Introduction

A personal loan can look affordable at first glance, especially when the monthly payment seems manageable.

But the real cost of the loan depends on more than the payment. The APR shows how much borrowing will cost each year once interest and certain loan fees are factored in.

This guide explains what personal loan APR means, how it differs from the interest rate, how it affects your total repayment cost, and how to compare loan offers without being misled by low advertised rates or smaller monthly payments.

Key Takeaways

- APR shows the broader cost of a personal loan. It includes the interest rate and certain required loan costs, which makes it more useful than the interest rate alone.

- APR and interest rate are not the same thing. The interest rate shows the cost of borrowing the money, while APR gives a fuller view of the yearly cost of the loan.

- A higher APR increases what you pay back. Even a few percentage points can raise your monthly payment and total interest, especially on larger loans or longer terms.

- A lower monthly payment can still cost more. Stretching repayment over more years may reduce the monthly bill but increase the total amount paid.

- Fees can change the real value of the loan. Origination fees may reduce the amount you receive while still requiring you to repay the full borrowed amount.

- Advertised rates are not guaranteed. The lowest rates usually go to borrowers with stronger credit, stable income, and lower debt levels.

- The best comparison looks at the full loan offer. APR, fees, term length, monthly payment, amount received, and total repayment should all be reviewed together.

Disclaimer: This site contains affiliate links. If you make a purchase, we may earn a commission at no extra cost to you.

APR Is the Number That Shows the Real Cost of a Personal Loan

APR stands for annual percentage rate. It shows the yearly cost of borrowing money, expressed as a percentage.

For a personal loan, APR is usually more useful than the interest rate alone because it can include both the interest charged on the loan and certain required lender fees. That broader view helps you compare loan offers more fairly, especially when one lender has a lower interest rate but higher upfront costs. The Consumer Financial Protection Bureau explains that APR measures the interest rate plus additional lender fees, such as origination charges.

For example, two lenders may both offer a $10,000 personal loan. One may advertise a lower interest rate but charge a large origination fee, while the other may have a slightly higher interest rate with no upfront fee. Looking only at the interest rate could make the first loan seem cheaper. Looking at APR helps reveal which loan may cost more once required fees are included.

APR does not tell you everything by itself. You still need to compare the loan term, monthly payment, total interest, fees, and amount you actually receive. But APR is one of the best starting points because it gives you a clearer view of the loan’s real cost.

APR vs. Interest Rate: Why They Are Not the Same Thing

The interest rate is the cost of borrowing the loan amount. It tells you how much interest the lender charges before certain fees are included.

APR gives a broader view. It combines the interest rate with certain required loan costs, then expresses that cost as a yearly percentage. That is why APR is usually the better number to use when comparing personal loan offers.

Here is a simple way to think about it:

| Loan Term | What It Shows | Why It Matters |

|---|---|---|

| Interest rate | The cost of borrowing the principal | Useful, but incomplete if the loan has fees |

| APR | The yearly cost of the loan after interest and certain fees | Better for comparing offers side by side |

For example, a loan with a 10% interest rate and a 5% origination fee may have a higher APR than a loan with an 11% interest rate and no origination fee. The lower interest rate may look better at first, but the APR can show that the total cost is actually higher.

That is why you should avoid comparing personal loans by interest rate alone. If two loan offers have different fees, APR usually gives you the clearer comparison.

