Introduction: Understanding the Real Cost of Fast Cash

When money runs short, a title loan can look like a quick way to get cash without a traditional credit check. You use your vehicle title as collateral, and in many cases, you can keep your vehicle while the loan is active.

But that convenience comes with serious risk.

Title loans are usually short-term, high-cost loans. If you cannot repay on time, fees can grow quickly, and the lender may be able to repossess your vehicle. That can turn a temporary cash shortage into a much bigger financial problem.

Before you borrow against your vehicle, you need to understand how title loans work, what they can really cost, what happens if you fall behind, and what safer options may be available.

This guide explains the title loan process, the biggest risks to watch for, and the steps to take before signing any loan agreement.

Key Takeaways

- A title loan lets you borrow money using your vehicle title as collateral.

- You may still be able to drive your vehicle during the loan, but you can lose it if you default.

- Title loans often come with high costs, short repayment windows, and rollover risks.

- State laws vary, so title loan rules, fees, APR limits, and repossession rights depend on where you live.

- Always review the full repayment amount before signing, not just the cash you receive upfront.

- Safer alternatives, such as credit union loans, payment plans, emergency assistance, or Payday Alternative Loans, may cost less and carry less risk.

- A title loan should be treated as a last-resort option, not a first choice for fast cash.

Disclaimer: This site contains affiliate links. If you make a purchase, we may earn a commission at no extra cost to you.

What Is a Title Loan and How Does It Work?

A title loan is a short-term loan that uses a titled asset as collateral. In most cases, that asset is a vehicle, such as a car, truck, motorcycle, RV, or boat, depending on the lender and state rules.

A car title loan is the most common type of title loan. With this option, you borrow money using your car title as collateral. In many cases, you can keep driving the vehicle while the loan is active, but the lender may place a lien on the title until the loan is repaid.

The basic structure is similar across title loans: the lender offers money based partly on the value of the titled asset, your ownership status, your income, and the lender’s rules. If you repay the loan as agreed, the lien is removed or the title is released. If you do not repay, the lender may be able to repossess or claim the asset.

Common title loan examples include:

- Car title loans, backed by a car title

- Truck title loans, backed by a pickup or commercial-style truck title

- Motorcycle title loans, backed by a motorcycle title

- RV title loans, backed by a recreational vehicle title

- Boat title loans, where accepted by the lender and allowed by state law

- Title pawns, which are title-backed transactions used in some states

Most title loans are designed for fast approval. Instead of focusing mainly on your credit score, lenders usually look at the titled asset, proof of ownership, income, and ability to repay.

That speed is what makes title loans appealing, but it is also what makes them risky. Repayment windows can be short, costs can be high, and rollovers can make the debt grow quickly.

A title loan is not just quick cash. It is a loan tied directly to an asset you may rely on for transportation, work, family responsibilities, or daily life. Before you sign, make sure you understand the full repayment amount, due date, fees, rollover rules, and what happens if you cannot pay on time.

