan Alternatives to consider first, how each one works, and what to avoid before you borrow.

Key Takeaways

- Payday loans may be fast, but the repayment can put pressure on your next paycheck.

- The best payday loan alternative depends on how much you need, how fast you need it, and what repayment will do to your budget.

- Some alternatives help you avoid borrowing, such as bill extensions, payment plans, local assistance, or employer support.

- Credit unions may offer small-dollar loans or Payday Alternative Loans with clearer repayment terms than many payday loans.

- Cash advance apps and paycheck advances can help with small gaps, but they still need a repayment plan.

- Before choosing any option, compare the fees, timing, total cost, and what happens if you cannot pay on time.

- If you need short-term cash every month, a loan may only cover the symptom. You may need a bigger fix, such as bill negotiation, budgeting help, or local support.

Disclaimer: This site contains affiliate links. If you make a purchase, we may earn a commission at no extra cost to you.

Why Payday Loans Can Create a Bigger Problem

A payday loan can feel helpful because it solves the first problem fast: you need cash, and the lender can provide it quickly. The harder part is what happens when repayment is due.

Many payday loans are built for short-term repayment. That can create pressure if the full payment, fees, and your regular bills all hit around the same time.

For example, you may borrow money to cover a utility bill today. But when the loan payment comes due, your next paycheck may also need to cover rent, groceries, gas, insurance, and other expenses.

That is where the cycle can start. If the repayment leaves you short again, you may feel forced to borrow again just to cover normal bills.

The risk is not only the cost of one loan. The bigger risk is repeat borrowing.

This is why it helps to look at safer alternatives first. A better option should give you at least one of these advantages:

- More time to repay

- Lower fees or interest

- A smaller hit to your next paycheck

- A payment plan instead of one large payment

- A way to solve the bill without borrowing at all

The goal is not just to get through today. The goal is to get through today without making the next payday harder.

How to Choose the Best Alternative for Your Situation

The best payday loan alternative depends on the problem you are trying to solve. A rent shortfall, a utility shutoff notice, a car repair, and a grocery gap may all need different answers.

Start with the option that solves the problem with the least cost and the least risk. If you can avoid borrowing, start there. If you do need to borrow, choose the option with clear terms and a payment you can handle.

Ask yourself these questions before choosing:

- How much money do I need?

- How fast do I need it?

- Can I solve this without borrowing?

- Can I ask for more time to pay?

- What fees or interest will I pay?

- When is repayment due?

- Will this leave me short again next payday?

If the problem is a bill, call the company first. A payment plan or extension may be cheaper than any loan.

If the problem is a small cash gap, an employer advance, earned wage access option, or cash advance app may help, as long as the repayment will not hurt your next paycheck.

If the problem is larger or needs more structure, a credit union loan, Payday Alternative Loan, or personal loan may make more sense.

The safest choice is the one that gives you enough help without creating another emergency. Before you agree to anything, make sure the repayment fits your real budget, not just your best-case paycheck.

Safer Payday Loan Alternatives to Consider First

Before you use a payday loan, look for an option that either lowers the cost, gives you more time, or helps you avoid borrowing completely. The best place to start is usually the option tied to the actual problem.