How APR Changes What You Pay Back

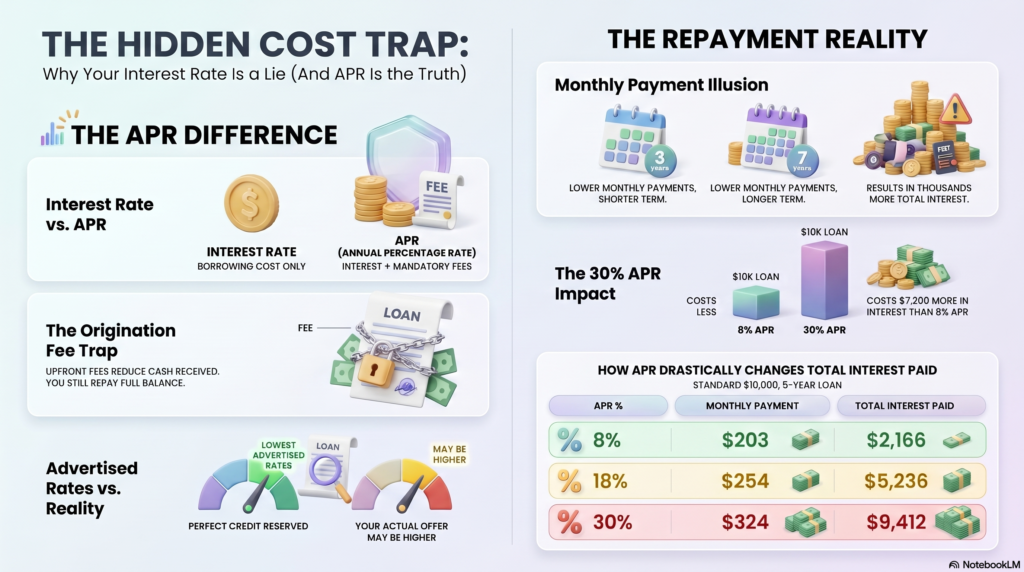

APR affects both your monthly payment and the total amount you repay. The higher the APR, the more interest builds into the loan, even when the loan amount and repayment term stay the same.

Here is a simple example using a $10,000 personal loan with a five-year repayment term and no added fees:

| Loan Amount | Repayment Term | APR | Estimated Monthly Payment | Total Interest | Total Repaid |

|---|---|---|---|---|---|

| $10,000 | 5 years | 8% | $203 | $2,166 | $12,166 |

| $10,000 | 5 years | 18% | $254 | $5,236 | $15,236 |

| $10,000 | 5 years | 30% | $324 | $9,412 | $19,412 |

The difference is significant. At 8% APR, the loan costs about $2,166 in interest over five years. At 30% APR, the same loan costs about $9,412 in interest.

That is why APR matters so much when comparing personal loans. A higher APR does not just raise the monthly payment. It can add thousands of dollars to the total cost of borrowing.

Why a Lower Monthly Payment Can Still Cost More

A lower monthly payment can be helpful when you need more room in your budget. But it does not always mean the loan is cheaper.

With personal loans, the repayment term has a major effect on total cost. A longer term spreads the balance over more months, which can reduce the monthly payment. The tradeoff is that interest has more time to add up.

Here is an example using a $10,000 personal loan at 18% APR:

| Loan Amount | APR | Repayment Term | Estimated Monthly Payment | Total Interest | Total Repaid |

|---|---|---|---|---|---|

| $10,000 | 18% | 3 years | $362 | $3,015 | $13,015 |

| $10,000 | 18% | 5 years | $254 | $5,236 | $15,236 |

| $10,000 | 18% | 7 years | $211 | $7,710 | $17,710 |

The seven-year loan has the lowest monthly payment, but it also costs the most overall. Compared with the three-year loan, it lowers the monthly payment by about $151, but increases total interest by about $4,695.

That does not mean a longer term is always wrong. Sometimes a lower payment is necessary to keep the loan affordable. The important point is to compare both numbers: monthly payment and total repayment cost.

What Can Make a Personal Loan APR Higher

Personal loan APR is based on risk, loan structure, and lender pricing. In general, lenders offer lower APRs to borrowers they see as more likely to repay on time.

Several factors can affect the APR you receive:

- Credit score and credit history: A stronger credit profile can help you qualify for a lower APR. Missed payments, high balances, or limited credit history can lead to a higher rate.

- Income and employment stability: Lenders want to see that you have enough reliable income to make the monthly payments.

- Debt-to-income ratio: If a large share of your income already goes toward debt, a lender may see the new loan as riskier.

- Loan amount: Larger loans may come with different pricing because the lender is taking on more exposure.

- Repayment term: Longer terms can sometimes come with higher APRs because the lender waits longer to be repaid.

- Origination fees: Some lenders charge upfront fees that can raise the APR, even if the interest rate looks competitive.

- Lender pricing: Two lenders can review the same borrower and offer different APRs. That is why comparing multiple offers matters.