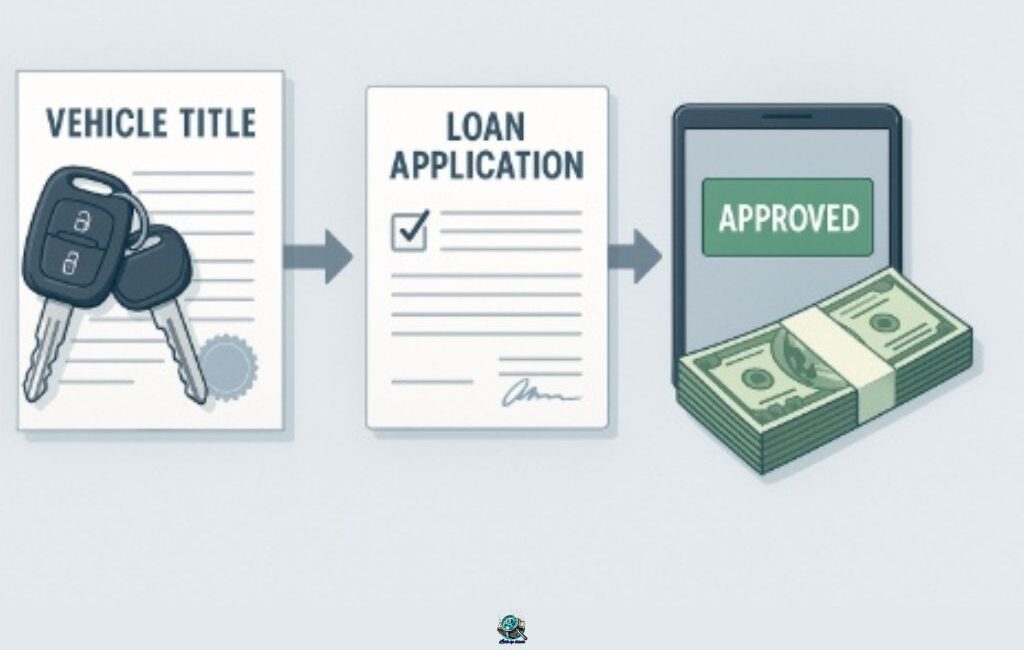

The Title Loan Process Step by Step

Getting a title loan is usually fast, but each step comes with details you should review carefully. Speed can be helpful in an emergency, but it should never replace caution.

Here is how the process usually works.

1. You Apply Online or In Person

You start by submitting basic personal information, vehicle details, and proof that you own the vehicle.

Some lenders advertise fast approval with minimal paperwork. That may sound convenient, but you should still confirm that the lender is licensed in your state before sharing personal information.

2. The Lender Reviews Your Vehicle

The lender estimates your vehicle’s value based on factors like make, model, year, mileage, condition, and market demand.

Some lenders inspect the vehicle in person. Others use photos or online valuation tools. Either way, remember that the lender’s offer is not the same as your car’s full value.

3. You Receive a Loan Offer

The lender gives you a loan amount, repayment terms, fees, and interest rate.

This is the step where you need to slow down. Review the annual percentage rate, finance charge, due date, rollover terms, late fees, and repossession rules before signing anything.

4. You Sign the Agreement

If you accept the offer, you sign the loan agreement. The lender may keep your physical title or place a lien on the vehicle title until the loan is repaid.

Do not sign if the repayment amount, fees, or default terms are unclear. Ask questions before you agree, not after the loan is active.

5. You Receive the Funds

After the paperwork is complete, the lender gives you the money. Depending on the lender, this may happen by cash, check, prepaid card, or direct deposit.

Same-day funding can be useful, but it can also make the decision feel rushed. Make sure the loan solves the problem without creating a larger one.

6. You Repay, Renew, or Risk Default

Most title loans have short repayment timelines. If you cannot repay on time, the lender may offer to renew or roll over the loan.

A rollover may delay the due date, but it often adds more fees and keeps the original debt alive. If you continue falling behind, the lender may be able to repossess your vehicle.

Bottom Line

The title loan process is simple on the surface: apply, offer, sign, get funds, repay. The real risk is in the terms.

Before moving forward, make sure you know the total repayment amount, the due date, the lender’s rollover policy, and exactly what happens if you cannot pay.

Are Title Loans Legal in the U.S.?

Title loans are legal in some states, restricted in others, and effectively unavailable in places with strict interest-rate caps or consumer lending rules.

That is why you should never assume a title loan is legal, affordable, or properly licensed just because a lender advertises online. State laws can affect loan amounts, APR limits, repayment terms, licensing rules, repossession rights, and whether title lenders can operate at all.

Before applying, check your state’s official financial regulator, attorney general, or consumer protection agency. This matters even more with online lenders, since some may advertise across state lines while still being subject to your local laws.

Federal law requires lenders to provide written disclosures about finance charges and the annual percentage rate before you sign a credit agreement, according to the Federal Trade Commission. That disclosure helps you compare the true cost of borrowing, but it does not automatically make a title loan affordable or safe.

Some states have very specific rules. For example, the California Department of Financial Protection and Innovation says interest charges are capped on automobile title loans under $10,000 made under a California Financing Law license, while current state law does not limit rates for loans of $10,000 or more.