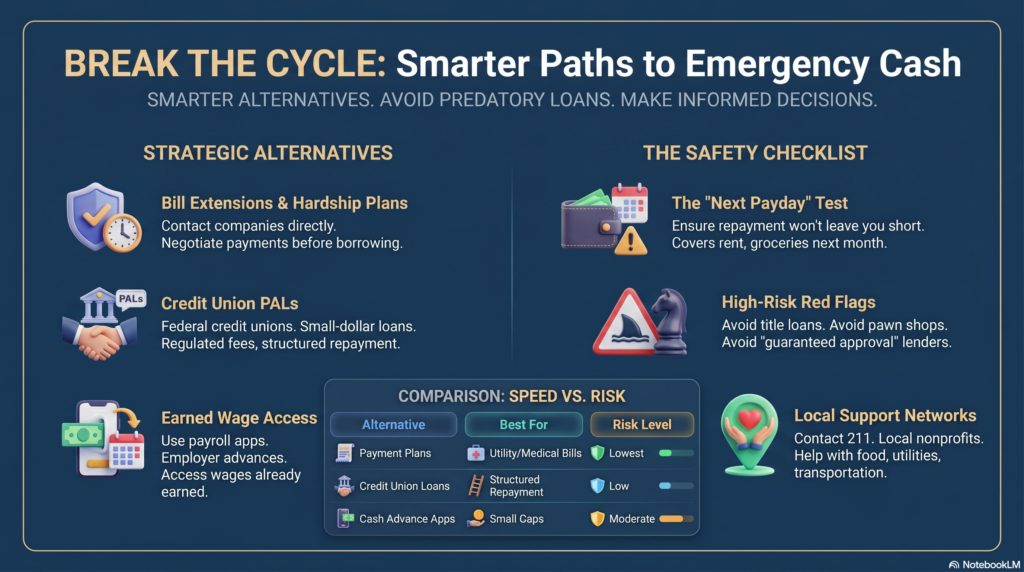

Bill Extensions and Payment Plans

If the cash shortage is tied to a bill, contact the company before you borrow. Utility companies, medical offices, landlords, phone providers, and service companies may offer extensions, partial payments, or hardship plans.

- Best for: Utility bills, medical bills, rent issues, or service payments

- Why it helps: You may solve the problem without taking out a loan

- Watch for: Late fees, service shutoff dates, or written agreement details

Ask for the new due date, the payment amount, and whether any fees will be added.

Credit Union Small-Dollar Loans

Credit unions may offer small personal loans or emergency loans with clearer repayment terms than payday loans. These can be useful if you need more structure and can wait long enough to apply.

- Best for: Borrowers who already belong to a credit union

- Why it helps: You may get a fixed payment and a clear payoff date

- Watch for: Membership rules, approval time, and application requirements

If you are not already a member, ask whether you can join and apply for a small-dollar loan.

Payday Alternative Loans

Payday Alternative Loans, or PALs, are small-dollar loans offered by some federal credit unions. They are designed as a safer alternative to traditional payday loans.

- Best for: Credit union members who need a small short-term loan

- Why it helps: PALs have rules around loan amounts, fees, and repayment terms

- Watch for: Availability, membership requirements, and whether the credit union offers PAL I or PAL II

A PAL can be a strong option when you need short-term cash but want a more structured repayment plan.

Employer Advances or Earned Wage Access

Some employers let workers access part of their earned wages before payday. This may come through payroll, HR, or an earned wage access app connected to your employer.

- Best for: A small gap before your next paycheck

- Why it helps: You may be using wages you already earned instead of taking a new loan

- Watch for: Fees, transfer costs, and a smaller next paycheck

This can help with a short gap, but it still needs a plan. If the advance leaves your next paycheck too small, the problem may repeat.

Local Assistance Programs

Local nonprofits, churches, community groups, and government programs may help with food, rent, utilities, transportation, or medical needs. These programs may not cover everything, but even partial help can reduce how much you need to borrow.

- Best for: Basic needs and emergency bills

- Why it helps: You may avoid debt or borrow less

- Watch for: Eligibility rules, limited funds, and processing time

This option works best when you ask early, before the bill becomes urgent.

Borrowing From Friends or Family

Borrowing from someone you trust can cost less than a payday loan, but it needs clear terms. A casual promise can turn awkward fast if repayment is unclear.

- Best for: Small amounts and short repayment timelines

- Why it helps: You may avoid interest, fees, and lender pressure

- Watch for: Relationship stress if expectations are not clear

Put the amount, repayment date, and payment method in writing. Simple is fine. Clear is the goal.

Cash Advance Apps

Cash advance apps can help with a small cash gap before payday. They may be faster than a loan, but they are not free if fees, tips, subscriptions, or instant-transfer costs apply.