A higher APR does not always mean the loan is automatically wrong, but it does mean you should look more closely at the total cost. Before accepting an offer, compare the APR, fees, monthly payment, repayment term, and total amount you will repay.

Fees That Can Raise the Cost of a Personal Loan

Personal loan fees can change what the loan really costs, even when the interest rate looks reasonable. That is why APR is useful: it can include the interest rate plus certain lender fees, such as origination charges.

The fee to watch most closely is the origination fee. This is an upfront charge some lenders take for processing or funding the loan. It is often deducted from the loan proceeds before the money reaches you.

For example, if you are approved for a $10,000 loan with a 5% origination fee, the lender may deduct $500 and send you $9,500. You may still have to repay the full $10,000, plus interest.

Other fees can also affect the cost of borrowing:

- Late payment fees: Charged if you miss the payment due date.

- Returned payment fees: Charged if a payment fails because of insufficient funds or another processing issue.

- Prepayment penalties: Less common with personal loans, but worth checking. This fee applies if the lender charges you for paying off the loan early.

- Optional add-on costs: Some loans may offer extras such as credit insurance. These can increase the total cost and should be reviewed carefully before agreeing.

Before accepting a loan, check the APR, the fee list, the amount you will actually receive, and the total repayment cost. A loan with no origination fee is not always cheaper, but fees can make a low advertised rate less valuable than it first appears.

Common Mistakes People Make When Reading APR

APR is meant to make loan costs easier to compare, but it is still easy to focus on the wrong number. Before signing a personal loan agreement, watch for these common mistakes:

- Assuming the advertised rate is guaranteed: The lowest APR in an ad is usually reserved for borrowers with stronger credit, steady income, and lower overall risk. Your actual rate will depend on your financial profile and may be higher.

- Focusing only on the monthly payment: A low monthly payment can feel affordable, but it may cost more if the loan is stretched over a longer term. Always compare the monthly payment with the total repayment cost.

- Looking at the interest rate but ignoring APR: The interest rate does not always show the full cost of borrowing. A loan with an 8% interest rate and high upfront fees may have a higher APR than a loan with a 10% interest rate and no origination fee.

- Forgetting how origination fees affect your payout: If you need exactly $10,000 but the lender deducts a 5% origination fee upfront, you may receive only $9,500. You may still have to repay the full $10,000 plus interest.

Treating prequalification as a final offer: Prequalified rates are useful estimates, but they are not final loan terms. Your APR can still change after the lender reviews your full application, verifies your information, and runs a hard credit inquiry.

How to Compare Two Personal Loan Offers Side by Side

The easiest way to compare personal loan offers is to look beyond the advertised rate and place the full terms next to each other. A loan with a lower monthly payment is not always cheaper, and a loan with a lower interest rate may still cost more if it comes with higher fees.

Use the same comparison points for each offer:

| What to Compare | Loan Offer A | Loan Offer B |

|---|---|---|

| Loan amount | $10,000 | $10,000 |

| Interest rate | 11% | 12% |

| APR | 13.5% | 12% |

| Origination fee | 5% | $0 |

| Amount received | $9,500 | $10,000 |

| Repayment term | 5 years | 5 years |

| Estimated monthly payment | Lower or higher? | Lower or higher? |

| Total interest | Compare full cost | Compare full cost |

| Total amount repaid | Compare final total | Compare final total |

In this example, Loan Offer A has the lower interest rate, but the origination fee raises the APR and reduces the amount the borrower receives. Loan Offer B has a slightly higher interest rate, but no origination fee, which may make it the better deal depending on the final monthly payment and total repayment cost.

When comparing offers, pay close attention to:

- APR: The broader cost of the loan, including interest and certain fees.

- Monthly payment: The amount you need to fit into your budget.

- Repayment term: The number of months or years you will be paying.

- Total repayment cost: The full amount you will pay by the end of the loan.

- Amount received: The money you actually get after any upfront fees.

- Fees and penalties: Origination fees, late fees, returned payment fees, and possible prepayment penalties.

A good offer should be affordable each month and reasonable over the full repayment period. If one loan has a lower payment but a much higher total cost, it may only be making the debt look easier in the short term.