Because the rules vary so much, treat state-law information as a starting point, not a final answer. Verify the current law in your state before submitting personal information or signing any title loan agreement.

Safer Rule of Thumb

If you cannot clearly confirm that the lender is licensed in your state, the APR is disclosed, the repayment terms are affordable, and the repossession rules are clear, do not move forward.

How Much Can You Borrow With a Title Loan?

The amount you can borrow with a title loan usually depends on your vehicle’s value, your equity in the vehicle, your income, and the lender’s rules.

According to the Federal Trade Commission, title loans are often for 25% to 50% of the vehicle’s value. That means a car worth $8,000 may lead to a much smaller loan offer, not an $8,000 loan.

Several factors can affect the offer:

- The vehicle’s make, model, and year

- Mileage and overall condition

- Whether the title is clear

- Local market value

- State lending rules

- Your income or ability to repay

- The lender’s internal limits

A higher offer is not always better. With a title loan, borrowing more can mean more interest, more fees, and a greater risk of losing your vehicle if you cannot repay on time.

Before accepting any amount, ask the lender for the full repayment total in writing. That total should include the loan amount, interest, fees, due date, rollover costs, and any charges that may apply if you pay late or default.

Bottom Line

Do not choose the largest loan just because it is available. Choose the smallest amount that solves the immediate problem, and only move forward if you have a realistic plan to repay it on time.

What You Usually Need to Qualify for a Title Loan

Title loans are often easier to qualify for than traditional loans, but approval is not automatic. Lenders still need to confirm that you own the vehicle, can prove your identity, and have some way to repay the loan.

The exact requirements vary by lender and state, but most title loan companies ask for similar information before making an offer.

Basic Title Loan Requirements

Most lenders ask for:

- A vehicle title in your name

- A valid government-issued ID

- Proof of residence

- Proof of income or regular deposits

- Vehicle registration

- Proof of insurance, if required

- Photos of the vehicle or an in-person inspection

- A spare key, in some cases

The most important requirement is usually a clear title. That means the vehicle is paid off and does not have another lender or lienholder listed on the title. Some lenders may consider vehicles with existing liens, but those loans can be more complicated and may come with extra costs.

How Credit and Income Affect Approval

Title loans are often marketed to borrowers with bad credit because approval depends heavily on the vehicle used as collateral. Instead of focusing only on a credit score, many lenders look at the title, the vehicle’s value, and whether the borrower has a way to repay.

That does not mean credit never matters. Some lenders may still check credit, even if they do not weigh it as heavily as a traditional lender would. Others may advertise no-credit-check title loans, but they still usually review the title, vehicle value, identity documents, and repayment ability.

Income can also come from different sources, depending on the lender. A borrower may use wages, self-employment income, retirement income, benefits, workers’ compensation, regular bank deposits, or other documented income. The important part is consistency. The lender wants to see that money comes in regularly enough to support repayment.

Still, qualifying for a title loan is not the same as being able to afford one. A lender may approve the loan based on your vehicle’s value, but the payment may still be too high for your budget.

Before accepting an offer, compare the full repayment amount with your actual cash flow. If paying the loan would force you to miss rent, utilities, insurance, groceries, or another essential bill, the loan is too risky.

Bottom Line

Bad credit or nontraditional income may not prevent approval, but approval alone should not be the goal. Focus on whether the loan fits your budget without putting your vehicle at risk.

What Happens If You Default on a Title Loan?

Defaulting on a title loan can create serious consequences because the loan is tied directly to your vehicle.

If you miss a payment or cannot repay the loan by the due date, the lender may charge late fees, offer a renewal or rollover, or begin the repossession process. The exact timeline depends on your loan agreement and state law.

A rollover may sound like a helpful extension, but it can make the loan much more expensive. The Federal Trade Commission warns that rolling over a car title loan often means paying new fees while still owing the original loan amount.

If the loan stays unpaid, the lender may be able to repossess your vehicle. In some situations, a lender can take a vehicle without going to court or giving advance notice, depending on state law and the loan terms. The Federal Trade Commission explains that repossession rules vary, so borrowers should understand their rights before and after a vehicle is taken.