- Best for: Small short-term gaps

- Why it helps: You may get quick access to a small amount

- Watch for: Fees, repeat use, and repayment timing

A cash advance app can help once in a while. It becomes risky if you need it every paycheck.

Personal Loans

A personal loan may make sense if the expense is larger and you need more time to repay. This option is usually better for bigger costs than a quick payday gap.

- Best for: Larger expenses that need structured repayment

- Why it helps: You may get fixed payments and a clear payoff date

- Watch for: APR, origination fees, long terms, and total repayment cost

Before applying, check whether the lender offers prequalification so you can compare possible terms first.

Credit Card Options

A credit card may help if you already have available credit and can pay the balance down quickly. It can also be useful if you qualify for a promotional APR offer.

- Best for: Short-term expenses you can repay quickly

- Why it helps: You may avoid a separate loan application

- Watch for: Cash advance fees, high interest, and balances that linger

A credit card is only a safer option if you have a realistic payoff plan. Otherwise, the balance can become another monthly burden.

Payday Loan Alternatives Compared by Speed, Cost, and Risk

Each payday loan alternative solves a different problem. Some are fast but can shrink your next paycheck. Others take more time but may cost less or help you avoid debt altogether.

Use this comparison to narrow your choices before you borrow.

| Alternative | Best For | Typical Speed | Main Cost Risk | Best First Step |

|---|---|---|---|---|

| Bill extension or payment plan | Bills you cannot pay on time | Same day to a few days | Late fees or missed agreement terms | Call the company and ask what hardship options are available |

| Credit union small-dollar loan | Borrowers who want structured repayment | A few days, depending on the credit union | Application requirements or interest costs | Ask your credit union about small-dollar or emergency loans |

| Payday Alternative Loan | Federal credit union members who need short-term cash | Depends on membership and approval | Availability and repayment fit | Ask whether the credit union offers PAL I or PAL II |

| Employer advance or earned wage access | Small gaps before payday | Same day to a few days | Smaller next paycheck or access fees | Ask payroll or HR what options are available |

| Local assistance program | Rent, utilities, food, transportation, or medical needs | Varies by program | Limited funds or eligibility rules | Contact local nonprofits, community agencies, or 211 |

| Friends or family loan | Small amounts with flexible repayment | Often fast | Relationship strain if terms are unclear | Agree on the amount and repayment date in writing |

| Cash advance app | Small cash gaps | Often fast | Fees, tips, subscriptions, or repeat use | Check the total cost and repayment date before accepting |

| Personal loan | Larger expenses that need more time | Same day to several days | APR, fees, and long repayment terms | Prequalify and compare offers before applying |

| Credit card | Short-term costs you can repay quickly | Immediate if available | High interest or cash advance fees | Check your APR, fees, and payoff plan first |

The safest option is usually the one that solves the problem with the least damage to your next paycheck. A bill extension or local assistance program may be better than borrowing if it handles the immediate need.

If you do need to borrow, compare the full cost before choosing. Look at the fee, APR, repayment date, and whether the payment will leave you short again.

Speed matters in an emergency, but speed should not be the only reason you choose an option. A slower option with clearer terms may protect your budget better than fast cash with a painful repayment date.

Options to Be Careful With Before You Borrow

Some fast-cash options can help in an emergency, but they can also make the next few weeks harder. Before you borrow, look at the full cost, the repayment date, and what happens if you cannot pay on time.

The problem is not always the loan itself. The problem is choosing an option that gives you money today but leaves you with a bigger bill tomorrow.

Title Loans

A title loan uses your vehicle title as collateral. That means the lender may be able to take your car if you do not repay the loan.

This can be risky if you need your car for work, school, childcare, or daily life. Losing the vehicle could create a much bigger problem than the original cash shortage.

Pawn Loans

A pawn loan uses something you own as collateral, such as jewelry, electronics, or tools. If you do not repay the loan, the pawn shop can keep the item.