When a Personal Loan APR Deserves a Closer Look

A personal loan APR does not have to be perfect to be useful. In some situations, a higher APR may still be manageable if the loan solves a short-term problem, replaces more expensive debt, or gives you a clear repayment plan.

Still, some offers deserve extra caution before you sign.

The APR Is Close to a Credit Card Rate

If the personal loan APR is similar to the rate you already pay on a credit card or other debt, the loan may not save much money. It may still simplify repayment, but the savings could be limited.

Before accepting, compare the total cost of keeping your current debt where it is against the full cost of the new loan.

The Origination Fee Is High

A high origination fee can make a loan more expensive than it first appears. It can also reduce the amount of money you actually receive.

This matters most when you need a specific loan amount. If the fee is deducted upfront, you may need to borrow more than planned to cover the same expense.

The Term Is Much Longer Than You Need

A longer repayment term can make the monthly payment easier to handle, but it can also increase the total interest you pay.

If the payment only looks affordable because the loan stretches across many years, compare it with a shorter term before deciding.

The Monthly Payment Leaves No Room in Your Budget

A loan payment should fit your budget without making every month feel fragile. If the payment only works when everything goes perfectly, the loan may create more pressure than it solves.

Review your regular expenses, savings needs, and emergency costs before accepting the offer.

The Terms Are Hard to Understand

A trustworthy loan offer should clearly show the APR, interest rate, fees, repayment term, monthly payment, total repayment amount, and any penalties.

If the lender makes those details difficult to find or understand, take more time before moving forward. A personal loan should make your financial picture clearer, not harder to read.

Conclusion

APR is one of the most important numbers to review before choosing a personal loan because it gives you a clearer view of what borrowing really costs. The interest rate matters, but APR can show more of the full picture when lender fees are part of the loan.

Still, APR should not be the only number you compare. A good loan decision also looks at the monthly payment, repayment term, origination fee, amount received, and total amount repaid. A loan that looks affordable month to month may still cost more over time if the term is too long or the fees are too high.

Before accepting a personal loan, compare offers side by side and read the final terms carefully. The best offer is usually the one that gives you a manageable payment, a clear repayment schedule, and the lowest total cost you can reasonably qualify for.

Frequently Asked Questions

What does APR mean on a personal loan?

APR stands for annual percentage rate. It shows the yearly cost of borrowing, including the interest rate and certain lender fees. The CFPB explains that APR includes the interest rate plus additional fees charged by the lender, such as origination charges.

Is APR the same as the interest rate?

No. The interest rate shows what the lender charges to borrow the principal. APR gives a broader view because it can include the interest rate plus certain loan fees. That makes APR more useful when comparing two personal loan offers with different fee structures.

What is a good APR for a personal loan?

A good APR depends on your credit profile, income, debt level, loan amount, repayment term, and the lender. In general, the lower the APR, the less expensive the loan may be. But you should still compare the monthly payment, fees, term length, amount received, and total repayment cost before deciding.

Why is my APR higher than the advertised rate?

Advertised rates usually show the lowest APR available to the strongest borrowers. Your actual APR may be higher if the lender sees more risk based on your credit score, income, existing debt, loan term, loan amount, or other application details.

Does prequalification guarantee my APR?

No. Prequalification is usually an estimate, not a final offer. The lender may still verify your information and run a hard credit inquiry before approving the loan. The CFPB explains that hard inquiries often happen after applying for credit and can affect your credit score.

Can an origination fee make a personal loan more expensive?

Yes. An origination fee can increase the cost of the loan and reduce the amount of money you receive. The CFPB lists origination fees among common personal installment loan fees.

Should I choose the lowest APR or the lowest monthly payment?

Start with APR, but do not stop there. The lowest APR usually points to a lower-cost loan, but the best offer should also have a monthly payment you can afford, a repayment term that makes sense, and a reasonable total repayment cost.

Can I lower my personal loan APR?

You may be able to qualify for a lower APR by improving your credit score, reducing existing debt, increasing income stability, applying with a qualified co-borrower, choosing a shorter term, or comparing offers from multiple lenders. The most reliable step is to compare prequalified offers before submitting a full application.

0 Comments