After repossession, the lender may sell the vehicle and apply the sale proceeds to the loan balance, repossession costs, storage fees, and other charges. If the sale does not cover everything owed, you may still owe a remaining balance, depending on your state’s laws.

The risk is not rare. The Consumer Financial Protection Bureau found that one in five borrowers who took out a single-payment auto title loan had their vehicle seized after failing to repay.

Bottom Line

Defaulting on a title loan can cost more than late fees. It can put your transportation, job access, family responsibilities, and financial stability at risk.

Before signing, make sure you know the due date, total repayment amount, rollover rules, late fees, repossession terms, and what happens if the vehicle sells for less than you owe.

How to Avoid Default and Protect Your Vehicle

The best way to protect your vehicle is to avoid taking a title loan unless you have a clear, realistic repayment plan before you sign.

Because your car is collateral, missed payments can create more than a money problem. They can put your transportation at risk. That is why the goal should be simple: borrow as little as possible, understand every cost, and act early if repayment starts to look difficult.

Borrow Only What You Truly Need

Do not accept the maximum loan amount just because the lender offers it.

A larger loan usually means a larger repayment burden. If you only need enough to cover one urgent bill, borrow for that bill, not for extra cushion. Every extra dollar borrowed can increase the cost and make the loan harder to repay.

Get the Full Repayment Amount in Writing

Before signing, ask the lender to show the total repayment amount in writing.

That amount should include:

- The loan principal

- Interest

- Fees

- Due date

- Late fees

- Rollover or renewal costs

- Repossession-related charges, if listed in the agreement

Do not rely only on the amount you receive upfront. The number that matters most is what you must repay.

Avoid Rollovers When Possible

A rollover may feel like relief because it gives you more time, but it often adds fees while keeping the original loan balance alive.

If you already know you cannot repay on time, pause before agreeing to a renewal. Compare other options first, including a payment plan, help from a local nonprofit, a credit union loan, or advice from a nonprofit credit counselor.

Contact the Lender Early if Trouble Starts

If you think you may miss a payment, contact the lender before the due date.

Some lenders may offer an extension, payment arrangement, or other option. That does not make the loan safe, but early communication may give you more choices than waiting until the account is already in default.

Get Help Before Repossession Becomes Likely

If you are at risk of losing your vehicle, consider contacting a nonprofit credit counselor, legal aid office, or local consumer protection agency.

This is especially important if you believe the lender is not licensed, the terms were unclear, or the repossession process seems unfair. Your rights can vary by state, so local help matters.

Bottom Line

A title loan is easiest to control before you sign. Once the loan is active, missed payments, rollovers, and repossession risk can move quickly.

Protect your vehicle by borrowing the smallest amount possible, getting every cost in writing, avoiding rollovers when you can, and asking for help before the situation gets worse.

Online vs. In-Person Title Loans

Title loans can be offered online, in person, or through a mix of both. The basic loan structure is usually similar, but the application experience can feel very different.

Online title loans may move faster because you can upload documents, submit vehicle photos, and receive an offer without visiting a store. That convenience can help in an emergency, but it also makes it easier to rush into a loan before checking the lender’s license, fees, and repayment terms.

In-person title loans may give you more direct support. You can ask questions, review paperwork with a representative, and have the vehicle inspected on-site. The downside is that some borrowers may feel more pressure to sign quickly when they are sitting across from a lender.

| Feature | Online Title Loan | In-Person Title Loan |

|---|---|---|

| Speed | Often faster and more convenient | May take longer because of travel and inspection |

| Vehicle review | Usually based on photos or online valuation | Usually includes an on-site inspection |

| Document submission | Uploaded digitally | Presented in person |

| Support | May rely on phone, email, or chat | Face-to-face questions may be easier |

| Pressure risk | Easier to pause before signing | Some borrowers may feel pressured in person |

| Safety concern | Must verify the lender is licensed | Must still review terms carefully |

No matter how you apply, do not let speed become the deciding factor. A fast application does not mean the loan is affordable, licensed, or safe.

Before submitting personal information, confirm that the lender operates legally in your state. Before signing, review the APR, finance charge, repayment deadline, rollover policy, late fees, and repossession terms.