This may be better than some high-cost loans because it usually does not involve your credit. But it can still be expensive, and you may lose something important if you cannot repay on time.

Overdrafts

An overdraft may cover a payment when your account is short, but it can come with fees. If more charges hit before your next deposit, the fees can stack up quickly.

This is risky when your account is already tight. One overdraft can turn into several fees before you realize how much it costs.

High-Fee Cash Advances

Some cash advances look small at first, but fees, tips, subscriptions, or instant-transfer charges can raise the real cost.

Before using one, check how much you will receive, how much you will repay, and when the money will come out of your account.

Guaranteed Approval Loans

Be careful with any lender that promises approval without checking your income, identity, or ability to repay.

Fast approval can be normal. Guaranteed approval can be a warning sign, especially if the lender hides the APR, charges upfront fees, or pushes you to sign quickly.

Repeat Borrowing

The biggest warning sign is needing short-term loans again and again. If you borrow every payday, the loan may no longer be solving the problem. It may be keeping the cycle going.

If that is happening, look for help that deals with the larger issue, such as bill negotiation, a payment plan, local assistance, or nonprofit credit counseling.

The safest choice is the one that helps today without making your next paycheck harder to manage. If the cost is unclear, the payment feels tight, or the lender rushes you, pause before borrowing.

When You May Need Help Beyond a Loan

A payday loan alternative can help with a one-time problem. But if you need fast cash every month, the issue may be bigger than one bill or one missed paycheck.

That does not mean you failed. It usually means your income, bills, debt payments, or payment dates are not lining up in a way that works.

A loan may help for a few days, but it will not fix a regular budget gap. If the same shortage keeps coming back, it may be time to look for support that reduces the pressure instead of adding another payment.

You may need help beyond a loan if:

- You borrow money before nearly every payday.

- You cannot cover basic bills without using credit or advances.

- You are choosing between rent, food, utilities, gas, or medicine.

- You are behind on several bills at once.

- You are using one loan to pay another loan.

- You do not know how much money will be left after your bills are paid.

In that situation, start with the bill that creates the biggest risk. That might be housing, utilities, transportation, food, or medical care.

Then look for support tied to that specific need. A utility company may offer a hardship plan. A landlord may agree to a written payment arrangement. A local nonprofit may help with food, rent, transportation, or emergency bills. A nonprofit credit counselor may help you review debt payments and build a plan.

The goal is to reduce the shortage, not cover it with another short-term loan. Sometimes the safest payday loan alternative is not a loan at all.

Common Mistakes to Avoid When Comparing Payday Loan Alternatives

Choosing a payday loan alternative is not just about finding money fast. It is about choosing the option that creates the least stress after the money arrives.

The wrong choice can still leave you short, even if it is not technically a payday loan.

Choosing the Fastest Option Without Checking the Cost

Fast money can feel like relief, but speed does not tell you whether the option is affordable.

Before you accept anything, check the full cost. Look at fees, interest, transfer charges, late fees, and when repayment is due.

Ignoring the Next Paycheck

Some options solve today’s problem by taking money from your next paycheck. That can work once, but only if your next paycheck can still cover regular bills.

Before using a paycheck advance, cash advance app, or short-term loan, ask yourself one question: “Will I be short again when this gets repaid?”

Borrowing More Than You Need

Extra cash can feel helpful, but it can also make repayment harder.

Start with the exact amount needed to solve the urgent problem. If the bill is $300, borrowing $600 may create a larger payment than your budget can handle.

Missing Non-Loan Options

A loan is not always the first move. If the problem is a bill, ask for an extension or payment plan before borrowing.

If the problem is food, utilities, rent, transportation, or medical care, local assistance may help reduce the amount you need.

Assuming Every Credit Union Offers the Same Loans

Credit unions can be helpful, but their loan options vary. Some offer Payday Alternative Loans, some offer other small-dollar loans, and some may not offer either.

Ask directly what small-dollar or emergency loan options are available before you build your plan around one product.