Bottom Line

Online title loans may be convenient, and in-person title loans may feel more direct. Either way, the real decision is not where you apply. It is whether the loan terms are clear, legal, and affordable enough to avoid putting your vehicle at risk.

How to Avoid Borrowing More Than You Need

Because a title loan uses your vehicle as collateral, the goal should not be to borrow the largest amount possible. The goal should be to borrow the smallest amount that solves the immediate problem, only if you are confident you can repay it on time.

A larger loan may feel helpful at first, but it also creates a larger repayment burden. With title loans, that can mean more interest, more fees, and a higher risk of losing your vehicle if you fall behind.

Know Your Vehicle’s Value Before You Apply

Check your vehicle’s estimated value before speaking with a lender. You can use vehicle pricing tools or compare similar cars for sale in your area.

This helps you understand whether the lender’s offer is reasonable. It also helps you avoid being pressured into a larger loan than you planned to take.

Borrow Based on the Emergency, Not the Offer

A lender may approve you for more than you need. That does not mean you should take the full amount.

For example, if you need $700 to cover an urgent bill, borrowing $1,500 may create a bigger problem later. Title loans are expensive, and every extra dollar borrowed can increase the cost of repayment.

Ask for the Total Repayment Amount

Before signing, ask the lender to show the full repayment amount in writing. This should include the loan principal, interest, fees, due date, rollover costs, and any other charges that may apply if you pay late or default.

Do not rely only on the payment amount. A loan can look manageable in pieces while still being very expensive overall.

Compare the Loan to Safer Options

Before using your car title, compare the loan against safer options, such as a credit union loan, a payment plan, a Payday Alternative Loan, local emergency assistance, or help from someone you trust.

Even if those options take longer, they may protect you from the risk of repossession.

Keep Your Vehicle Risk in Mind

Your car may be worth far more than the amount you borrow. If you default, you could lose access to transportation, work, childcare, medical appointments, and other essentials.

That is why you should treat a title loan as a last-resort option, not a way to unlock the full value of your car.

Bottom Line

Do not use your vehicle’s value as a reason to borrow more. Use it as a reminder of what is at stake.

A smaller loan, a clear repayment plan, and a safer alternative can protect you from turning a short-term cash problem into a long-term financial setback.

What to Consider Before Taking a Title Loan

Before you sign a title loan agreement, pause and look at the full picture. The loan may solve an immediate cash problem, but it can also create a larger problem if the repayment terms do not fit your budget.

Use these questions as a final check before moving forward.

| Question to Ask | Why It Matters |

|---|---|

| Can I repay the full amount on time? | If not, you may face late fees, rollovers, default, or repossession. |

| Do I know the total repayment amount? | The cash you receive is only one part of the loan. You need to know the principal, interest, fees, and due date. |

| Have I checked the APR and finance charge? | These numbers show the real cost of borrowing and help you compare options. |

| Is the lender licensed in my state? | An online ad does not prove the lender is operating legally where you live. |

| Do I understand the rollover rules? | Renewing the loan can add fees and keep the original balance alive. |

| Have I compared safer alternatives? | A credit union loan, payment plan, assistance program, or Payday Alternative Loan may cost less and carry less risk. |

| Do I understand the repossession terms? | If you default, the lender may be able to take and sell your vehicle, depending on state law. |

| Am I borrowing only what I truly need? | Taking more than necessary can increase the repayment burden and risk. |

If any answer makes you uncomfortable, slow down before signing. A title loan should never depend on hope, pressure, or vague promises.

You should know exactly how much you owe, when it is due, what happens if you cannot pay, and what other options you have checked first.

Bottom Line

A title loan is not just a quick application. It is a financial decision tied to your vehicle.

Before borrowing, make sure the loan is legal, affordable, clearly explained, and truly necessary. If you cannot confirm those things, it is safer to keep looking for another option.

Safer Alternatives to Title Loans

If you need emergency cash, a title loan may feel like the fastest option. But fast does not always mean safe.

Before using your vehicle as collateral, compare lower-risk options. Some may take longer, but they can help you avoid high fees, rollovers, and the possibility of repossession.

| Alternative | Why It May Be Safer | What to Watch For |

|---|---|---|

| Credit union personal loan | Often has lower rates than title loans and does not require your car title as collateral | You may need membership, income verification, or a credit check |

| Payday Alternative Loan | Federal credit unions offer PALs with a maximum interest rate of 28%, according to the National Credit Union Administration | You must apply through a participating federal credit union |

| Payment plan with a creditor | May help you solve the original bill without taking on a high-cost loan | You need to contact the creditor before the account gets worse |

| Emergency assistance program | Local nonprofits, churches, or government programs may help with rent, utilities, food, or medical needs | Availability depends on your location and situation |

| Borrowing from family or friends | May avoid interest and lender fees | Put the terms in writing to prevent misunderstandings |

| Cash advance app | May provide small short-term cash without using your car as collateral | Fees, tips, subscription costs, and repayment timing can still create problems |

| Nonprofit credit counseling | Can help you review options and make a repayment plan | Use a reputable nonprofit agency, not a debt relief company making big promises |

Credit Union Personal Loans

Credit unions and community banks may offer small personal loans at lower rates than title lenders. Even if your credit is not perfect, they may consider your income, membership history, and overall ability to repay.

This option may take more time than a title loan, but it can protect your vehicle and reduce the chance of getting trapped in expensive short-term debt.

Payday Alternative Loans

A Payday Alternative Loan, or PAL, is a small-dollar loan offered by some federal credit unions. PALs are designed as a safer alternative to payday loans and other high-cost emergency loans.

The National Credit Union Administration says PALs have a maximum interest rate of 28%, and they must follow specific federal credit union rules.

Payment Plans and Emergency Assistance

If the emergency comes from a bill, contact the company you owe before taking out a title loan. Utility companies, medical providers, landlords, and other creditors may offer payment arrangements or hardship options.

Local nonprofits, churches, and government programs may also help with rent, utilities, food, medical bills, or transportation needs. These options may not be instant, but they can keep you from risking your car.

Borrowing From Family or Friends

Borrowing from someone you trust can be uncomfortable, but it may cost far less than a title loan.

If you go this route, write down the amount, repayment date, and any agreed terms. Clear expectations protect the relationship and help both sides avoid confusion.

Cash Advance Apps

Cash advance apps may help with small short-term gaps, but they are not free money. Some charge subscription fees, express funding fees, optional tips, or repayment withdrawals that can strain your next paycheck.

Use them carefully and compare the total cost before choosing this option.

Bottom Line

Before taking a title loan, compare every safer option you can. A slower solution that protects your vehicle is often better than fast cash that could put your transportation at risk.

Disclosures and Further Resources

This guide is for informational purposes only and does not provide financial or legal advice. Title loan laws, fees, APRs, repayment terms, rollover rules, and repossession rights vary by state and lender.

Before applying for a title loan, confirm that the lender is licensed in your state. Review the full loan agreement carefully, including the finance charge, APR, fees, due date, rollover terms, late-payment rules, and repossession terms.

For general consumer guidance, you can review title loan information from the Federal Trade Commission and the Consumer Financial Protection Bureau. You can also check your state financial regulator or attorney general’s office for local rules.

If you are already behind on payments or worried about losing your vehicle, consider contacting a nonprofit credit counselor, legal aid organization, or local consumer protection office before agreeing to a rollover, refinance, or new loan.

Bottom Line

Do not rely only on a lender’s advertisement or verbal explanation. Get the terms in writing, verify the lender’s license, and understand your rights before signing anything.

This replaces your current disclosure section while keeping the same purpose, but makes it more protective and specific to title loans.

Final Thoughts: Think Carefully Before You Borrow

A title loan may offer fast cash, but the risk is serious because your vehicle is on the line.

Before you borrow, make sure you understand the full cost, not just the amount you receive. Review the APR, finance charge, due date, fees, rollover terms, and repossession rules. If any part of the agreement feels unclear, pause before signing.

Also compare safer options first. A credit union loan, payment plan, emergency assistance program, or Payday Alternative Loan may take more effort, but it can help you avoid putting your car at risk.