Using Short-Term Help Again and Again

A short-term option can help with a one-time emergency. It becomes risky when it turns into a monthly routine.

If you keep needing cash before payday, the better next step may be bill negotiation, budgeting support, local assistance, or nonprofit credit counseling.

The best payday loan alternative should help you get through the problem without making the next paycheck harder to manage. If the option gives you money today but creates another emergency tomorrow, keep looking.

A Simple Example of Choosing a Payday Loan Alternative

Imagine James needs $400 to keep his phone and utility bill from falling behind. Payday is six days away, and a payday loan looks easy because he can apply quickly.

Before borrowing, James checks the bill first. The utility company offers a short extension with a smaller payment due now and the rest due later. That lowers the amount he needs today.

Next, he looks at his paycheck. If he borrows the full $400 and has to repay it right away, his next check may not cover groceries, gas, and rent. That means he could end up needing another loan.

Instead, James chooses a smaller solution:

- He sets up a payment plan for the utility bill.

- He uses a small employer advance to cover the phone bill.

- He avoids borrowing more than he needs.

- He checks that his next paycheck can still cover regular bills.

This works because he matched the solution to the problem. He did not just grab the fastest cash available. He reduced the bill first, borrowed less, and made sure repayment would not leave him short again.

That is the goal with payday loan alternatives. The best option is the one that solves the immediate problem without creating another one on your next payday.

Conclusion

Payday loan alternatives work best when they solve the urgent problem without making your next paycheck harder to manage. The goal is not just to get cash quickly. The goal is to choose the option with the lowest cost, clearest terms, and safest repayment path.

Start with non-loan options when you can. A bill extension, payment plan, employer support, or local assistance program may reduce the amount you need or help you avoid borrowing altogether.

If you do need to borrow, compare credit union loans, Payday Alternative Loans, personal loans, cash advance apps, and credit card options carefully. Look at the fees, repayment date, total cost, and whether the payment will still fit after your regular bills are covered.

A payday loan may feel like the fastest answer, but fast does not always mean safe. Before you borrow, pause long enough to check your alternatives. A better choice today can help you avoid a bigger money problem tomorrow.

Frequently Asked Questions About Payday Loan Alternatives

What is the best alternative to a payday loan?

The best alternative depends on why you need the money. If the problem is a bill, start by asking for an extension or payment plan. If you need a small loan, check with a credit union before using a payday lender.

What can I do if I need money before payday?

You may be able to use an employer advance, earned wage access, a cash advance app, a credit union loan, or help from a local assistance program. Before choosing, check the fees and make sure repayment will not leave you short again.

Are Payday Alternative Loans better than payday loans?

Payday Alternative Loans can be a safer option because they come from participating federal credit unions and follow specific rules. They may offer clearer repayment terms than many payday loans, but you still need to qualify and make sure the payment fits your budget.

Can I get a payday loan alternative with bad credit?

Yes, some alternatives may still be available with bad credit. Credit unions, payment plans, local assistance programs, employer advances, and borrowing from someone you trust may not depend only on your credit score.

Do credit unions offer payday loan alternatives?

Some credit unions offer small-dollar loans, emergency loans, or Payday Alternative Loans. Not every credit union offers the same products, so ask directly what short-term loan options are available.

Are cash advance apps safer than payday loans?

Cash advance apps may be safer for small gaps, but they still need caution. Fees, tips, subscriptions, and fast-transfer charges can add up, and repayment may reduce your next paycheck.

What if I cannot repay a payday loan?

Contact the lender as soon as possible and ask about repayment options. You can also consider help from a nonprofit credit counselor, local legal aid organization, or state consumer protection office if you feel trapped or pressured.

What should I avoid when looking for fast cash?

Be careful with guaranteed approval loans, unclear fees, title loans, high-cost cash advances, and any lender that pressures you to sign quickly. A safer option should explain the cost, repayment date, and consequences before you agree.

0 Comments