If you decide to move forward, borrow only what you truly need and make sure you have a realistic repayment plan. A title loan should never depend on hope, pressure, or a best-case scenario.

Fast cash can feel helpful in the moment, but protecting your transportation, income, and financial stability matters more.

Bottom Line: Use a title loan only as a last resort. Know the cost, know the risk, and do not sign until you are confident you can repay the loan without losing your vehicle.

Frequently Asked Questions About Title Loans

Can I get a title loan if my car is not fully paid off?

Usually, you need a clear vehicle title to qualify for a title loan. A clear title means the vehicle is in your name and does not have another lender or lienholder attached to it.

Some lenders may advertise options for vehicles with existing liens, but those loans can be more complicated and may carry extra costs. Read the terms carefully before moving forward.

How fast can I get cash from a title loan?

Some title loans can be funded the same day or within one business day, depending on the lender, your documents, and how quickly the vehicle is evaluated.

Fast funding should not be the only reason you choose a lender. Always review the APR, finance charge, fees, due date, and repossession terms before signing.

Will a title loan affect my credit score?

It depends on the lender. Some title lenders do not report regular payments to the major credit bureaus, so paying on time may not help your credit the way a traditional loan might.

However, if you default and the account goes to collections, it could hurt your credit. Ask the lender how payments, defaults, and collections are reported before you borrow.

What happens if I cannot repay my title loan?

If you cannot repay on time, the lender may charge late fees, offer a rollover, or begin the repossession process. A rollover may give you more time, but it can also add new fees while leaving the original balance unpaid.

If the loan remains unpaid, the lender may be able to repossess and sell your vehicle, depending on your state’s laws and the loan agreement.

Are online title loans safe?

Some online title lenders are legitimate, but others may be risky or unlicensed. Never assume an online lender is legal in your state just because the website accepts applications.

Before submitting personal information, verify the lender’s license, read reviews carefully, and check your state financial regulator or attorney general’s office.

Can I refinance a title loan to avoid repossession?

Sometimes, but refinancing is not always a real solution. It may lower the immediate payment, but it can also extend the debt and add more fees.

Only consider refinancing if it clearly lowers your total cost or gives you a realistic path to repay the loan. Do not refinance just to delay default without a plan.

Do I need car insurance for a title loan?

Many title lenders require proof of insurance before approving the loan. Some may also require you to keep insurance active while the loan is open.

If your insurance lapses, the lender may treat it as a loan agreement violation. Check the insurance rules before signing.

Do I lose equity in my vehicle when I take out a title loan?

You do not automatically lose vehicle equity when you take out a title loan, but you do put that equity at risk.

If you default and the lender repossesses your car, the vehicle may be sold to cover the loan balance, fees, storage costs, and repossession costs. Depending on the sale amount and state law, you may lose access to the vehicle’s remaining value.

Are title loans better than payday loans?

Not always. Both can be expensive, short-term borrowing options. The biggest difference is that a title loan is secured by your vehicle, which means you could lose your car if you default.

Before choosing either option, compare safer alternatives like a credit union loan, Payday Alternative Loan, payment plan, or emergency assistance program.

What is the safest way to use a title loan?

The safest approach is to avoid a title loan unless you have no better option and a clear repayment plan.

If you do move forward, borrow the smallest amount you need, get the full repayment amount in writing, avoid rollovers if possible, and make sure you understand exactly when the lender can repossess your vehicle.

3 Comments

Emergency Car Title Loans: Fast Cash or a Dangerous Trap? - Look Up Loans · April 18, 2025 at 3:40 pm

[…] you’re not sure what a title loan really is, start here before diving into emergency […]

Personal Loans: Read This Before You Sign Anything - Look Up Loans · October 9, 2025 at 1:08 pm

[…] Title loans let you borrow against your car and lose it in a single missed payment. These are not emergency options. They are debt accelerators, not debt solutions. […]

Car Title Loans Can Cost More Than You Think - Look Up Loans · May 31, 2026 at 11:39 am

[…] A car title loan is one type of title-backed borrowing. To understand the broader category, including how title loans work, what they cost, and when they may be risky, read our full guide to title loans. […]